The world’s major economies have performed quite well in recent months despite the influence of political and policy upheaval. Brexit and the outcome of the U.S. election have yet to produce the negative outcomes some had feared.

But there may be challenging times ahead. The commitment to free trade in several markets remains in question, and any reduction in a trade alliance could diminish growth in all of the participating countries. Monetary policy, on balance, is becoming less accommodative. And asset prices in some markets are stretching their mooring to fundamental value.

Yet unless one of these risks becomes unmanageable, the global expansion seems poised to continue, and is even gaining steam in some places.

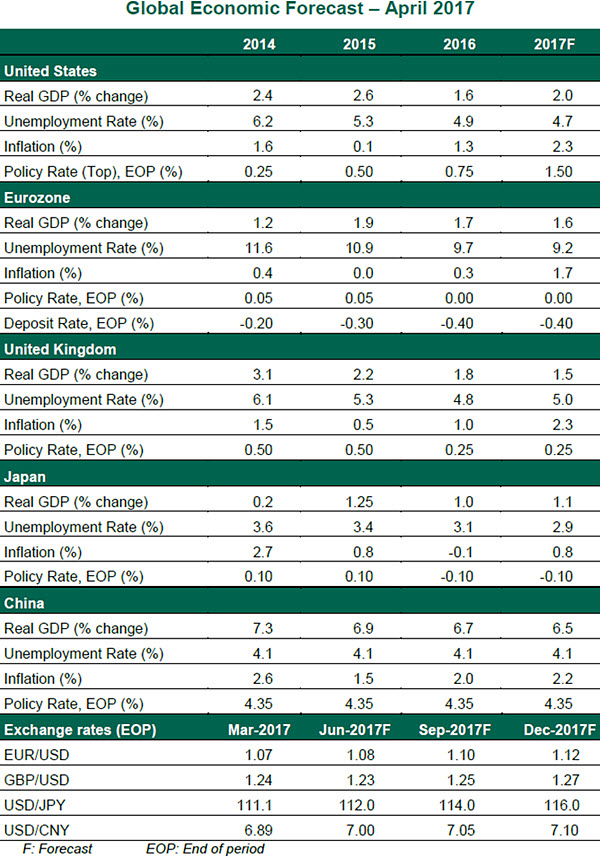

United States

The current U.S. economic expansion is already the third longest on record and could easily move further up the list. More importantly, it is in a sweet spot, with the U.S. Federal Reserve’s full employment and price stability mandates satisfied. Steady growth close to the potential level is predicted for this year. As discussed in a recent weekly commentary, we are not expecting much fiscal stimulus this year, and major change may not even occur in 2018.

Consumer spending is projected as the driver of growth after a lull in the January-February period. Business expenditures and residential investment outlays are expected to make modest positive contributions. Further strengthening of the labor market should move the jobless rate lower, while an acceleration of wages is most likely in the months ahead. Overall inflation crossed the Fed’s 2.0% target in February, but conditions do not suggest that prices will grow much faster than that.

The Fed raised the policy rate in March after taking a similar step at the end of last year. Assuming a calm geopolitical situation and no market turbulence in the wake of the upcoming French and German election outcomes, the Fed is on track to implement two more policy rate hikes in 2017. It is also weighing the option of shrinking its balance sheet later this year or early next year, which would be an important step in the effort to normalize monetary policy.

Eurozone

Purchasing Manager Indices across the continent have had a fairly spectacular run over recent months, highlighting the growing strength of the eurozone’s economic recovery. Businesses appear to be shrugging off political risk, as is evident by the positive economic data coming out of France.

Our base case remains that none of electoral tail risks will be realized in 2017, although Italy could surprise on the downside. Furthermore, we continue to expect the eurozone to benefit from relocation of businesses, especially in the financial services industry, from the United Kingdom to the continent. Overall, we expect real gross domestic product (GDP) to grow at 1.6% in 2017 and unemployment to fall marginally to 9.2%. Risks are tilted to the upside.

Inflation has exceeded expectations since late 2016, but it has been largely an oil story and therefore transitory. The recent decline in oil prices, along with ample spare capacity — both material and labor — should keep a lid on price pressures. We expect eurozone-wide headline inflation to soften from its recent highs and average 1.7% for the full year.

Consequently, we expect the European Central Bank (ECB) to continue its accommodative stance while it awaits a “durable,” “self-sustained” and “broad-based” rise in inflation over the “medium term.” (Quotations indicate the ECB’s inflation adjustment criteria.) We believe that some of the recent comments by various ECB policy makers have been over-interpreted by the markets and we do not expect any change in ECB’s deposit rate before early 2018. We do, however, expect the ECB to announce a reduction in the pace of its asset purchases in the third quarter of 2017.

United KingdomAs we noted in our recent commentary, Brexit will weigh on the U.K.’s economic prospects in the years to come. The British government triggered Article 50 of the Lisbon Treaty last week and the U.K. will have two years to settle the terms of separation and future engagement with the European Union.

The recent contraction in business investment highlights the negative impact from the uncertainty around the U.K.’s future regulatory and trade regime. One of the immediate consequences of last year’s referendum was the sharp depreciation of the pound sterling. For an economy where consumption makes up 60% of all economic activity, imported inflation combined with tepid nominal wage growth is an obvious challenge. Recent declines in consumer confidence and stretched household balance sheets indicate that retail sales will likely weaken further. Some relief has been provided by the boost to overseas revenues of U.K. corporations from sterling’s depreciation, but that is unlikely to offset the weakness in other quarters.

U.K. Chancellor Phillip Hammond has indicated an unwillingness to use fiscal policy to cushion the economy against the aforementioned headwinds. We forecast real GDP growth to decelerate to 1.5% in 2017, with risks tilted to the downside. For the same reason, we expect the Bank of England to maintain an accommodative stance and look though any further spike in inflation.

JapanThe Japanese economy should continue to grow at a steady, if uninspiring, pace of just above 1% in 2017. Growth will be supported by buoyant investment, a pick-up in export revenues on the back of an improving global growth environment and the yen’s weakness and fiscal spending from last year’s supplementary budget. The Bank of Japan’s (BoJ) policy stance should remain accommodative, but we do not foresee any marginal boost to growth from monetary policy. As we have noted in our previous editions, the lack of structural reforms (particularly in the labor market), demographic constraints, and inadequate fiscal stimulus continue to limit Japanese growth and price fundamentals.

Disappointing wage hikes after the spring negotiations as well as tepid inflation expectations continue to cap Japanese price level increases. While we do not expect a return to the deflation we saw in the middle of last year, our inflation forecast of 0.8% for 2017 is contingent on the yen’s weakness and stable oil prices. We expect the BoJ to maintain its benchmark policy rate at -0.1%, though pursuing its “around 0%” yield target for 10-year Japanese government bonds could prove challenging in the face of rising global yields. Therefore, we do not rule out technical adjustments to the BoJ’s policy, even if the overall policy stance remains unchanged.

ChinaChinese policymakers have adjusted their growth target from 6.5-7% last year to “around 6.5%” for 2017. But there is little to show for the much awaited Chinese economic rebalancing from investment to consumption. The dissonance between producer price inflation and consumer price inflation highlights the failure on this front. While the former has shot up to close to 8% on the back of strong public investment spending (growing more than twice as fast as private investment), the latter is languishing below 1% due to weak retail spending.

At the same time, the target for job creation has been raised. Officials are cognizant of the need to rebalance the economy, which would necessitate a moderation in growth; but social stability remains paramount for China.

Monetary authorities are torn between tackling a frothy financial sector and stimulating weak real activity. The recent hike in repo rates, even as the benchmark policy rate has remained unchanged, demonstrates that the authorities are using different tools to manage financial and price stability separately. In addition, ad hoc macroprudential measures are being employed to manage the real estate boom, albeit with limited success, and foreign reserves are being deployed to manage yuan’s stability.

We continue to believe that the fundamental issues with China’s banking sector, asset markets and the composition of growth pose serious long-term challenges. But all things considered, it is important to note the extraordinary ability of Chinese policymakers to sustain the status quo for much longer than most analysts have expected. Indeed, a Chinese hard landing has been on the list of global economic threats for the better part of a decade now. While the weight of evidence over the last few years suggests an unwillingness of Chinese policymakers to take tough measures to address fundamental imbalances and sustainability issues, we expect a sense of self-preservation to prompt corrective measures sooner rather than later.

northerntrust.com

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

©

2017 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/disclosures.

© Northern Trust

Read more commentaries by Northern Trust