Amid the political uncertainty in Europe prompted by upcoming elections and the start of Brexit negotiations, another story is quietly playing out, involving improved economic and corporate conditions. Here, Philippe Brugere-Trelat and Katrina Dudley of Franklin Mutual Series explain how they’re cutting through the political noise to uncover potential opportunities in European equities. They take a fresh look at two areas in particular that have been prominent in the financial news of late: UK-listed stocks and European financials.

We believe the economic and financial backdrop for European stocks has improved and the region is better able to weather unexpected shocks than in recent years. Although recent history shows there is reason to be skeptical of political polls, we do not believe populist parties will score victories significant enough in national elections to cause an existential threat to the European Union (EU). If elections play out as polls suggest, and if the United Kingdom and the EU can begin constructive Brexit negotiations, we believe pent up corporate demand and relief among investors could lead to strong economic and financial market performances across Europe.

On balance, we maintain a positive outlook for European equities, but we feel selectivity is crucial. Our bottom-up stockpicking process focuses on buying good companies trading at discounts to their intrinsic values based on fundamental analysis (e.g., price-to-cash-flow multiples or sum-of-the-parts analysis). Macroeconomic conditions and political events may affect an individual company’s valuation, but we do not make top-down sector or geographic positioning decisions based on an expected event outcome.

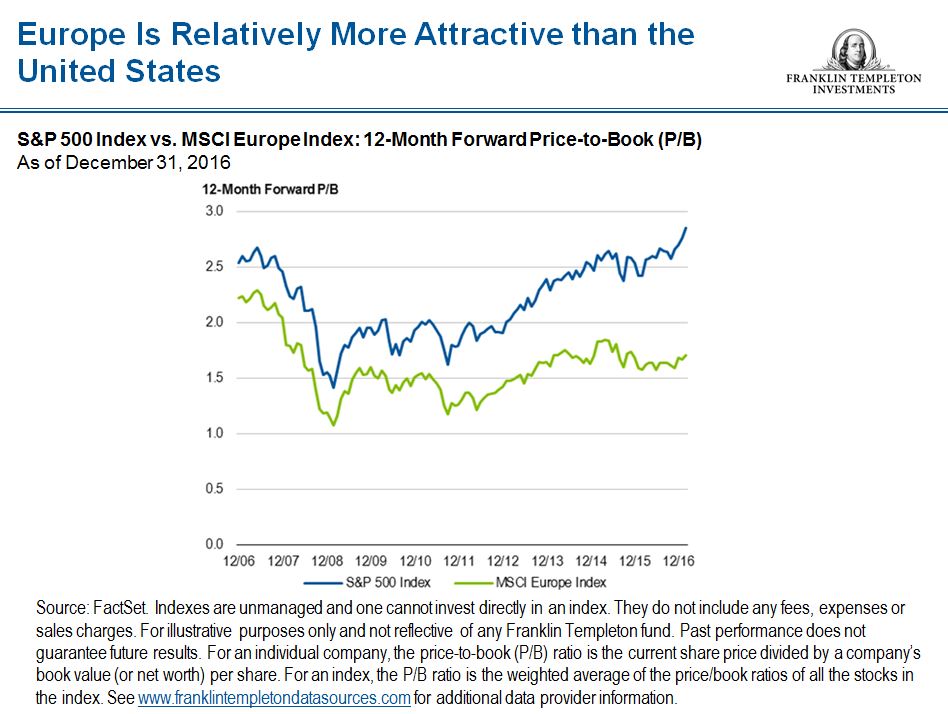

Based on our fundamental analysis, we believe conditions have begun to turn more favorable for European stocks, especially value stocks and companies in cyclical industries. Comparing the S&P 500 to the MSCI Europe Index, European stocks are significantly less expensive than US stocks on a number of metrics, including price-to-book (P/B) and price-to-cash-flow; the recent outperformance of US stocks relative to European stocks has made valuations even more attractive, in our view.1

Stronger economic growth in Europe and the positive turn in inflation are good news for profit margins and should enable companies to regain some pricing power in our view. At similar stages of the economic cycle in the past, we have found that companies in economically sensitive industries, such as automotive, construction and industrials, have generally fared well, and are attractively priced relative to their historical averages. On the other hand, our analysis of companies based on a combination of factors, including price-to-earnings (P/E), P/B and dividend yields, shows that areas of the equity market considered defensive or lower volatility (e.g., consumer staples) are trading at historically elevated levels.

Any rise in interest rates and steepening in yield curves are also likely positive for financials but for “bond proxy” stocks, such as staples and utilities. Within the financials sector, we have found a greater number of potentially attractive opportunities in the region’s insurance industry, which we regard as being in relatively better financial shape and operating in a more stable regulatory environment than banks.

In addition, a number of insurance companies are working through restructurings of their business, including the monetization of non-core assets, in order to seek to improve their operational performance.

We are of the view that, generally, banks in Europe are still challenged by issues of asset quality (non-performing loans) and insufficient capital levels. In addition, the negative interest-rate policy of the European Central Bank (ECB) has adversely impacted banks’ net interest margins and profitability. However, not all banks in the region are unattractive to us and we continue to see opportunities in French and UK banks that offer relatively solid balance sheets, are well-leveraged to a resumption of credit growth and have exposure to parts of the world other than Europe, namely the United States or Asia.

Focusing on the United Kingdom, we believe current conditions favor large UK multinational companies that obtain much of their earnings abroad or report their results in foreign currencies (e.g., global integrated oil and gas companies). Domestically-oriented UK companies are likely to face more challenging conditions thanks to a weaker British pound and potentially softer consumer demand. In addition, Brexit is a significant risk for UK financial companies of all stripes as provisions that allow the sale of financial products throughout the European bloc could be lost.

In Europe, we believe improved economic and corporate conditions are being overshadowed by political and financial uncertainty. Brexit, election-related anxieties in other major EU countries and uncertainty regarding future monetary policy moves by the ECB and Bank of England have seemingly led investors to take a wait-and-see approach. We believe the probability of Brexit and election outcomes causing an existential risk to the EU is low.

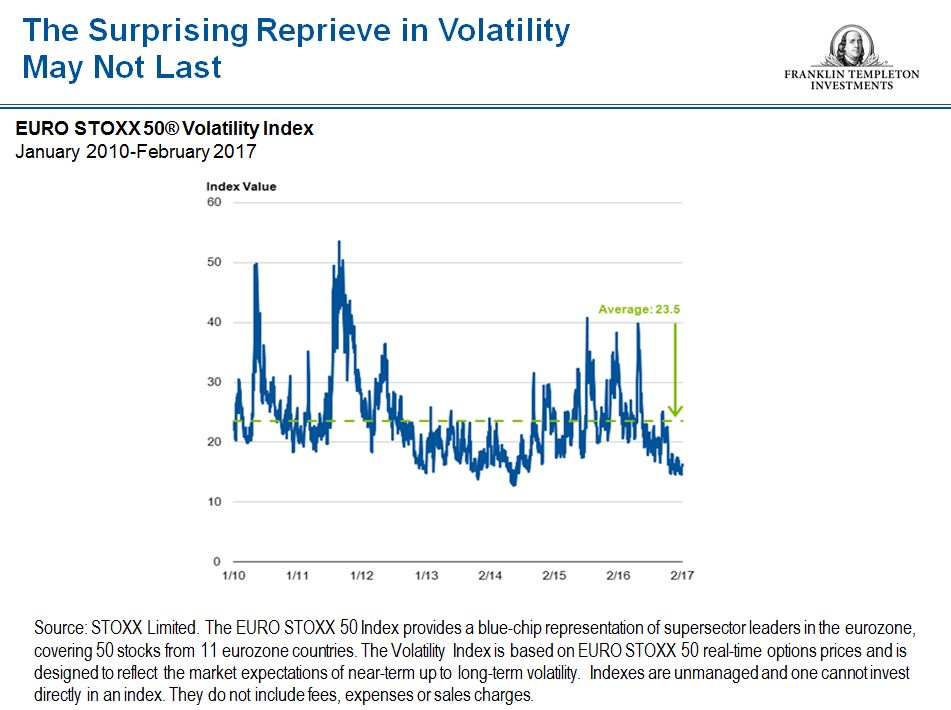

However, we believe that volatility is also likely to resurface, after an unexpected period of calm in late 2016 and early 2017. While political, economic and geopolitical conditions make it challenging to predict near-term moves or to time specific portfolio actions, we are focused on searching for potential opportunities in companies with attractive risk/reward profiles. From our perspective, periods of heightened volatility can affect stocks in an indiscriminate manner, providing us with excellent windows for opportunistic investing.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

The comments, opinions and analyses expressed herein are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. Because market and economic conditions are subject to rapid change, comments, opinions and analyses are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy.

This information is intended for US residents only.

What Are the Risks?

Franklin Mutual European Fund

All investments involve risks, including possible loss of principal. Value securities may not increase in price as anticipated or may decline further in value. Special risks are associated with foreign investing, including currency fluctuations, economic instability and political developments. Because the Fund invests its assets primarily in companies in a specific region, it is subject to greater risks of adverse developments in that region and/or the surrounding regions than a fund that is more broadly diversified geographically. Political, social or economic disruptions in the region, even in countries in which the Fund is not invested, may adversely affect the value of securities held by the Fund. The Fund’s investments in smaller-company stocks carry an increased risk of price fluctuation, especially over the short term. The Fund’s investments in companies engaged in mergers, reorganizations or liquidations also involve special risks as pending deals may not be completed on time or on favorable terms. These and other risk considerations are discussed in the fund’s prospectus.

It is generally expected that the UK’s exit from the EU will take place within two years after the UK formally notifies the European Council of its intent to withdraw, but there is still considerable uncertainty regarding the potential consequences and timeframe for such exit, which may increase global market volatility. Any further exits from the EU, or belief that such exits will occur, may cause additional market disruption globally and introduce new legal and regulatory uncertainties.

Investors should carefully consider a fund’s investment goals, risks, charges and expenses before investing. To obtain a summary prospectus and/or prospectus, which contains this and other information, talk to your financial advisor, call us at (800) DIAL BEN/342-5236 or visit franklintempleton.com. Please carefully read a prospectus before you invest or send money.

________________________________

1 Source: FactSet. The S&P 500 Index is a gauge of US large-cap equities capturing 80% coverage of market capitalization. The MSCI Europe Index captures large- and mid-cap representation across 15 developed market countries in Europe. Indexes are unmanaged and one cannot directly invest in them. They do not include fees, expenses or sales charges. For an individual company, the price-to-book (P/B) ratio is the current share price divided by a company’s book value (or net worth) per share. For an index, the P/B ratio is the weighted average of all the price/book ratios of stocks in the index.

© Franklin Templeton Investments

© Franklin Templeton Investments

Read more commentaries by Franklin Templeton Investments