SUMMARY

- The Fed Contemplates the Great Reduction

In a recent meeting here at the bank, two of my partners were celebrating their success at losing weight. One relied primarily on fitness, while the other followed a strict diet. Both agreed, though, that reduction was more difficult than accumulation.

The Federal Reserve, which meets again next week, finds itself contemplating a similar transition. Having accumulated a massive portfolio of securities during its quantitative easing (QE) program, the Fed has now arrived at a point where reduction is appropriate. But trimming the weight of monetary accommodation may not be easy.

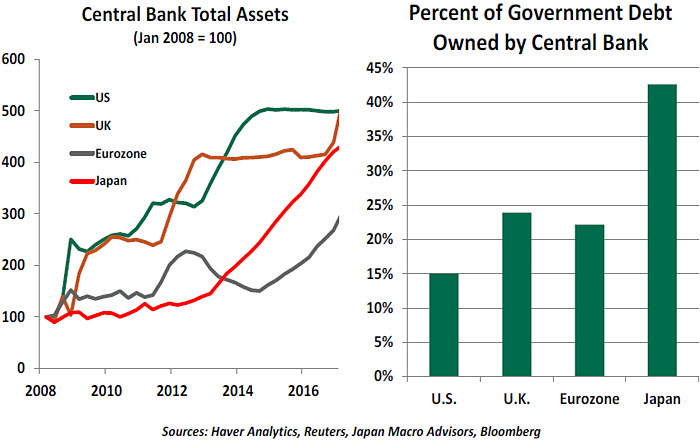

When short-term interest rates were lowered to near-zero at the end of 2008, the Federal Reserve and other global central banks turned to unconventional strategies. Both the Fed and the Bank of England aggressively took up QE, and the European Central Bank and the Bank of Japan followed suit somewhat later. The Fed is the first of the bunch to seriously consider unwinding these efforts.

QE operates through several channels. Purchasing long-term securities lowers long-term rates, which aids sectors of the economy that depend on longer-term credit. By reducing the yield on risk-free assets, QE raises the cost of risk aversion and invites capital to become more aggressive. In combination with forward guidance, QE also reinforces the message to markets that the central bank is intent on doing whatever it takes.

QE was hotly debated in each of the markets in which it was applied. From a historical perspective, the U.S. Fed was once responsible for supporting liquidity in government bond markets, a linkage that was broken in the 1950s to establish the independence of monetary and fiscal policy. The large-scale asset purchases that began in 2008 were seen in some corners as backtracking on that accord, and as a step toward monetizing debt.

When mortgage-backed securities (MBS) were added to the QE mix, some complained the Fed was favoring the housing industry over others. Central bank investment programs have affected pricing and liquidity in the markets where they have concentrated their holdings. For a multitude of reasons, former Richmond Fed President Jeffrey Lacker expressed concern that QE placed the Fed’s reputation at risk, and urged an early end to the program. (Ironically, Lacker was forced to step down from his post earlier this year after admitting to an ethical lapse.)

There are certainly differences of opinion over how effective QE has been. As a whole, however, it is fair to say that the Fed’s aggressive strategy is one reason why the American economy has enjoyed an eight-year recovery. This outcome has diminished the need for easy money, and the Fed has set about slowly getting back to normal.

Designing a program to skinny down the Fed’s balance sheet will require exploration of the following topics.

Setting a Goal

Defining the new normal when it comes to the Fed’s balance sheet isn’t easy. At first blush, one might ask why asset holdings shouldn’t decline to where they stood prior to the financial crisis. The answer would be that neither banks nor the Fed want that outcome.

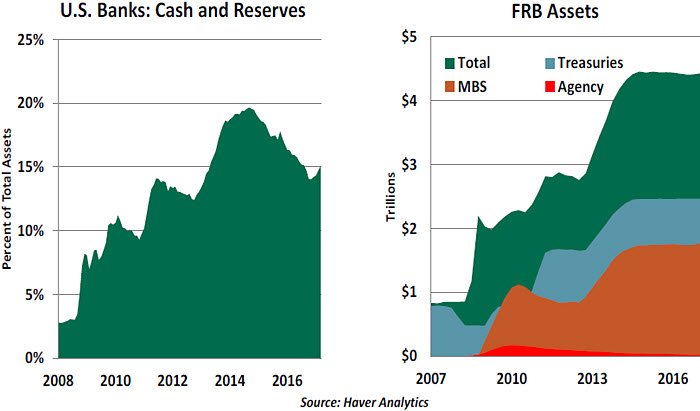

The optimal level of liquidity in the banking system has risen substantially since 2008. The level of economic and market activity has grown since then, requiring greater reserves. More significantly, the appetite among banks for leaving funds on deposit with the Fed has undergone a sea change.

For most of its history, the Federal Reserve has been prohibited from paying interest on the funds deposited there by financial institutions. This absence of compensation led banks to keep the level of reserves they deposited at the Fed to the bare minimum. Sweep accounts, which move funding out of deposits and into money market assets daily, were widely employed for this purpose.

A bill passed in 2006 allowed the Fed to begin paying interest in 2011, but the implementation date was moved forward during the peak of the 2008 stress. The interest rate on excess reserves (IOER) was initially set at around 25 basis points; this didn’t seem like much, but banks realized intrinsic returns from placing their spare funds with a strong counterparty. Risk aversion, along with the substantial easing of monetary policy, caused bank reserve balances to skyrocket in the ensuing years.

From the Fed’s perspective, paying interest on reserves provides a tool it can use to modulate the degree to which its creation of money translates into credit expansion. (For the economic technicians among you, the IOER can determine how much of the monetary base turns into the money supply.) Offering a lower rate promotes more lending; a higher rate might contain it. In combination with the Fed’s Reverse Repurchase Program, the payment of interest on reserves helps monetary authorities manage overnight interest rates efficiently within the targeted band.

From the perspective of banks, leaving reserves at the Fed is still desirable today, even though concern about private counterparties has receded. Among the post-crisis regulatory reforms is a requirement that banks hold “high-quality” liquid assets in amounts that covered the risk of sudden funding loss. Excess reserves held at the Fed fit this purpose perfectly, and are also friendly to calculations of risk-based capital.

The Fed has gotten a smattering of criticism for essentially paying banks not to lend. And why should the central bank reward private institutions whose perceived misdeeds had such a great social cost? The fact that some recipients of interest from the Fed are U.S. subsidiaries of foreign banks has only intensified the concern. But there are very sound systemic reasons for the practice, as discussed

here.

So it seems likely the Fed’s balance sheet will settle in at a lower level. But what might that be? The topic has been debated actively. Former Fed Chairman Ben Bernanke recently

suggested a minimum level of $2.5 trillion. Other analysts have arrived at a lower number; discussants at the Fed’s Jackson Hole Symposium last summer went in the other direction,

proposing that no balance sheet reductions were necessary.

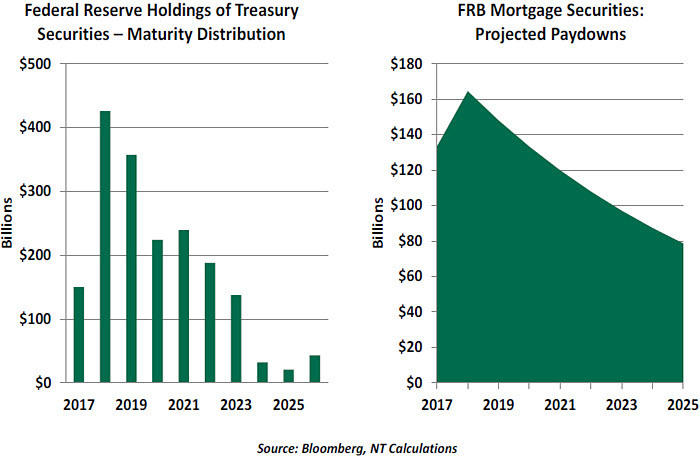

The Fed has said it ultimately prefers to hold its assets exclusively in Treasury securities. But it will take a very long time for the MBS it owns to fully recede. At some point in the future, it is entirely possible the Fed will resume its purchases of government securities even as its MBS holdings continue to run off.

Just as it is hard to define a neutral long-run level of interest rates, it is difficult to ascertain how large a central bank’s balance sheet should be. The answer may vary over time, based on market factors. Difficult though it will be, the Fed will have some idea of the balance sheet’s destination before it begins its right-sizing journey.

Designing a DietIn theory, there is nothing to prevent the Fed from reaching its new target almost immediately. The securities it holds are highly liquid and highly marketable, and could be sold in a short span of time. But even if properly previewed, it is highly likely the sudden transition would be disruptive to the global financial system.

The release of such a large block of securities back into the market would almost certainly lower bond prices and expose the Federal Reserve to capital losses upon sale. It’s not as if the Fed can’t afford this - it remanded $92 billion to the U.S. Treasury last year, the excess of the interest it earned on its bond holdings over its expenses. But the appearance of the central bank taking a loss, along with the hunger among the U.S. Congress for revenue, could raise eyebrows among the Fed’s detractors.

It would be simplest to allow the Fed’s holdings to run off at a natural pace. (The Fed’s public statements have advocated a “passive” approach.) Quite a few of the Treasury securities owned by the central bank will come due over the next several years. And MBS generate regular principal returns as homeowners move or refinance their loans. The Fed’s MBS holdings are being paid down at a rate of about 10% per year, which would represent more than $170 million annually.

Simply ceasing to reinvest principal that comes due also saves the Fed from designing and communicating a decision rule aimed at modulating the pace of balance sheet reduction in response to economic performance. Some have suggested the Fed might begin by tapering its reinvestments on a given schedule, but there is no history on which such tactics could be based. And beginning slowly means it will take the Fed longer to reach its ultimate goal.

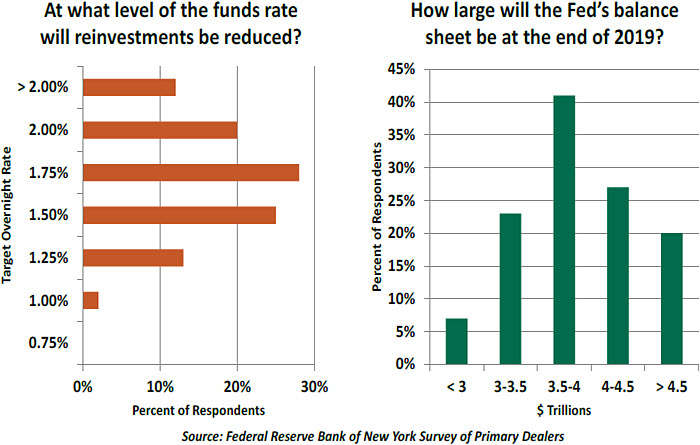

Timing is EverythingFed officials have stated that balance sheet reductions would not commence until the process of interest rate normalization is “substantially underway.” There is no direct translation of that phrase to a specific rate level, but many analysts have guessed that an overnight rate of 1.25% to 1.5% would be sufficient. Most forecasts, including the Fed’s, anticipate reaching that level by the end of this year.

With that threshold approaching, Fed officials have made increasing mention of balance sheet size in their speeches and meeting minutes. Proper foreshadowing will be critical to avoiding a repeat of the 2013 “

taper tantrum.” For now, the bond markets do not seem to be living in fear of a big release of supply from the central bank; in fact, long-term interest rates have fallen even as mention of Fed balance sheet discipline has advanced.

The Fed might want to get the process started sooner rather than later. There will likely be a leadership transition at the top of the table early next year, and there may be value in having the balance sheet on its way down before then. This would relieve the incoming chair of having to trigger the process soon after taking office, allowing the chair to ease into the role more gradually.

The charts below summarize the expectations of leading investment banks for the Fed’s balance sheet. There is little consensus among them. One could also imagine there is little clear consensus within the Federal Reserve about the best way to proceed.

It is almost impossible to anticipate exactly how markets and the economy will react when the time comes. In order to isolate that reaction, some think the Fed will announce the change in its reinvestment policy at a meeting where they leave interest rates unchanged. That strategy would also allow the Fed chair to devote the post-meeting press conference to an explanation of balance sheet strategy.

All of this may sound overwhelming, and problematic. But the problems associated with Fed balance sheet reduction are good ones to have. We wouldn’t be engaged in this evaluation if the economy weren’t on sound footing. This is exactly the outcome the Fed was hoping for.

Both partners in the weight loss discussion wanted to avoid returning to their former states. They had set targets, designed strategy to reach them, and were monitoring conditions carefully to prevent a relapse. The Fed may not be getting back to a thirty-two inch waist, but the belt tightening that lies ahead will be a welcome development.

© Northern Trust

www.northerntrust.com

© Northern Trust

Read more commentaries by Northern Trust