Does China Present Global Risk? The Coming Slowdown in China Could Affect the Reflation Trade

The Coming Slowdown in China Could Affect the Reflation Trade

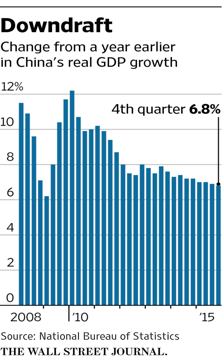

In the first quarter, China’s GDP grew 6.9% which was the fastest growth since the third quarter of 2015. The modest increase over the 6.8% growth in the fourth quarter was fueled by a 20% increase in property sales and fiscal spending, which rose by more than 20%. The improvement in China’s growth rate may be short lived, as a combination of tighter monetary policy and stricter banking regulations begin to impinge on growth in coming months. Since the financial crisis, the fiscal policy of the Chinese government and monetary policy of the People’s Bank of China (PBOC) have bordered on being manic depressive. Policy makers have alternated between efforts to temper real estate bubbles, a growing corporate debt bubble, serial housing bubbles, and unprofitable excess capacity, only to reverse course and stimulate growth through more debt, more government fiscal stimulus, and new waves of real estate speculation.

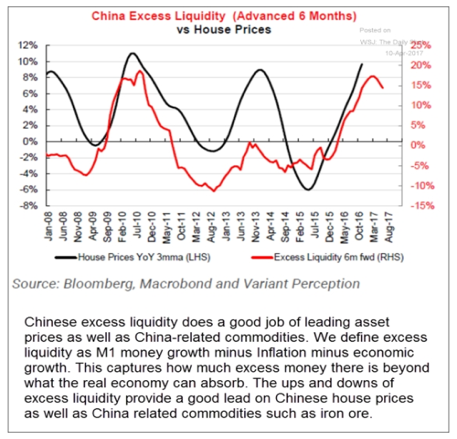

The stop and go changes in fiscal and monetary policy are apparent in the ebb and flow of excess liquidity in China. To calculate excess liquidity, inflation and GDP growth is subtracted from M1 money supply growth. For instance, if M1 money growth is 20%, inflation is 2.0% and GDP growth is 7%, excess liquidity would be 11% (20% -2% -7% = 11%). Since changes in economic activity lag changes in liquidity by 6 months or more, excess liquidity is shifted forward by six months to approximate economic turning points. Housing prices in China have been highly correlated to excess liquidity. After the financial crisis, excess liquidity soared and peaked in late 2010 near 18%. GDP growth rebounded strongly in 2009 and posted a secondary peak in late 2010, just as excess liquidity was beginning to recede. Excess liquidity fell below 0% in the summer of 2011 and bottomed in August 2012 at -10%. Home prices followed the path of excess liquidity and were negative until the fall of 2012, turning up just after excess liquidity reversed higher. During the contraction of excess liquidity, GDP slowed markedly from over 10% to 7.6% in the third quarter of 2012. Between the summer of 2012 and the fall of 2013, excess liquidity improved from -10% to near zero. GDP growth stabilized just over 7%, but housing prices jumped again and were up by over 8% in late 2013. The run up in housing prices reflects the real estate bubble mentality that pervades China, as the increase in home prices was not fueled by excess liquidity.

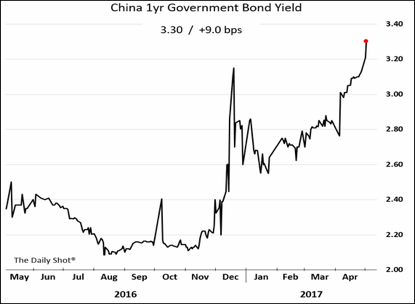

In August 2015, China began to devalue the Yuan which led to an outflow of capital. China’s foreign reserves fell from a peak of almost $4 trillion in July 2014 to $3.0 trillion in December 2016. To stem the outflow of reserves and stabilize the Yuan, the PBOC increased its Overnight SHIBOR rate from 2.0% in August 2016 to 2.85% in April. In order to manage the gradual devaluation of the Yuan, the PBOC was forced to buy Yuan, which had the perverse effect of tightening domestic monetary policy. To mitigate the negative impact from the Yuan’s devaluation in August 2015, the PBOC lifted the growth of M1 enough so that excess liquidity turned positive in early 2016. By March of this year, excess liquidity growth was up 17%, but has begun to slow to 15%, as higher interest rates begin to bite. As noted, housing prices were up 20% in the first quarter. However, with excess liquidity beginning to decline, it is likely that housing prices are peaking.

Despite the significant increase in excess liquidity since the summer of 2015, GDP growth has barely improved from the 6.7% rate in the second, third, and fourth quarters of 2016. This reinforces a point I’ve made before – increases in liquidity has led to banks rolling over debt for many companies unable to service their existing debt, rather than contributing to an increase in GDP. In the eight years since the financial crisis, China’s debt to GDP ratio has soared from 125% to 277%, but GDP growth has slowed. In recent years, each new dollar of debt has created a diminishing amount of GDP, so China’s reliance on debt to power economic growth is becoming an increasingly untenable option.

Chinese President Xi JinPing has instructed the China Banking Regulatory Commission (CBRC) to crack down on banks making highly leveraged bets on markets through popular investment products. In an April 10 seven page document, the CBRC also warned banks about the excessive use of short term funding that banks are relying on. In March, a number of rural banks failed to repay short-term loans to other lenders. To prevent the defaults from evolving into a full blown credit crisis, the PBOC injected $43.6 billion into the financial system on March 22.

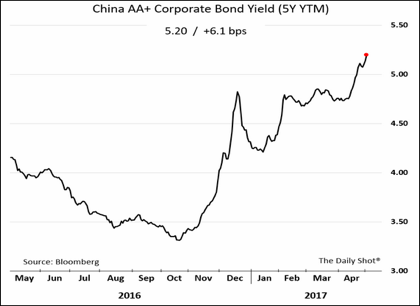

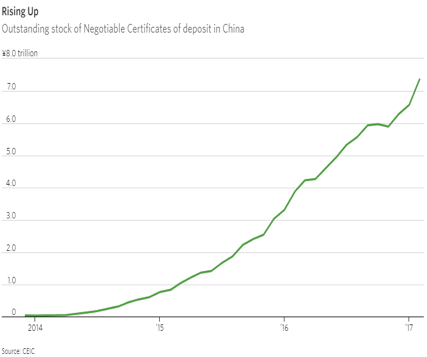

As discussed last month, small and mid-sized banks have been issuing Negotiable Certificates of Deposit (NCD), using the proceeds to invest in higher yielding longer term corporate bonds or government bonds. The banks begin to lose money if the yields on the government or corporate bonds they own rise. Since October, the Overnight SHIBOR rate has jumped from 2.1% to 2.9%. Certificates of Deposit in the U.S. are linked to the federal funds rate and Treasury bill rates, and short term Chinese NCD’s are tied to the Overnight SHIBOR rate and Chinese 1-year government bond yields. This has caused the rate on NCD’s to rise from 2.9% in October to 4.5% in late April. Last October, banks could issue NCD’s for 2.9% and use the proceeds to purchase AA corporate bonds maturing in 5 years yielding 3.3% to 3.4%. The spread would allow them to earn .4% to .5%. Since October, the yield on those corporate bonds has soared to 5.2%. The surge in corporate bond yields has caused the value of those bonds to fall well below the price the banks paid for them just six months ago. This suggests that banks that purchased these bonds with the proceeds from NCD’s have been dumping them at a loss, which helps explains why yields on corporate bonds have risen so much more than the increase in short term rates. The 1.85% surge in the 5-year AA corporate bond yield far exceeds the .8% increase in the Overnight SHIBOR rate.

Since 2013, the amount of NCD’s issued has rocketed from $89 billion to $1.65 trillion at the end of 2016. Since NCD’s are not booked as a loan, the banks have set aside little or nothing in reserves to buffer losses, as they would with a traditional loan. The NCD’s don’t appear as a liability and the corporate or government bonds purchased don’t show up as an asset on their balance sheet. This is similar to the Structured Investment Vehicles (SIV) set up by Citigroup and other large U.S. banks in the years leading up to the financial crisis. The SIV’s borrowed short term money and purchased longer term assets like mortgage backed securities. The Federal Reserve only became aware of these off the balance sheet entities in the fall of 2007, just as the financial crisis was gaining momentum. U.S. banks were forced to absorb the losses from the SIV’s, after the liquidity in short term funding markets disappeared and they were forced to sell the long term assets at a loss.

According to Fitch Ratings, at the end of 2016, NCD’s and other off balance sheet investments totaled $2.8 trillion and represented 26% of China’s GDP, up from 10% in 2013. NCD’s represented 19% of small and medium sized bank’s total assets. The good news is they only comprised about 1% of big bank assets.

The combination of tighter monetary policy and lower excess liquidity has caused the Shanghai Class A Index composite to shed more than 6% since its high in early April. In the process, the Index has closed below the uptrend support line from the lows in February 2016, which is not a good sign.

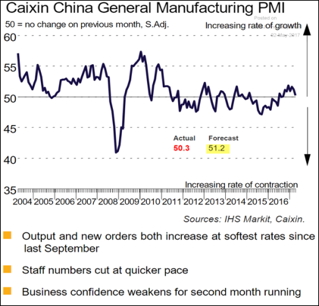

A dozen companies have defaulted on their corporate bonds, after they were unable to refinance bond issues at higher rates. The Caixin China General Manufacturing PMI dropped to a barely positive level of 50.3 in April, as both output and new orders increased at the slowest rate since September. The turn lower in excess liquidity suggests China’s property market is likely to soften in coming months, after rising 20% in the first quarter and lifting GDP.

Although President Trump would be loath to admit it, China has played a more significant role in the reflation trade than his election.

Over the past year, imports into China grew 15.3%, which shows that China has played an important role in the improvement in the global economy. In contrast, imports into the U.S. only grew 3.5%. According to Macquarie, China represents 27% of global investment, but only comprises 15% of the global economy.

If growth in China is slowing, its demand for raw materials would be expected to ebb. The recent declines in the prices of iron ore, steel, copper, and rubber suggests some air is coming out of the reflation trade. While the recent 10% decline in oil prices has more to do with U.S. shale production, and Russia failing to cut production as much as promised, a slowdown in China would negatively impact demand. A growth scare out of China is not being widely discussed in the financial press or by investment strategists. With hardly anyone paying attention, a slowdown in China could prove a negative surprise for the markets in the next few months. If the PBOC increases the Overnight SHIBOR rate more and Chinese bank regulators continue to clamp down on the wide spread shadow banking activity that pervades China’s banking system, the slowdown could become more serious.

The long term chart of copper suggests that a decline below $2.00 is possible based on the pattern. The peak in April 2011 occurred about six months after the peak in excess liquidity and coincided with a weakening in China’s property markets. The low in early 2015 in copper was preceded by a turn up in excess liquidity and subsequent rebound in home prices. The recent reversal in excess liquidity is likely to negatively affect the housing market, and could lead to a Wave 5 in copper below $2.00, or at least a test of that level. A close below $2.42 would indicate another leg of the decline was starting. If the past is any guide, the current depressive state of policy in China will be followed by another manic phase that will lead the PBOC to ease monetary policy and fiscal policy to become expansive. How long will the PBOC be willing to tap the monetary brake while the Chinese government pursues regulatory reform? I don’t know, but Guo Shuqing, Chairman of the China Banking Regulatory Commission said in April, “Strong medicine must be prescribed.” They certainly don’t want to kill the patient, so watching for injections of liquidity by the PBOC and other signs they are beginning to ease monetary policy would likely indicate the PBOC and the CBRC are ready to take their foot off the brake.

U.S. Economy

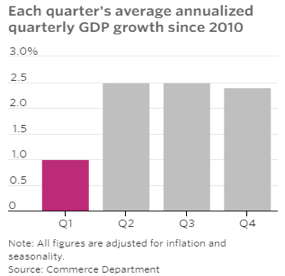

Growth slowed in the first quarter with GDP up only .7%. Since 2009, first quarter GDP has been far weaker than the average GDP growth in the other quarters, which suggests the seasonal adjustments used by the Commerce Department need adjustment. Some of the problem is likely due to the wide weather fluctuations the U.S. has experienced in recent years, from the Polar Vortex to the warmest February this year since 1954, which depressed utility output in the first quarter. Over the past eight years, the economy has grown at an average rate of 1% in the first quarter, while growing at a 2.3% rate in the remaining quarters.

Delays in refund checks from the IRS likely depressed consumer spending in the first quarter, which will kick start GDP in the second quarter as the IRS catches up. First quarter GDP was dinged by almost 1% as firms reduced inventories. If companies leave inventories unchanged in the second quarter, GDP will be boosted by 1%. Faulty seasonal and inventory swings have lifted estimates for the second quarter to 3.5%, with the Atlanta Fed’s GDP now forecasting growth of 4.2%. These estimates may prove too optimistic.

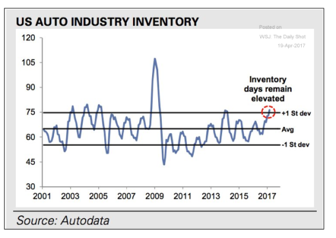

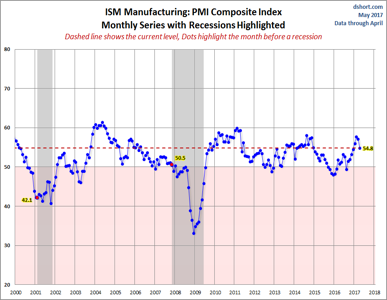

Consumer spending in the first quarter grew at the slowest pace since 2009. Tardiness by the IRS in getting refund checks sent out may explain a portion of the spending shortfall in the first quarter, but certainly not all of it. Car sales in April were 4.7% below a year earlier, according to AutoData. I first flagged the coming slowdown in auto sales in the November Macro Tides. “The increase in lending standards by auto lenders will lower sales in coming months, and falling used car prices will pressure new car prices. The coming slowdown in car manufacturing will turn what had been a positive growth sector into a modest drag on GDP growth in coming months.” With sales down, there are now more than 1 million unsold cars sitting on dealer lots. According to J.D. Power, the slowdown in sales has occurred even though discounts are nearing an all-time record of $4,000 per car or truck sold. The slowdown in the auto sector may be spilling over into the broader economy. The Institute of Supply Management’s Purchasing Managers Index of manufacturing fell to 54.8 in April from 57.2 in March the second straight monthly decline. There may be more weakness to come as the new order index fell sharply from 64.5 in March to 57.5 in April. The Employment component dropped to 52.0 from 58.9. Maybe some of the optimism generated by Trump’s election is melting away. (ISM Chart compliments of Doug Short, Advisor’s Perspectives)

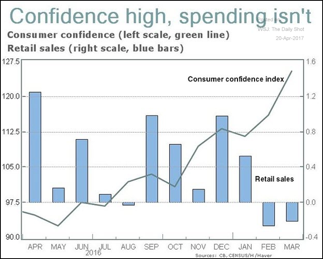

Consumer confidence soared after the election but consumers haven’t gotten off the couch to hit the shopping malls. Retail sales declined in February and March, which the decline in auto sales contributed to. But there may be something bigger going on, as the personal savings rate climbed to 5.9% in March up .5% since December. The surge in consumer confidence indicates that consumers are expecting the economy to improve and more importantly benefit them directly. The reality is that nothing tangible that is positive has taken root. Although the Republican controlled House passed their version of health care reform, it raised more questions and anxiety since health care reform is months away from becoming law. Health care is important since it represents 17% of GDP, and will become increasingly important due to demographics as the Baby Boomers age and require more medical care. But the majority of Americans get their health care through their employer, so the actual repeal of the Affordable Care Act won’t affect them as much as the promised middle class tax cuts. Treasury Secretary Mnuchin indicated that tax reform and the tax cuts are not likely to pass Congress until after the August recess. The weakness in consumer spending may have more to do with the long delay in consumers realizing the increase to their net pay from tax cuts, than the delay in the IRS processing refund checks. Second quarter GDP may get a modest lift from the delivery of refund checks, but consumer spending may be held captive until Congress passes the tax cut legislation. After 16 years of no growth in median income, “Show me the money” is the mindset of many consumers.

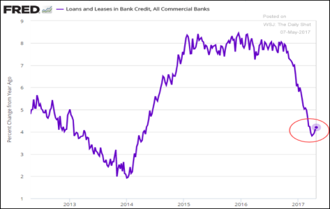

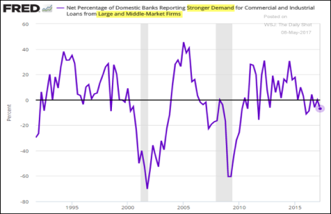

Consumers may not be the only group keeping their wallets in their pocket. Small and large business confidence jumped after the election, as the prospects of less regulation and lower taxes raised expectations of better times to come. After years of tepid business investment, first quarter GDP was boosted by a 9.4% increase. This is encouraging, but the sharp deceleration in Commercial and Industrial loans at commercial banks suggests the majority of companies have adopted a wait and see attitude. The annual growth rate in C&I lending has fallen off the table and is up only 4.2% from more than 8% just before the election. Companies are holding off until they understand how much corporate taxes will be lowered, and what if any incentives will be available for targeted investments. Weak demand for C&I loans is another symptom of the dearth of business investment in recent years.

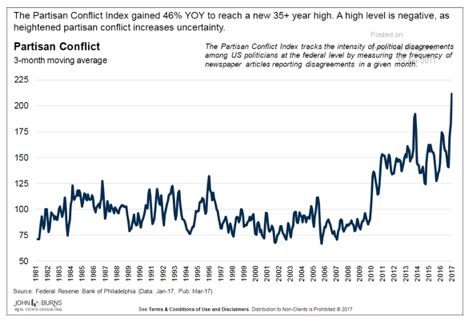

The prospect of fundamental changes to the tax code have raised hope and confidence, but also provided a good reason not to act. This is another reason why the rebound in the second quarter may not measure up to the GDP estimates that helped investors dismiss the slowdown in the first quarter. The trigger for consumers to increase spending and companies to ramp up business investment is thus dependent on Congress to work together. Since 2010, members of Congress have done a far better job of disagreeing with one another than actually doing the work of the people. The Index of Partisan Conflict has tripled since the early 1990’s, and doubled since 2010. Surfing between CNN, MSNBC, and Fox and listening to the less than enlightening discussions on health care, tax reform, and how to improve economic growth, suggests the bull market in partisanship is alive and well. There is a good chance that investor’s patience will become impatience, as Congress fumbles and bumbles without giving investors what they have already priced into the market – tax cuts and better economic growth.

Federal Reserve

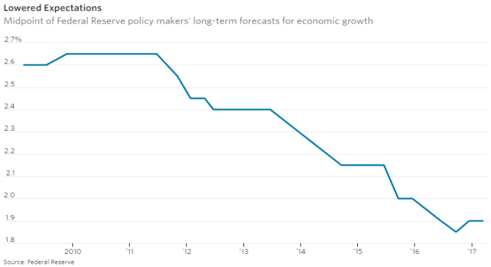

Investor’s willingness to give the first quarter stumble in the economy a pass was reinforced when the Federal Reserve said the slowdown was “transitory”. Who better than the Fed to tell investors what they want to hear, notwithstanding the Fed’s less than stellar track record? As we now know, GDP growth since the recovery began has averaged just 2.0%. The Fed was too optimistic in every year since 2010.

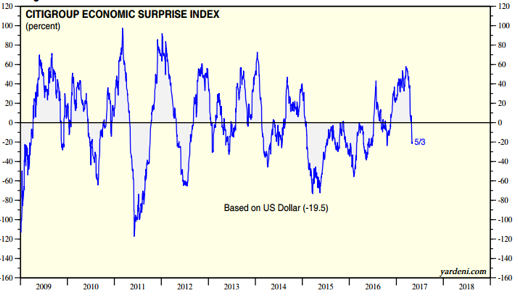

The Citigroup Economic Surprise Index has plunged from +58 to -19 over the past eight weeks as a majority of economic reports came in less than estimated. The weakness in the first quarter has carried over into the beginning of the second quarter. The trend of reports coming in less than estimated could continue since auto sales and production are not likely to pick up in the second quarter. The lack of legislative progress on health care and tax reduction for consumers and business is likely to deflate the surge in confidence, and do little to improve consumer spending or business investment in the second quarter. If growth in China slows as I expect, and U.S. GDP growth doesn’t show signs of rebounding to the 3.5% rate economists are forecasting, the potential of a growth scare or disappointment could materialize in coming months.

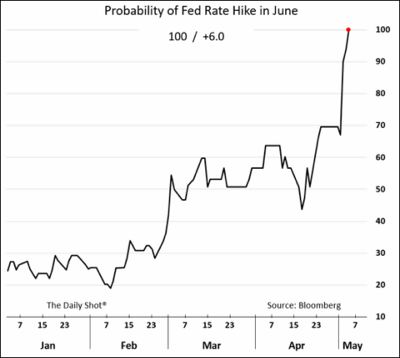

After the FOMC meeting on May 3, the probability of a June rate hike zoomed to over 90% and hit 100% after the strong employment report. The Fed certainly wants to raise rates so they have more leverage with the federal funds rate when the next recession develops. If the rebound in the economy doesn’t confirm forecasts, and Fed presidents continue to give speeches preparing the markets for a June hike, the equity market could correct modestly, while Treasury bond yields dip. If the economy is so weak the Fed is not able to increase the federal funds rate in June, the equity market could be vulnerable to a deeper correction, and Treasury yields could challenge the lows of mid April.

Emerging Markets

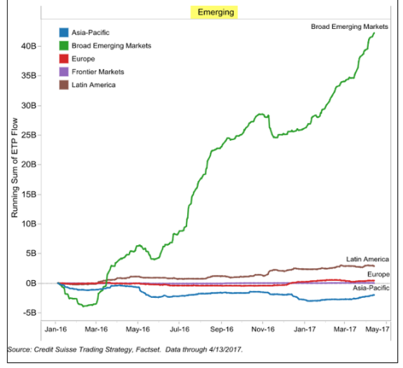

The coming slowdown in China has the potential to cast a pall over the enthusiasm toward emerging markets that has taken hold of investors since early 2016. This is clearly visible in the money flows into Emerging markets which have topped $40 billion. Whenever an asset class garners too much favorable press and a big surge of inflows, a yellow light begins to flash. The story line embracing the emerging markets was driven by three factors. On a valuation basis, the emerging markets were cheap relative to the developed markets in general and the U.S. stock market in particular. Based on the Cyclically Adjusted Price Earnings ratio (CAPE), emerging markets were half as expensive as the U.S. market. This attracted value oriented investors. Emerging market currencies had collectively experienced large declines relative to the dollar between May 2014 and an initial peak in January 2016, with a modestly higher peak (2%) in December 2016. The rally in emerging market currencies reduces the burden of dollar denominated debt, which totals more than $10 trillion. Many emerging market economies are dependent on the prices of raw materials, which had fallen significantly from a high 2011, and plunged further as oil prices dropped from over $100 a barrel in mid 2014 to a low in the first quarter of 2016. From that first quarter low, most commodity prices have recovered which improves the cash flow for commodity dependent countries.

Since its low in February 2016, the Emerging Market ETF (EEM) has rallied almost 50%, so the valuation argument isn’t quite as compelling as it once was. Technically, EEM is overbought and there are momentum divergences, even as EEM has made higher highs during the past month. After rebounding smartly, a number of EM currencies have begun to roll over, so the tailwind from an appreciating currency could be less in coming months. The long term uptrend in the Trade Weighted Dollar index is still intact, so a rebound in the Dollar from the rising support line could lead to a decline in EM currencies in the short term. As discussed, China has been tightening credit and its economy is likely to slow in coming months. The demand for many raw materials has already softened, and a number of raw industrial commodities have experienced double digit declines.

The correlation between the Emerging Market ETF (EEM) and the China ETF (FXI) has been tight for years, with both making highs and lows coincident with each other, even if the magnitude of the rallies and declines has varied. In the last two months, FXI has declined while EEM has continued to go up. (Chart below) Something will soon change. Either China rallies or EEM corrects to narrow the performance gap. A rally in the Chinese stock market and FXI seems less likely, if China continues to slow in response to higher interest rates and tighter monetary policy. Eventually, investors will realize that emerging market economies will not be immune to a slowdown in China, leading to a correction in EEM.

Eurozone

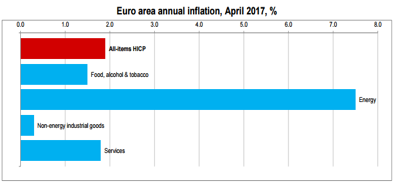

GDP growth is running close to 2.0% in the Eurozone, elections in the Netherlands and France have lessened the rise in populism and the concern that stress fractures within Europe would increase. Inflation is near the ECB’s 2% target, and business and consumer confidence continues to increase. (EU GDP is reported as a quarterly figure and not annualized as is the practice in the U.S.) These improvements are somewhat in conflict with the ECB continuing its QE program purchases of government and corporate bonds at a monthly clip of $60 billion. At the last ECB policy meeting on April 24, Mario Draghi said underlying inflation in the Eurozone was too weak and the bloc’s economy still needed ‘very substantial’ support from the ECB. Given his comments, Draghi’s opinion is not likely to change much prior to the next ECB meeting on June 8.

On the surface, Draghi’s comments appear to be a denial of what is obvious – economic growth has improved and inflation is near the ECB’s target. But a large part of the increase in inflation is from the big recovery in oil prices, which is the main reason EU inflation is near 2.0%. The rate of change in oil prices will gradually lower the EU’s inflation rate progressively below 2.0% in coming months.

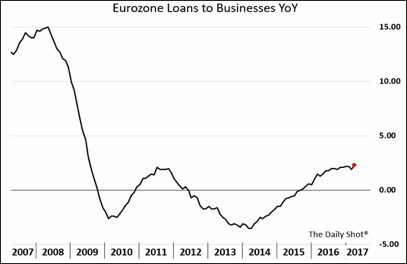

In the U.S., bank lending represents 35% of credit creation. In the EU, bank lending comprises more than 70% of credit creation, so the EU is far more dependent on a healthy banking system. As banks in the EU have struggled to repair their balance sheets since the financial crisis, bank lending has suffered. Bank lending contracted from mid 2012 until late in 2015. The weak level of bank lending is one of the primary reasons why economic growth in the EU has averaged 1.4% less annually than in the U.S. since 2009, according to the IMF. Bank lending is on the mend but is still well below the levels in 2007 and 2008, before the financial crisis. The European banking system is still burdened with $1 trillion of nonperforming loans and many banks need to improve their capital ratios in order to meet the Basil III standards by March 2019. This suggests further improvement will be moderate, and not likely to return to 2007 levels for a number of years. Of the $1 trillion in nonperforming loans, more than $300 billion is concentrated in Italian banks.

The ECB’s QE program has been responsible for keeping bond yields lows throughout Europe, including Italy. Before the end of 2017, the ECB will likely reduce the amount of its monthly purchases from $60 billion a month. When the bond markets in Europe begin to anticipate the reduction in the ECB’s buying, bond yields in Europe will likely go up. Since global bond yields are linked, any meaningful increase in yields, especially in German 10-year Bunds, will cause a rise in Treasury bond yields in the U.S. The first warning will come when the yield on the German 10-year Bund closes above the highs in January and March at .50%.

While the election in France may be over, the problems of economic growth and high unemployment will remain a serious challenge in the second largest country within the EU. The new president is 39 years old and is not part of any of the established political parties in France. President Macron will find it difficult to get support from the philosophically different parties necessary to pass the reforms he seeks, even though they are sorely needed. GDP growth has averaged less than 1% since the financial crisis and France’s unemployment rate is still over 10%. Government spending represents 57% of France’s GDP, and Macron would like to shave that to 52% by reducing civil services. He wants to reduce the power the labor unions exert on hiring and firing of private sector workers and France’s pension system, which offers more protection to unionized workers than the self-employed and small entrepreneurs. In return for these changes, Macron has pledged to keep the minimum retirement age at 62 and the 35 hour workweek. The only question is how long before labor unions to mount national strikes in opposition to the changes Macron seeks to make. As it becomes apparent during the next twelve months that substantive change in France is not going to happen, the enthusiasm so widespread now about EU growth will fade.

Jim Welsh

© Marcro Tides