Macro Tides

The Latest Technical and Chart Developments

This article explores the tension between individual economic outlooks and the institutional desire for collective stability in a highly scrutinized environment.

From Tariff Angst to Optimism

In the last three months tariff news has whipped financial markets around remarkably in response to President Trump’s ever changing tariff policies. The most pronounced reactions were concentrated in the US stock market.

Monthly Global Economic Report

While the economy helped President Trump win a second term, it also created expectations that could prove difficult to meet.

Monthly Global Economic Report

The expert and you are in a car and the expert is driving. After awhile, you notice that the expert is driving the car by looking through the rearview mirror. Concerned you ask him why he’s not looking ahead as he drives.

Economic Carbon Monoxide

Lending standards are a lot like carbon monoxide since they operate in the back ground. When the Senior Loan Officer Opinion Survey (SLOOOS) showed that banks significantly increased lending standards in the third quarter, no one on Wall Street noticed.

The FOMC Won’t Blink

As expected and discussed in the January Macro Tides the December Consumer Price Index (CPI) dropped below 7.0% falling to 6.5% from 7.1% in November.

Forward Guidance Failures

One of the themes I’ve discussed in recent months is the disconnect between a 40 year high in inflation and the lack of experience money managers have in understanding the monetary policy required to deal with such high inflation, including managers with 25 to 30 years of experience

FOMC Inflation Test Coming

In January Goldman Sachs projected that the FOMC would increase the federal funds rate at every other meeting (each meeting is 6 weeks apart) starting with the March meeting.

FOMC Tightens as Economy Slows

In 2021 the FOMC refused to accept and acknowledge that inflation was getting worse in the second and third quarter and continued with its monthly purchases of $120 billion in Treasury debt and Mortgage Backed Securities.

Is the FOMC Impotent?

In March 2020 the Federal Reserve was able to use old and new tools to manage the unimaginable – a Pandemic. The Fed stabilized the Treasury bond market and the municipal bond market through its purchases and back stopped government loans to small and medium sized businesses to keep them from going under.

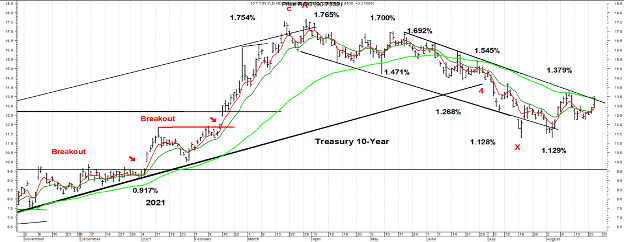

What’s the Message from Treasury Yields?

The 10-year Treasury yield finished 2020 at 0.917% and then climbed to 1.765% before topping on March 30. The 30-year Treasury yield rose to 2.505% on March 18 after ending 2020 at 1.646%. In the January 11 Weekly Technical Review (WTR) I noted that Treasury yields had broken out to the upside and that the 10-year Treasury yield would likely climb to 1.75% to 1.95% in 2021. “Treasury yields broke out on January 6 as expectations of more fiscal stimulus and technical selling kicked into gear. At some point in 2021, the 10-year Treasury yield could spike up to 1.75% to 1.95%.”

Transitory Inflation? Not so Quick

Transitory is defined as being of brief duration, tending to pass away and not persistent

The Times Are a Changing

Some changes unfold over time and it’s possible to see them coming. There are demographic changes coming in the next decade that will change the direction of the U.S., since the Silent generation and the Baby Boomers hold a different view of government than Gen Z’s and Millennials.

Monthly Global Economic Report

Some changes unfold over time and it’s possible to see them coming. There are demographic changes coming in the next decade that will change the direction of the U.S. since the Silent Generation and the Baby Boomers hold a different view of government than Gen Z’s and Millennials.

Safety Net or Stimulus

In response to the COVID-19 pandemic governments imposed shelter in place rules for their citizens and issued orders to close all but essential business in their country. The collective impact resulted in an unprecedented global plunge in economic activity that threatens the existence of many small and medium size businesses...