The global financial crisis affected many countries' economies in different ways. What made the difference was how each country's policymakers, banks and financial companies responded as the crisis unfolded.

Policymakers in the US and the UK put their nations on the right path and got their banks back on track with aggressive responses – including letting some institutions fail, forcing relief on others and implementing strict new regulations. Most European countries, however, were indecisive about pumping in sufficient new capital and implementing reforms, and their banking problems still linger. Greece is a case in point, and the country continues to struggle today.

Greece: A case study in taking the wrong path

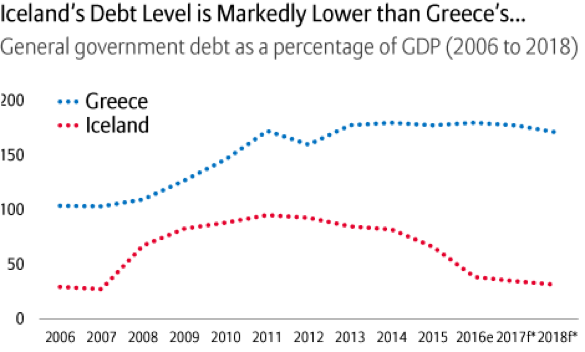

Greece is one of the worst-off European nations economically. Its bank and debt crisis continues, yet its politicians cannot admit the plain truth that Greece's debt – more than 175% of its gross domestic product in 2015 – is unsustainable and must be written off.

Unfortunately, the austerity measures implemented by the European Union and International Monetary Fund have been insufficient. Instead, these institutions pretend the situation is sustainable and provide more loans so they can receive interest on the existing debt mountain. No wonder the IMF is desperate to extricate itself from this situation.

So how did Greece get here? The financial crisis of 2007-2008 exposed fault lines that already existed in Greece's economy and triggered a chain of inadequate responses:

- International lenders, mostly banks, had extended too much credit to Greece.

- Politicians nationalized Greece's debts, absolving bank lenders of any losses rather than dealing directly with their solvency issues.

- This created huge liabilities on the balance sheets of the EU and the European Central Bank.

- The EUR 86 billion loan rescue package imposed by the ECB and IMF forced Greece to impose austerity measures and pay back EUR 7 billion per year for its debts.

Yet with debt forgiveness politically unacceptable to most creditor countries in the EU, Greece is forced to endure a charade of economic sustainability, and its people are suffering a depression far worse than the US endured in the 1930s. A stagnant economy, low investment, low employment and poor prospects are driving domestic capital out of the country instead of attracting it in. Political corruption is an ongoing problem, and the government still relies on tourism to drive trade and create jobs, rather than stimulating other industries. Even worse, Greece's situation appears set to continue until its debt is forgiven, it leaves the euro or it strikes oil – at least figuratively speaking.

There are certainly reasons why many creditors are unsympathetic to Greece's situation. According to some estimates, Greece has a cash economy that accounts for around 25% of its gross domestic product, and tax evasion and smuggling could subtract another 6% to 9%. Given that 88% of government revenue comes from taxation, Greece desperately needs to find a way of bringing this economic activity onto the books – but it hasn't found a way to capture it or make its citizens pay their bills:

- Nearly 3 million people (around half of Greece's tax-paying population) declare less than EUR 12,000 in income, which is tax-free. Of course, Greece also has an unusually big farming sector by European standards, and many of its people struggle to make a living.

- Another 2.8 million Greek citizens paid a collective EUR 60 million in taxes – slightly more than EUR 20 per person.

- Corporations are not pulling their weight either: 220,000 companies declared less than EUR 1.2 million in annual profit in 2011.

- More than 61% of the country's corporate taxes are paid by a total of only 900 corporations.

The net result is that not only do taxes remain unpaid, but Greece's bigger issues remain unresolved, exacerbated by a lack of leadership from the country's politicians. However, as Iceland demonstrated, the situation does not have to be this dire.

Iceland: A case study in tackling issues head-on

Iceland was one of a handful of countries that addressed their problems directly and proactively in the wake of the financial crisis. Of course, Iceland had more flexibility than other European nations – it isn't part of the euro zone and has a population of 320,000, vs. 10 million for Greece – but its aggressive response was nonetheless notable. The small island nation punished domestic and foreign creditors alike, allowed its currency to fall – forcing a rapid internal devaluation – and nationalized its banks.

The first few years of Iceland's road to recovery were full of potholes: GDP collapsed, inflation rose, wages fell in real terms and international lenders cried foul. The nationalization of its banks was also a brutal process; only domestic entities were protected, and international interests were trapped behind capital controls that served only Iceland. Moreover, high levels of inflation prompted the central bank to lift interest rates to a punitive peak of 18% in 2009. Fortunately, the government sought to help out Iceland's citizens by using fiscal policy to lower consumer debts and improve social support.

Ten years later, however, and Iceland is close to reaching its goals. It has repaid more than USD 60 billion of its foreign debts, returning to a much safer pre-crisis level. The current account surpluses generated by the fall in Iceland's currency, combined with the benefits of having solvent nationalized banks, have allowed the economy to rebalance and begin to grow again.

Indeed, economic momentum is improving rapidly and attracting back international investors, as Iceland expands its primary industries away from fishing and tourism and toward renewable energy and information technology. The normal economic feedback loops are already back at work as well, with employment rising alongside wages. Capital controls have also been lifted to allow Iceland back into the global economy – its problems fixed and its lessons learned.

Which road will Greece take?

Europe and Greece should follow Iceland's lead and let the markets and capitalism run their course. It will be painful, but the results should be worth it, as two head-to-head comparisons make clear:

- Debt to GDP – Greece's ratio shot up from 103% in 2007 to 175% in 2015 and still hasn't recovered; meanwhile, Iceland's enviable 38% ratio in 2016 is close to pre-crisis levels.

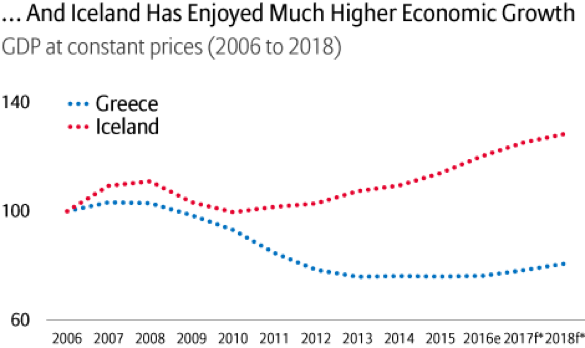

- GDP at constant prices – Since 2008, negative GDP growth and high inflation have shrunk Greece's real GDP and its economy. Meanwhile, Iceland's economy has recovered well despite a brief period of negative GDP growth between 2008 and 2010.

At this stage, however, it is unclear whether Greece or its creditors are prepared to make the hard decisions. Negotiations between Greece and its international lenders have become more intense, but the parties have different views on Greece's fiscal progress and market reforms. For his part, EU Council President Donald Tusk has tried to be reassuring, acknowledging that "The sacrifices of the Greek citizens have been immense. One thing must be clear – no one intends to punish Greece. Our goal is only to help Greece."

The danger, in our view, is that if the EU provides additional rescue funds, they won't help. What is needed are real structural reforms and less-distortionary monetary policy – rather than allowing Greece to continue to borrow against its future.

Source: European Commission as of 3/7/17; estimates and 2017-2018 forecasts by the European Commission.

Follow Us on Twitter

For more investment insights and market perspectives from our global research network, follow @AllianzGI_US on Twitter or visit us.allianzgi.com.

Important Information

The material contains the current opinions of the author, which are subject to change without notice. Statements concerning financial market trends are based on current market conditions, which will fluctuate. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities. Forecasts and estimates have certain inherent limitations, and are not intended to be relied upon as advice or interpreted as a recommendation.

Past performance of the markets is no guarantee of future results. This is not an offer or solicitation for the purchase or sale of any financial instrument. It is presented only to provide information on investment strategies and opportunities.

Allianz Global Investors Distributors LLC, 1633 Broadway, New York NY, 10019-7585, us.allianzgi.com, 1 800 926 4456.

162282