Why we're constructive on oil

Not many investors have been bullish on the price of oil recently, but Allianz Global Investors has had a constructive view of the industry for the past 12-18 months. Now that both members and non-members of the Organization of the Petroleum Exporting Countries (OPEC) have renewed their commitment to limit production in an attempt to boost prices, it's a good time to review the prospects for oil. Here are five reasons why we think the price of oil will turn around – and why investors should consider positioning themselves to take advantage of the opportunity.

1. Global demand for oil is reassuringly stable

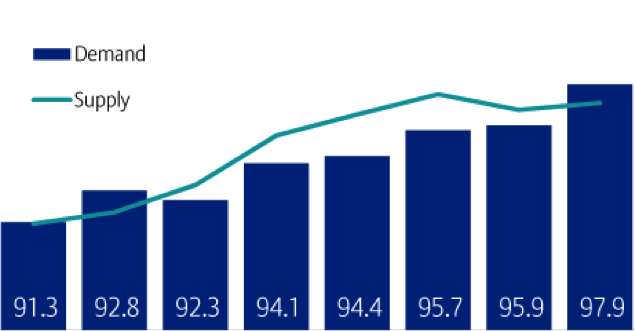

Although the International Energy Agency (IEA) lowered its predictions for oil-demand growth in 2017 from 1.4 million barrels per day to 1.3 million, global demand has remained reassuringly stable. At the end of 2016, the world consumed slightly more than 97 million barrels per day, making the IEA's modest downward revision look relatively inconsequential and still representative of healthy growth. At the same time, oil inventories have been decreasing and global economic growth is buoyant. Taken together, these factors should underpin a steady demand for oil despite higher prices.

It is important to note that a rising oil price has a downside as well, given that it functions as a tax on consumers and the global economy in general. Higher prices may crimp consumer spending and drive inflation through the economy. This effect can be amplified by currency movements globally, particularly given that oil is often priced in US dollars. For example, the post-Brexit fall in the British pound had the effect of re-pricing oil to the equivalent of $70 per barrel by the time it reached consumers at the pump.

Energy production growth is slowing

Percentage of energy production (million tons of oil equivalent) growth per decade

Source: International Energy Agency as of 12/31/15.

2. Multiple factors will constrain the oil supply

Global supply levels became much more difficult to assess in November 2016, when members and non-members of OPEC agreed to reduce production as a way to drain the oversupply of oil and boost prices. On May 25, this agreement was extended through March 2018. While analysing the actual effectiveness of this agreement will continue to be challenging, there is little doubt that it has improved the supply/demand balance.

Moreover, many OPEC nations are effectively petro-states that derive most of their government financing through the taxation of oil and gas revenue. When the price of oil is threatened, their institutions become vulnerable – and given that oil prices have been low for some time, many of these countries have experienced serious issues:

- Mexico, already under pressure from the trade and immigration policies of President Donald Trump, has seen its revenues and financial flexibility drop sharply as production and profits fall.

- Venezuela, which produces around two million barrels of oil per day, has struggled with hyperinflation and appears on the verge of collapse as its economy runs out of cash, credit and food.

- Nigeria is suffering not only from a weak, inflation-prone currency and economy, but from serious security problems in its oil-producing delta regions.

- Oil production across the Middle East is also being threatened by continuing destabilization in countries such as Libya and Iraq – which may get worse before it gets better.

The fragile state of many petro-states is one of the reasons why OPEC is aiming to boost prices by cutting production. These issues have also ratcheted up geopolitical tensions – already at an elevated level thanks to US airstrikes on Syria and missile testing in North Korea. If markets become increasingly nervous, we expect to see a further premium on prices.

The supply/demand imbalance may be shifting

World oil supply/demand in millions of barrels per day

Source: International Energy Agency as of 12/31/16.

3. New discoveries are dwindling

For decades now, discovering new oil fields has grown increasingly difficult. As a result, the global economy is essentially relying on a few old and aging mega-fields to produce the supply of oil it needs. In fact, aside from the US shale-oil industry, which has made significant advances in recent years, few energy companies have been investing more in finding new oil fields. Many companies also enacted significant capital-expenditure cuts in 2015-2016, which meant they had even less to spend on oil discovery. They have instead focused on cost control and cash generation. If this capital discipline remains in place, and if the price of oil stays stable, shares of energy companies could move higher – particularly given that a fluctuating oil price helped keep valuations quite low for years.

Some energy companies have prioritized "brownfield" developments that attempt to eke out more production from existing fields using cost-effective technologies. These efforts can help companies achieve quick cash-flow boosts, but the stock of these fields is increasingly limited. Indeed, a recent study from Rystad Energy suggests that, across the industry, reserve-replacement ratios have fallen to their lowest level in 70 years. While there may be no immediate impact, the effects of this fall in volumes could be felt on global supply over the long term. This figure is unlikely to pick up if there is no major investment increase.

In our view, this cutback in oil discoveries will start to filter through by 2019 and will noticeably reduce supply. For investors, it means the market could be looking at another oil-price spike not too far in the future.

4. The US shale industry has problems

In recent years, new technologies and drilling techniques contributed to a US shale-oil boom that significantly boosted supply and helped drive down oil prices. When OPEC nations restricted their oil production late last year, largely in an effort to combat low prices, US shale producers seized the opportunity to ramp up their output and exports. This further altered the balance of supply and demand in the global oil market.

Shale oil is a clearly profitable source of production for US energy companies, but it is important to note that the US is still a net importer of oil and other petroleum products. Moreover, the US shale-oil industry as a whole is grappling with some significant issues:

- Many US oil producers are still cash-flow negative, relying on funding from banks and investors to provide enough cash to stay in business.

- The robust pace at which drilling activity has increased over the past year is bound to decelerate due to growing constraints on available personnel and equipment.

- As quickly as the shale boom started in 2012, the industry suffered a sudden recession in 2014. Consequently, much of the talent, skills and capacity used in the previous boom are now gone. So even though today's production levels are high, today's unsustainably low costs are beginning to increase rapidly.

President Trump is certainly looking to support US domestic production and is less environmentally focused than his predecessor, but it is unlikely his policies will have much impact on the location and pace of US drilling. For investment and employment to rise, the US shale industry needs higher and more stable prices. The general breakeven point is estimated to be in the $45-50 per barrel range – but only for the premier acreage. That leaves the large number of less productive fields more vulnerable.

5. Domestic production is falling in a booming Asia

Elsewhere in the world, China's domestic production is also in decline, and additional falls are expected. At the same time, China's energy demands are growing along with its population size. This suggests that China will increasingly continue to rely on the global markets to add to its supply. In addition, India, Indonesia and other Asian nations are also seeing production declines even as regional economic growth is expected to move significantly higher overall. This should lead to increasing demand from the global markets.

Today's low prices make oil an attractive opportunity for investors. On May 15, Saudi Arabia and Russia announced an agreement to extend production cuts through March 2018 in an attempt to get surplus inventories under control. After this announcement, oil prices rose more than 3%, to $52.52 per barrel. Only 10 days later, OPEC and non-OPEC nations agreed to extend their arrangement to cut production, and we shall see if the price of oil responds accordingly over time.

Eventually, of course, these OPEC restrictions will be unwound once inventories are reduced to normal levels, which should result in a more natural supply/demand balance. And as we have discussed, geopolitical tensions alongside a lack of exploration and new project sanctions appear set to reduce supply globally. This combination of factors should lead to historically low global spare capacity, which could lay the foundations for an oil-price spike.

We also expect to see excitement in the marketplace surrounding the impending initial public offering of Saudi Aramco, which is expected to be valued as one of the top 10 companies in the world. This could have a halo effect on the markets.

In recent months, the oil price has been depressed because the market did not see the quick inventory declines it was looking for; as a result, speculative long positions contracted. We believe this happened at least in part because of a lack of good data about global inventories, which meant the markets focused only on US numbers. Either way, inventories would normally be building during this period due to seasonality, and instead they are falling. We believe this contributes to an attractive longer-term opportunity for investors.

Follow Us on Twitter

For more investment insights and market perspectives from our global research network, follow @AllianzGI_US on Twitter or visit us.allianzgi.com.

Important Information

The material contains the current opinions of the author, which are subject to change without notice. Statements concerning financial market trends are based on current market conditions, which will fluctuate. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities. Forecasts and estimates have certain inherent limitations, and are not intended to be relied upon as advice or interpreted as a recommendation.

Past performance of the markets is no guarantee of future results. This is not an offer or solicitation for the purchase or sale of any financial instrument. It is presented only to provide information on investment strategies and opportunities.

Allianz Global Investors Distributors LLC, 1633 Broadway, New York NY, 10019-7585, us.allianzgi.com, 1 800 926 4456.

167948

© Allianz Global Investors

Read more commentaries by Allianz Global Investors