SUMMARY

- Will High-Rises Come Down to Earth?

- Europe Contemplates Common Debt

- States are Rising Up to Retirement Challenges

A swagman waltzing to Ballarat to join the Australian gold rush of 1851 navigated using the stars and his senses. My recent trip to the area with friends was directed by a GPS navigator, but we nonetheless found ourselves misguided on more than one occasion. We found no gold, and we barely found Ballarat. So much for modern technology.

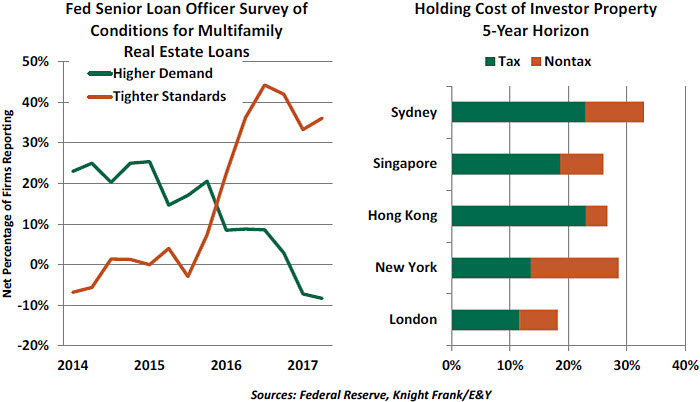

In the present day, speculators have been waltzing to Australia searching for gold in residential real estate. Property values have escalated briskly, encouraging overdevelopment and pricing residents out of the market. The authorities are now engaged in a campaign to ease conditions without having them crash.

With more traditional commodities also in decline, Australia’s world-record streak of 26 years without a recession may be at risk. The situation Down Under is not unique, but having company in a community of overheated property markets is cold comfort. How this community works through its challenges will have an important influence on global economic performance.

Thirty years ago, apartments seemed passé. Post-war generations favored suburban life and single-family dwellings. Today, by contrast, apartments are all the rage. Young professionals favor proximity to work, to play, and to one another. Apartments are also popular with another population: investors and bankers. The collective enthusiasm has raised property prices in some markets to stratospheric levels.

Residents in markets especially popular with investors are forced to take out huge mortgages if they seek to own property. Whereas households in the U.S. and the U.K. have reduced their leverage in recent years, Australia and Canada have seen personal leverage continue upward. Most observers agree this trend is not sustainable.

The banking systems in Canada and Australia take justifiable pride in their credit risk management, which allowed the two countries to come through the 2008 financial crisis in relatively good shape. But homeowners in both countries have found access to aggressive financing, including subprime and interest-only loans. These products served as dangerous accelerants during the 2008 crisis in the U.S.

Interest rates in most markets remain fairly low, limiting the interest burden for debtors and upholding credit quality. But low interest rates have also sent investors around the world searching for yield, and many have turned to apartments to satisfy their craving. Some are seeking rental cash flows, some are seeking price appreciation, and some are seeking assets that are not denominated in their local currency.

In many of the cities I visited during my recent swing through Asia and Australia, stories of investors from China arriving by the busload to buy high-rise units were common. While China has enacted further restrictions on capital flight, a favored few still seem to be able to bid aggressively on foreign real estate.

Authorities seeking to control the situation are confronted with a series of challenges. Since the marginal purchaser in the most popular property markets does not require leverage, raising interest rates on home loans provides less of a deterrent. Sweden attempted to address its property excess by increasing interest rates in 2011, but had to retreat in the wake of unsatisfactory results.

Attention in many regions has therefore turned to a cocktail of macroprudential policies. Financial supervisors have taken aim at property developers, warning banks to limit leverage and underwrite especially carefully. In the U.S., the Federal Reserve has used its ways and wiles to chill conditions surrounding multifamily lending.

The wisdom of this strategy is not immediately apparent, as restricting supply would tend to increase prices, not reduce them. Those hungry for property would merely increase their bidding for existing units.

Fiscal authorities have been adding layers to their property tax systems, targeting foreign purchases and adding special levies for vacant units, multi-unit ownership, and property “flipping.” All of these points were included in a

plan introduced to curb real estate excesses in the Toronto area. A global summary of the costs of real estate speculation can be found

here.

These tools all work in theory, but it remains to be seen whether they will work in practice. There is little data to calibrate how high property taxes need to be in order to bring about a modest (but not severe) correction in the market.

The most critical test for macroprudential management of property markets is underway in China. Domestic investors are largely confined to investing in domestic assets, fueling huge rises in apartment prices and construction. Recent curbs have reduced rates of price increase to “only” 15%. There is more work to be done in China, and success is by no means assured.

Apartments and commodities have a lot in common. Excavation can lead the way to new supplies, which are mostly homogeneous. Both are the object of global demand. Both can be the subject of consumption and speculation. And both can be the subject of irrational exuberance.

One of my clients in Asia said it eloquently: We need to find a way to make apartments primary residences, as opposed to an asset class. There is no GPS available to guide this transition, so policy makers will have to rely on their senses and hope for a little luck from the heavens.

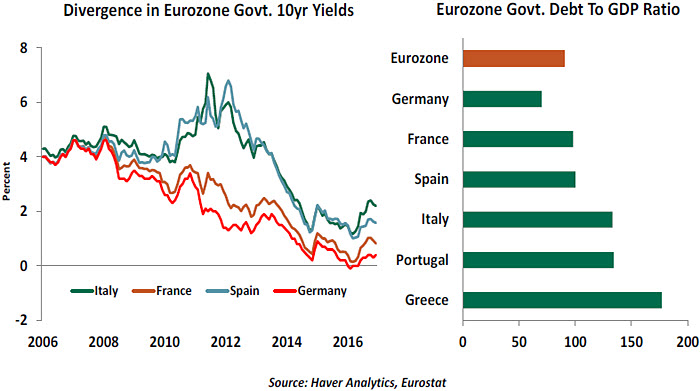

Everyone Into the PoolLast week, the European Commission (EC) came out with a new proposal to address the financial fragmentation within the European monetary union. It envisions the creation of sovereign backed securities, which would essentially be a bundling of individual sovereign obligations into a single European bond. The idea has much to recommend it, but needs some additional work.

The plan seeks to boost demand for debt issued by weaker governments by including it within a basket of sovereign bonds that includes bonds issued by stronger countries. Demand for the new securities could come primarily from Europe’s banks and the ECB, pending rulemaking that makes them eligible to satisfy statutory requirements.

More crucially, the plan seeks to break the link between the sovereign and the domestic banking system, the so-called “doom loop” that has surrounded stressed European countries. Whenever the sovereign debt comes under stress, the banking system that is required to hold government bonds sees its balance sheet weaken. A stressed banking system then puts further pressure on an already weak sovereign. The ensuing crisis prompts an outflow of capital and deposits from weaker countries to core eurozone economies.

These synthetic securities would delink the domestic banking system from the national government by allowing private institutions to hold a basket of eurozone sovereign debt, instead of just their own sovereign’s. Further, the repackaging would enhance the supply of safe assets on the continent. At a more symbolic level, a bond that represents all the governments in the union also serves as a shot in the arm for the European project.

It is important to note that the proposal rules out any form of debt mutualization or intergovernmental transfers. For example, if the Greek government is not able to fulfil its obligations, other European governments would not be making the bond holders good. The EC sees this as necessary to avoid the problem of moral hazard: any proposal that includes intergovernmental transfers would be a non-starter in Berlin.

Finally, the proposal can limit the fall-out on peripheral debt yields if and when the European Central Bank (ECB) decides to unwind its government asset purchase program. The organization that would be set up to carry out the issuance of these bonds could replace the ECB in buying those bonds without disrupting the demand dynamics of the eurozone government bond market.

There are some negatives to consider. Italy is likely to oppose the plan because the proposed synthetic bond would bundle existing eurozone government debt in a certain proportion, either by the relative size of economies or according to the ECB’s capital key, which weights countries by the size of their GDP and population. Unless the criteria is the relative size of outstanding government debt (which it would never be), the new bonds would hold a much larger share of the outstanding debt of core eurozone governments and leave out a significant chunk of debt from peripheral countries.

By making these synthetic Eurobonds more attractive to hold than national government debt in the peripheral banking system, the proposal would take away a ready source of demand from these residual periphery bonds, reduce their liquidity and drive up yields. Italy has the largest outstanding debt stock in the union and is understandably touchy about it.

The proposal could, however, be successful in ringfencing the banking sector against spillovers from a weak sovereign. But we could end up replacing the “doom loop” with the “austerity loop,” as rising periphery yields would result in market imposed belt tightening in countries such as Italy.

The uncomfortable reality is that any proposal that eschews fiscal transfers is unlikely to amount to anything more than window dressing at best. But it is an interesting start.

For the Public GoodPresident Trump signed a

bill last month that rolled back a rule that made it easy for states, cities and counties to run retirement savings plans for people who cannot get them through the workplace. Several states are ignoring this development and pressing ahead with alternate plans. The effort is commendable and should be encouraged.

As we

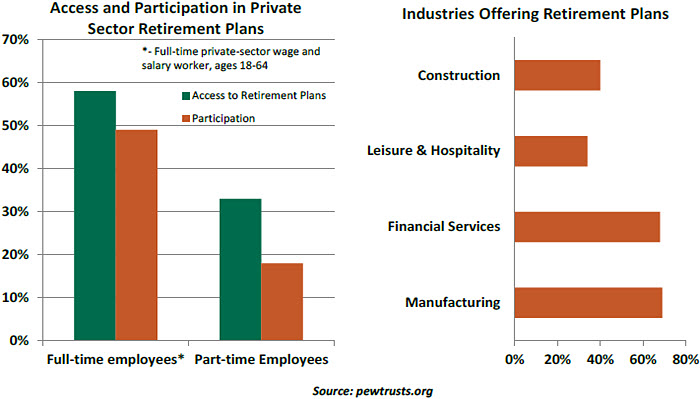

discussed in March, the world has a retirement problem, and America is no exception. To facilitate better access to retirement saving, the U.S. Department of Labor passed a rule last year that enabled states to implement auto-enrollment retirement accounts without being subject to the Employee Retirement Income Security Act (ERISA), which regulates pensions and 401(k) plans. Connecticut, California, Illinois, Maryland, New Jersey, Oregon and Washington moved quickly to introduce plans, and 23 other states and cities are poised to follow. Assets accumulated are turned over to private providers, who manage the investments under the direction of each employee. They are not commingled with state finances.

A majority of small businesses do not offer retirement plans, and nearly two-thirds cite cost as the biggest obstacle. A little over 40% of full-time private sector employees lack access to retirement programs. The situation with part-time workers is even more worrisome.

Research indicates that some industries offer more generous retirement savings programs than others. State-sponsored plans would be of great benefit to sectors like construction and hospitality, where employees are much less likely to have access to a retirement plan.

As the population ages, there will be pressing demands for states to bear costs of social service programs for seniors, such as Medicaid, housing subsidies, and energy assistance. State-sponsored retirement programs will help alleviate this burden by reducing the likelihood of indigence among seniors.

This would seem to be a trend that conservatives would embrace, since it represents a case of less regulation encouraging favorable economic outcomes. But private investment managers have complained that exempting states from ERISA creates an un-level playing field. In our view, however, America’s retirement readiness should take precedence over parochial concerns over market share.

© Northern Trust

www.northerntrust.com

© Northern Trust

Read more commentaries by Northern Trust