SUMMARY

- The United Kingdom Faces a Rising Degree of Difficulty

- The Fed vs. The Markets

- Interpreting Policy Uncertainty and VIX

For the second year running, a British Prime Minister has taken an electoral gamble that has backfired. We are left with more questions than answers: what will British leadership look like in six weeks or six months’ time? Do voters prefer a so-called “Soft Brexit” or a “Hard Brexit”? Will negotiations with the European Union (EU) start on time, and end on time? With the U.K. economy faltering, resolution on these fronts must come quickly.

When the election results came out last Thursday, Prime Minister Theresa May’s position looked untenable. But potential challengers have kept their knives sheathed. After securing the backing of Tory backbenchers (the 1922 Committee) in a highly choreographed meeting, it looks like she may survive for the time being.

This outcome seems to reflect the reality that Brexit has made the Prime Minister’s job a poisoned chalice. Prospective aspirants to 10 Downing Street are letting the incumbent take the blame for Brexit’s inevitable economic damage (or an inability to regain sovereignty from Europe), and living to fight another day. Predicting British politics these days is a fool’s errand, but the prospect of May surviving at least until 2019 (when the United Kingdom leaves the EU) is not as outlandish as it appeared last week.

The new make-up of Westminster Palace is not without silver linings. Tory gains in Scotland have taken the threat of another Scottish independence referendum off the table. Further, a minority Tory government reliant on the support of Irish Democratic Unionist Party is expected to be a more level headed negotiator with the European Union. Securing a frictionless border between Northern Ireland and the Republic of Ireland would now be a matter of political survival for the government. This, along with the reality check delivered by the voters, should end the bravado of a “no-deal” Brexit.

Some observers are now expecting a softer outcome, but that will be an exceptionally challenging outcome to reach. Retaining the benefits of membership in the single market inevitably means that the United Kingdom would continue to allow free movement of people with the EU and that the EU would retain a heavy hand in setting U.K. regulations. This not only makes leaving the EU pointless, but would be politically impossible to sell since the Brexit referendum was won on concerns over immigration and sovereignty.

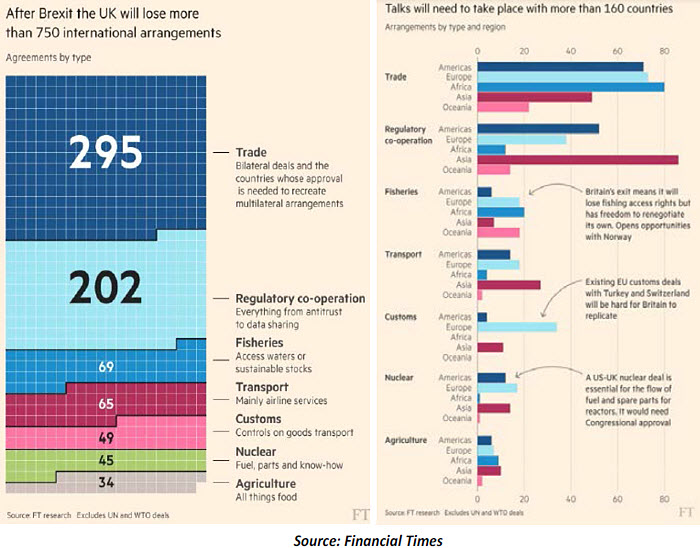

With negotiations soon to get underway, the focus will be on agreeing to the terms of exit from the EU, securing a transition agreement for the United Kingdom and establishing the United Kingdom’s future trading status with the remaining EU members. Time is of the essence here — not only does everything need to be negotiated by March 2019, but it also has to be ratified by 27 parliaments.

The first phase of negotiations will aim to reach a decision on immigrant rights and resolve the United Kingdom’s obligations to the EU budget as it makes its transition (the so-called Brexit bill). While the British government has been defiant on the Brexit bill, and noncommittal on the rights of EU citizens in the United Kingdom, London would gain both time and goodwill for its post-Brexit demands if it displays generosity here.

After sufficient progress has been made on this phase, simultaneous talks would begin on United Kingdom’s future trading relationship with the EU. Agreements on financial regulations, agriculture, fisheries, tariffs, movement of people, the Irish border and jurisdiction of the European Court of Justice, to name some of key items, need to be hammered out. Presenting a tradeoff between jobs and sovereignty at every step for the United Kingdom, these negotiations would put the unity of the government to test. For the EU, choosing between some short-term economic disruption and the integrity of the European project would be an easier job.

This would be a highly complex and time consuming process and a transition deal that keeps the United Kingdom in the single market for a period beyond 2019 is critical. It would avoid a legal cliff, give time to agree on a future trade agreement and make the point of contributions to the EU budget moot by keeping the United Kingdom a de facto member of the EU beyond 2019.

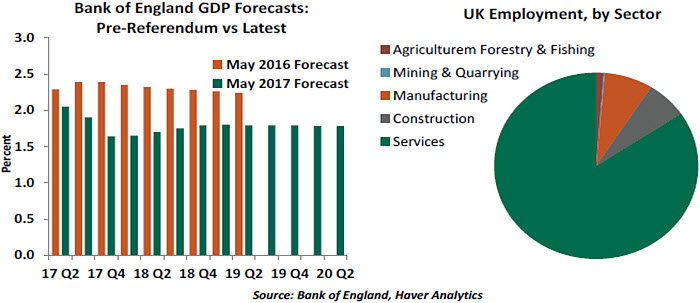

It is worth reiterating the need to get this right. As data continues to show, the U.K. economy is slowing and is expected to underperform the developed market universe. A weaker pound has been a bane for consumer spending, while providing no real benefit for exporters. Uncertainty remains high and is likely to deter investment. The services sector, the bread and butter of the U.K. economy, is focused on the terms of Brexit because a comprehensive trade agreement with the EU that covers business regulations is integral to its viability.

Over the last few months, the U.K. government has brushed aside many of these concerns, while expressing a preference for old-fashioned activist industrial policy. If history is any guide, it is doubtful that the government can achieve much. The importance of services and the requisite regulatory agreement cannot be overstated.

Before Britain fatefully decided to rejoin the gold standard at an overvalued rate in 1925, the then-Chancellor, Winston Churchill, quipped that he “would rather see finance less proud and industry more content.” The overvalued pound not only damaged British manufacturing, but it had a role in precipitating the Great Depression.

May has tried to capture the post-global financial crisis zeitgeist by appealing to the U.K.’s (now former) industrial heartland, while being ambivalent about financial sector’s interests. As in 1925, a disconnect between promise, actions and consequences could be very damaging to Britain.

She Said, They SaidAs expected, the Federal Reserve raised its benchmark interest rates again this week. Also as expected, its actions generated a certain level of controversy.

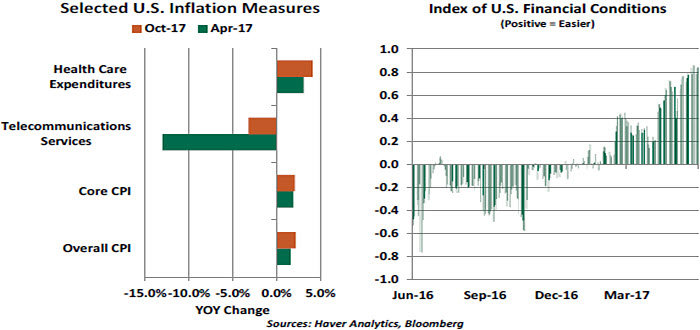

In the days surrounding the Federal Open Market Committee (FOMC) meeting, the financial press raised questions about the Fed’s assessment of U.S. inflation. The price level has advanced more modestly than the Fed’s forecasts anticipated, despite unemployment levels that are much lower than almost anyone predicted. As a consequence, interest rates have risen more slowly than the Fed’s “dot plots” have implied.

The projections released at the conclusion of this month’s FOMC meeting persist in anticipating that inflation will approach the Fed’s 2% target in the medium term. Reflecting this outlook, the median expectation among FOMC participants is for one further interest rate increase this year and three increases each in 2018 and 2019. This is very similar to our projections.

The financial markets, however, appear to have a different point of view. A forecast of Fed strategy can be inferred from fixed income prices and options on financial instruments. At present, those indications assign just a 30% probability to another rate hike this year. And long-term yields in the United States have been falling, even though the Fed has been signaling intentions to continue raising rates.

This led some observers to renew the contention that the Fed and the markets are in conflict with one another. Larry Summers, the former Treasury Secretary and onetime aspirant to the Chair of the Federal Reserve Board, penned an

editorial this week questioning the Fed’s credibility.

In the Fed’s defense, recent inflation readings have been significantly affected by sudden downward movements in a handful of categories, health care expenses among them. These are not expected to continue, and so inflation is likely running closer to the targeted level than it would appear on the surface. What we are seeing in the data may be more a matter of measurement challenges for idiosyncratic situations, rather than a systemic weakening of pricing power.

American monetary policy remains substantially accommodative, especially when you combine the level of interest rates and the size of the Fed’s balance sheet. (At the conclusion of this week’s meeting, the FOMC announced an outline for allowing the balance sheet to decline slowly; its post-meeting statement indicated that the process would start yet this year.) While the prices of goods and services have escalated modestly, asset prices have risen much more aggressively.

Leaving rates too low for too long could raise systemic risks. With financial conditions easing significantly over the past six months, the Fed may be seeking to tame investor exuberance more than inflation.

Finally, market indications of Fed policy and inflation expectations must be taken cautiously. Treasury securities are an international asset class, and the past two decades have seen a massive influx of foreign buyers to the market for U.S. government debt. Recent

reports indicate that China (among others) has been more active in purchasing U.S. government securities, despite the Fed’s outlook.

These investors are certainly looking for good returns, but they may also be trying to achieve better currency diversification and hold assets in a market which is the most liquid in the world. All of this is to say that the market prices that are used to make inference about monetary policy may not be providing the purest readings, and the apparent dissonance between markets and the Fed may be something of an exaggeration.

The Fed is certainly not infallible, which is why policy has proceeded cautiously. But markets are certainly not omniscient, either. Each party will need to watch incoming data over the next few months and recalibrate expectations.

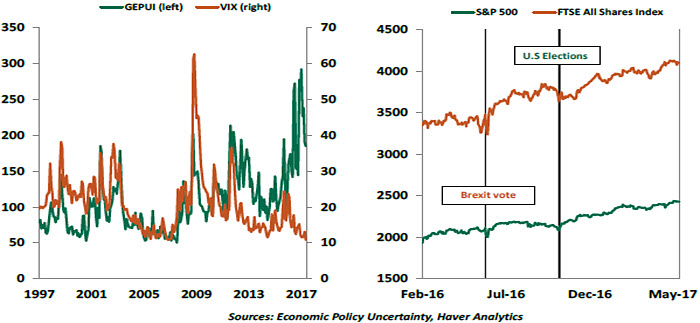

The DecouplingIndexes tracking market volatility and policy uncertainty have diverged, a change from historical patterns. Observers are actively debating which of these two signals best captures the current circumstance.

Two political events led to an increase in economic policy uncertainty in 2016 – the Brexit vote and the U.S. presidential elections. This can be seen in the Global Economic Policy Uncertainty Index (GEPUI), which is a gross domestic product-weighted average of national indexes for 18 countries. The GEPUI reflects the frequency of newspaper articles, in the respective countries, containing terms pertaining to the economy, policy and uncertainty. The GEPUI rose sharply last June and last November, and continues to hover at an elevated level.

The GEPUI and the VIX, the ticker for the Chicago Board Options Exchange Volatility Index, have historically tracked very closely, but have gone their separate ways in recent months. The VIX is a measure of market expectations of near-term volatility as suggested by S&P 500 stock index option prices; it is viewed as a gauge of investor sentiment.

The VIX has been remarkably sedate, even as U.S. equities have reached a series of new highs. Both developments are somewhat at odds with the more alarming signal from the GEPUI. The European Central Bank produced some

research about the reasons for the divergence, suggesting that policy reactions have played a role in holding down the VIX even as uncertainty indices continue to rise. But it is not clear why policy actions began to have an asymmetric impact on the two last year, after affecting them similarly in years prior.

Some of the disparity may stem from the tone of modern media, which has become more extreme (and parochial) in its coverage of economic events and policy. Headlines have become bolder, and adjectives and adverbs have a heightened edge. The GEPUI’s construction makes it vulnerable to the hyperbole that has emerged since Brexit and the U.S. elections, so it may not be the source of alarm that it once was.

Further, investors have proven quite resilient in looking past threats that have proven temporary. The day-to-day drama in Washington and London makes for interesting press, but may not have the long-term impact that some might think.

Nonetheless, the size of the current divergence between volatility and uncertainty measures raises the question of whether markets are overly sanguine. Rushing to embrace a worst-case scenario is probably not warranted, but assuming that all is well may not be well-advised, either.

© Northern Trust

www.northerntrust.com

© Northern Trust

Read more commentaries by Northern Trust