SUMMARY

The first half of the year has flown by. Much has changed: threats to the European Union’s survival have faded, the U.S. Federal Reserve has become less accommodative and China has tightened up on credit. Other things have not changed: American policy-making remains deeply divided, equity markets are still rallying and Europe still needs a lot of structural reform.

The remainder of 2017 promises to be eventful. The following are key themes we will be watching in the months ahead.

Politics and Policy

Many economists upped their U.S. forecasts after last fall’s election, expecting a flurry of health care reform, tax relief, deregulation, and infrastructure spending. We were not among them; even prior to the election, the political dynamic was hostile to advancing legislation of any kind. It went beyond friction between Democrats and Republicans; factions within the Republican Party have been battling as well.

We still do not think that there will be major changes to U.S. tax and fiscal policy this year, or even next. Nonetheless, optimism among consumers, investors and businesspeople remains high. Some markets (currencies, interest rates) have retraced their steps over the past six months, but equity markets have climbed resolutely upward. Corporate earnings have been strong, even in the absence of favorable legislation.

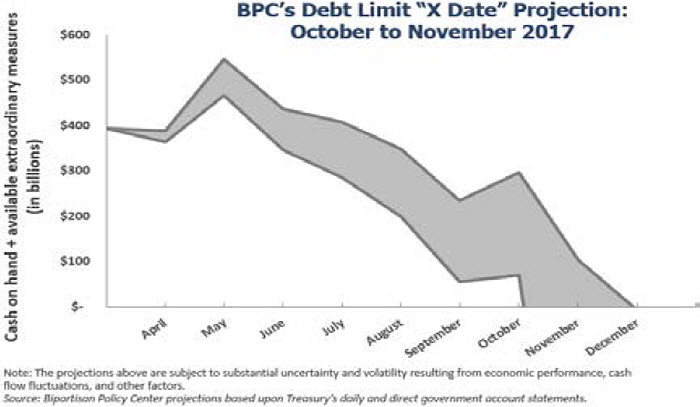

The upbeat outlook may be challenged this fall, when the Treasury runs out of borrowing room under the debt ceiling (right). At that point, the fractiousness in Washington could result in an interruption of government (and potentially a ratings downgrade). For now, spirits are high. But the question of how dependent asset prices are on the achievement of the Trump agenda remains unanswered.

The Votes Are In

Last winter, the European continent was filled with dread over the future of the European Union (EU). Euro-skeptics Marine Le Pen and Geert Wilders were polling as favorites for the French and Dutch general elections, respectively. The moderate Italian Prime Minister Matteo Renzi had just lost a referendum and the populist Five Star Movement appeared to be in the ascendency. The common market seemed to be facing an existential crisis.

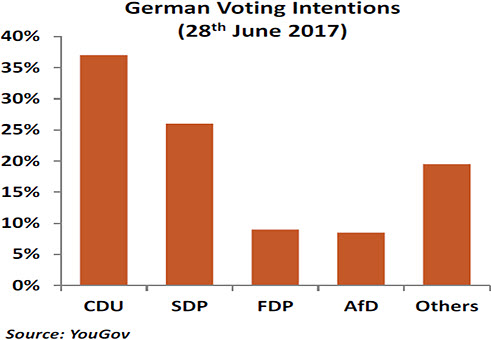

How things have changed. Geert Wilders is barely a footnote in Dutch politics at the moment, and the French turned resoundingly away from the National Front. German elections this autumn have now turned into a virtual non-event, as Angela Merkel is expected to ride home comfortably. This will allow her more room to work with France’s Emmanuel Macron towards forging a closer EU.

Even if we have an upset in Germany, it is unlikely to disturb the apple cart since Merkel’s rival Martin Schulz, of the Social Democratic Party, is perhaps the strongest supporter of EU integration in frontline European politics. He could also help correct some structural imbalances in the Germany economy, such as low wages and tight fiscal policy.

On the other side of the Alps, Italy could be witnessing the return of more familiar political forces as the center-right parties have gained ground in recent local elections. National balloting is likely to be held in the spring of 2018 under a new electoral regime.

While Europe’s populists have failed to advance at the ballot box thus far, it would be a miscalculation to dismiss them entirely. Until governments address the concerns of the aggrieved, the potential for renewed euro-skepticism remains.

The South Will Rise Again

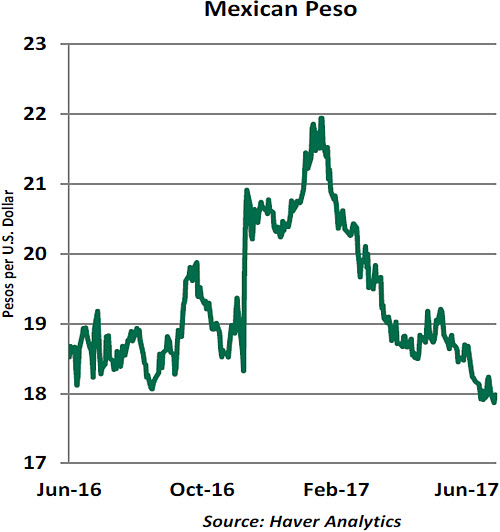

The Mexican economy has encountered a difficult series of challenges in recent months. The peso has endured wide movements, inflation is at a multi-year high, interest rates are elevated and the country is dealing with a challenging phase in its relationship with its northern neighbor.

The peso lost more than 20% of its value between November 2016 and January 2017 in the wake of the U.S. presidential election. Threats by the U.S. to upend the North American Free Trade Agreement (NAFTA) and introduce steep border taxes did not help the outlook for Mexico; neither did the frosty relationship between the presidents of the two countries. But as the most extreme U.S. proposals have become less likely, the Mexican currency has regained lost ground.

Improving Mexican fundamentals have also helped. The current account balance has been improving, portfolio flows are not problematic, and the non-oil trade balance shows a trade surplus for the first time since 1995.

The recent increase in the Mexican policy rate is possibly the end of a hiking cycle designed to contain inflation. The currency is anchored, inflation is predicted to retreat, and real economic growth has surpassed expectations.

There are, however, risks to consider. NAFTA will be reopened, and it is unclear how extensive alterations might be. Any hints that the Fed may shrink its balance sheet or raise rates faster than market expectations will work against the peso. Nonetheless, the economic tone surrounding Mexico is considerably better than it was six months ago.

Bailout or Bail-In?

Europe witnessed two cases of bank failure this month. The first was the collapse of Spanish banking group Banco Popular. It was taken over by rival Santander after it endured a run on its deposits. The Spanish taxpayer was not on the hook, as Popular’s shareholders and junior bond holders absorbed the losses. Essentially, the banking resolution system worked as European authorities envisaged it should.

While Banco Popular’s transition was seen as a successful test case for the new banking regime in Europe, the dissolution of two Venetian banks just weeks later came as a rude shock. Failing lenders Veneto Banca and Banca Popolare di Vicenza secured EUR 5.2 billion in public funds and an additional EUR 12 billion in government guarantees, even as its good assets were taken over by the Italian lender Intesa Sanpaolo. In contrast to what occurred for Santander in Spain, senior bond holders will be made whole by the Italian tax payer.

Italian policy makers have exploited a loophole in the new rules, justifying public support by citing the number of retail bond holders at risk and the systematic importance of the banks. EU leadership has been reluctant to disagree with this posture, given the political uncertainty present in Italy; imposing losses on the masses might have provided momentum to the anti-EU factions there.

But there may be more bank resolutions to come in Italy, and they could be quite expensive. Public support would further burden the Italian government, already one of the most indebted in Europe. And allowing national authorities to circumvent European standards undermines efforts to reinforce a fragmented financial system across the continent.

It is certainly unrealistic to expect the public sector to be a bystander if private buyers are not forthcoming. But recent actions do little to diminish moral hazard for poorly-run banks. Nine years after the onset of the financial crisis, Europe still has not found a consistent way to clean its dirty financial laundry.

Oil’s Not Well If you are taking a drive during your summer vacation, you are in luck. Gasoline prices remain very modest, so you can go as far as you would like. (Or as long as your children will remain peacefully occupied in the back seats.)

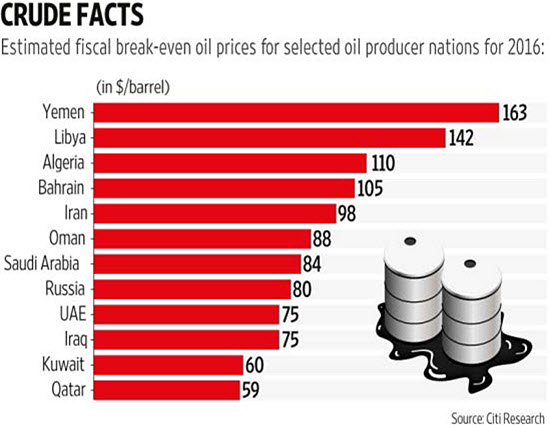

But major oil producers have had very bad luck, indeed. Despite a concerted effort to constrain supply, the Organization for Petroleum Exporting Countries (OPEC) has failed to engineer a sustained rise in crude prices. Increased American production has offset curtailed flow from the Middle East almost barrel-for-barrel.

Oil prices cracked in 2014, eventually falling by more than 60% from their peaks. This disrupted fracking operations in the center of America, where the number of active rigs dropped precipitously. But the remaining producers drove their extraction costs downward, allowing them to bring oil out of the ground profitably at prices of $25 per barrel or less. When the market moved to $50 per barrel in the middle of last year, the spigots opened.

The renewed production has not only capped the price of oil, it has capped the fiscal ambitions of OPEC members. Several of them rely heavily on petroleum revenue to provide benefits to their citizenry; these benefits are now coming under pressure. The Middle East has become much less stable in the last several years, and low oil prices will not help matters.

It was therefore not a great surprise when Saudi Arabia updated its succession plan recently, favoring the author of the ambitious

Saudi 2030 plan. The outline seeks to reduce the country’s reliance on oil by selling the state oil monopoly and reinvesting the proceeds in other avenues of economic development. It is a risky strategy, but there may be no other choice.

Countries that are overly reliant on commodities are always vulnerable to swings in market prices. But given the inelasticity of demand and the concentration of supply, oil seemed an exception to the rule for several decades. But both are now changing importantly, with significant consequences for OPEC and geopolitical stability.

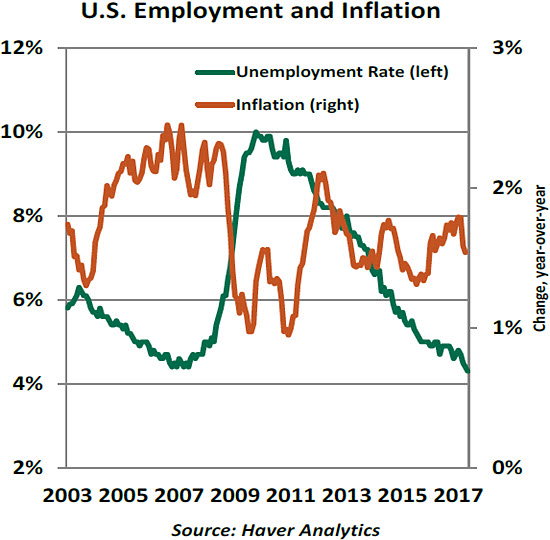

Monetary March The Phillips Curve is a basic tenet of economics that posits a trade-off between inflation and unemployment. Simply stated, inflation should accelerate as the unemployment rate declines. This relationship has traditionally been a pillar for the conduct of monetary policy, but recent U.S. data raises questions about the validity of the Phillips Curve today.

The U.S. unemployment rate, at 4.3%, is well below what most economists consider full employment. And yet inflation remains stubbornly below the Fed’s 2.0% target rate. Inflation readings for the last two months show a reversal even as the jobless rate has fallen; furthermore, wage growth is significantly below levels consistent with full employment.

The big question for monetary policy is whether to act now in anticipation that inflation will move toward the target rate. Fed officials present two views. Presidents Evans, Bullard, and Kashkari would prefer to see inflation move up before taking further action on interest rates, while others (including Fed Chair Janet Yellen) are more confident further growth will translate into higher prices.

This issue will be front and center for monetary policy discussions in second half of the year. In addition, speculation surrounding the future of Yellen, whose term ends in February 2018, will pick up in the months ahead. The Fed will need to manage communications deftly on both fronts to prevent market turbulence.

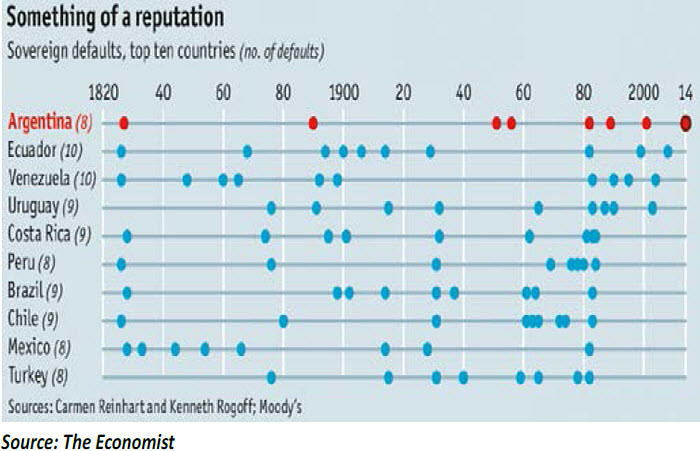

Argentina Hits a Century Argentine President Mauricio Macri has presided over a spectacular about-face in global perceptions of the Argentinian economy. The renewed optimism is not unwarranted, as the government has lifted capital controls, floated the currency and taken steps to tame inflation. Public finances remain an overarching concern, however, and the government is trying to wean the treasury from relying on money printing by the central bank. As part of this effort, Argentina has been issuing sovereign debt in the international markets, the latest offering of which has attracted a lot of attention.

The investor enthusiasm in Argentina’s recent 100-year bond issue has been held up by many as a sure sign of over-optimism, particularly given Argentina’s abysmal track record in honoring its financial commitments. Given the long maturity, the discounted present value of the principal is negligible and markets are pricing a sure default within 50 years. But the high coupon on the century bond still makes it an attractive proposition, since bond holders would get all their initial investment back in just 12 years from coupon payments alone. Essentially, investors are concerned about the return on the money, rather than the return of the money.

There are still significant risks, though. The secondary market for these bonds is fairly thin and any panic selling could involve a substantial discount. Furthermore, this investment is also a bet on Mr. Macri’s political future, which is far from certain. A blow in the October mid-term elections, and/or a shift in global risk appetite, could turn out to be costly.

© Northern Trust

www.northerntrust.com

© Northern Trust

Read more commentaries by Northern Trust

The peso lost more than 20% of its value between November 2016 and January 2017 in the wake of the U.S. presidential election. Threats by the U.S. to upend the North American Free Trade Agreement (NAFTA) and introduce steep border taxes did not help the outlook for Mexico; neither did the frosty relationship between the presidents of the two countries. But as the most extreme U.S. proposals have become less likely, the Mexican currency has regained lost ground.

The peso lost more than 20% of its value between November 2016 and January 2017 in the wake of the U.S. presidential election. Threats by the U.S. to upend the North American Free Trade Agreement (NAFTA) and introduce steep border taxes did not help the outlook for Mexico; neither did the frosty relationship between the presidents of the two countries. But as the most extreme U.S. proposals have become less likely, the Mexican currency has regained lost ground.

The investor enthusiasm in Argentina’s recent 100-year bond issue has been held up by many as a sure sign of over-optimism, particularly given Argentina’s abysmal track record in honoring its financial commitments. Given the long maturity, the discounted present value of the principal is negligible and markets are pricing a sure default within 50 years. But the high coupon on the century bond still makes it an attractive proposition, since bond holders would get all their initial investment back in just 12 years from coupon payments alone. Essentially, investors are concerned about the return on the money, rather than the return of the money.

The investor enthusiasm in Argentina’s recent 100-year bond issue has been held up by many as a sure sign of over-optimism, particularly given Argentina’s abysmal track record in honoring its financial commitments. Given the long maturity, the discounted present value of the principal is negligible and markets are pricing a sure default within 50 years. But the high coupon on the century bond still makes it an attractive proposition, since bond holders would get all their initial investment back in just 12 years from coupon payments alone. Essentially, investors are concerned about the return on the money, rather than the return of the money.