Macro Factors and their Impact on Monetary Policy, the Economy, and Financial Markets

Central Banks’ Era Tranquility Is Over

On June 1, I posted a commentary on Linked-In entitled, “Is a Secular Bear Market in Bonds Possible?” Here’s the last paragraph from that commentary. “In March of 2017, I thought the yield on the 10-year Treasury bond could fall from 2.60% to under 2.20%, as the economy displayed signs of slowing and a record short position held by institutional investors expecting higher interest rates in the Treasury bond futures were forced to cover. The 10-year Treasury yield fell to 2.177% before rising to 2.42%. The pattern in the 10-year Treasury yield bond suggests the yield could fall below 2.177% and approach 2.0%. However, the coming low in the yield could represent a higher low relative to the July 2016 low of 1.32%, and set the stage for the next move up in yields before the end of 2017. This suggests a review of the allocation to bonds and the investment strategy employed in managing bond market risk by investors and financial advisors is appropriate.” That advice proved prescient.

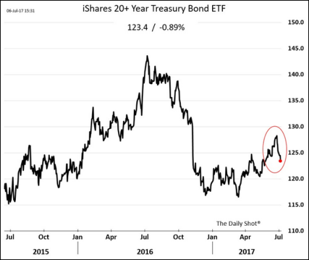

The yield on the 10-year Treasury bond fell to 2.103% on June 14 and posted its lowest close at 2.137% on June 26. In my June 26 Weekly Technical Review (WTR), I discussed why I thought it was time to sell at least half of the Treasury Bond ETF (TLT) after expecting a rally in TLT from $116.80 in mid March to $129.00. “This morning (June 26) TLT traded as high as $128.57, so it is near the 50% retracement level (at $129.00) of the decline from last July’s high and the low in March. The yield on the 10-year Treasury could fall to 2.0% as I have discussed (June 5 WTR), but it is certainly time to sell at least half of the TLT position”

When my advice to sell TLT was written on the afternoon of June 26, I had no idea that Mario Draghi would make comments the following morning that would rattle the global bond market. On June 27, TLT opened at $127.43 and by Friday July 7 had fallen to $122.72, a drop of 3.7%. The reaction to Draghi’s comments on the global bond market was not a surprise as I had discussed this potential in the June 10 issue of Macro Tides. “One of the factors that are likely to trigger higher Treasury bond yields in the U.S. is an increase in European bond yields. Specifically, if the yield on the 10-year German Bund closes above .50%, the Bund yield could quickly rise to .9% to 1.0%. An increase of this magnitude would certainly cause Treasury yields to rise. A decision by the ECB to reduce the amount of its monthly bond purchases could be a trigger for yields to rise throughout Europe.” The German Bund closed above .50% on July 6.

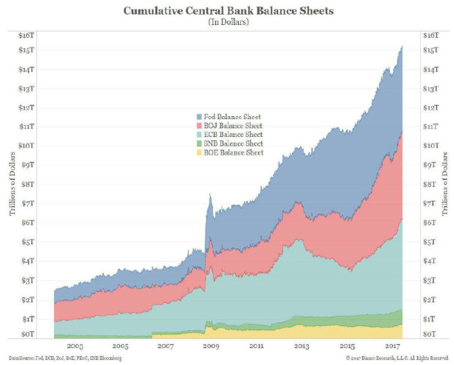

It is said that a bell doesn’t ring at a market top or bottom. But in the era of central bank monetary experimentation, the global bond market heard a bell on June 27, which sounded the end of the Era of Tranquility. Since the financial crisis the major central banks have confronted every economic hiccup with a sea of liquidity that has progressively calmed financial markets and created the Era of Tranquility. In 2009 the Federal Reserve’s response was warranted since the principal goal of a central bank is to provide liquidity during a liquidity crisis, when market participants are unable or are too focused on capital preservation to assume more risk. Prior to the financial crisis the balance sheet of the Federal Reserve totaled $900 billion and collectively the five major central banks held $3.5 trillion in assets. By mid 2009 the collective balance sheets of the central banks had ballooned to more than $7 trillion. After the global financial system was stabilized and the recession in the U.S. ended in June 2009, the major central banks allowed their balance sheets to shrink modestly. However, by 2011 the collective balance sheet was back to $7 trillion. In the six years since, the collective balance sheet has more than doubled, even though the financial crisis was years in the rear view mirror and economic growth had resumed.

Central bankers rationalized that because economic growth wasn’t as robust as they wanted, unemployment rates were deemed too high, and inflation was well below their 2.0% target, expanding their balance sheets was necessary. Central banker’s fixation on getting inflation up to 2.0% is interesting since it is universally accepted. This suggests it was taught to them as they were getting their PhD’s in economics, so no one ever questions whether having an inflation target of 2.0% makes sense. In 36 years, prices double if inflation is 2.0%, and quadruple in 72 years. The average person in the U.S. lives about 80 years. In the average lifetime, the cost of living will quadruple and a central banker armed with a PhD in economics considers this price stability and a monetary success story!

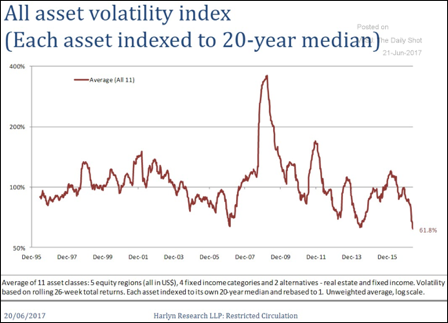

Central bankers can congratulate themselves on lowering volatility throughout the world in just about everything that trades. Based on rolling 26 week returns for 11 different assets classes that encompass 5 equity regions, four income categories, and two alternative asset classes, the level of volatility is the lowest in the past 22 years. On the surface this appears to be a good thing since lower volatility increases confidence which is supportive of economic growth. The risk from a prolonged period of low volatility is usually hidden, even though it is often hiding in plain sight. When volatility remains low for years, investors and businesses feel comfortable taking more risk since the assumption of more risk has been rewarded due to the stable environment. In 2005 and 2006, housing prices rose and rewarded those who bought a bigger home or invested in a second or third home. As it was unfolding, most people knew it was too good to be true, but no one anticipated what would cause it to end or the repercussions after the curtain came down. Importantly, the Federal Reserve proved no more observant of the obvious than the average schmuck who bought over priced property in Las Vegas, Phoenix, or Miami, even though it was the Fed’s responsibility to administer oversight of the large banks and lending practices.

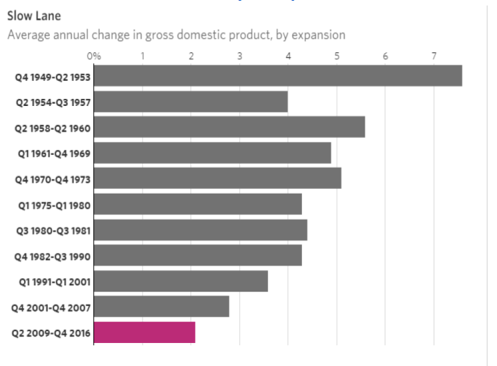

Between 2007 and the end of 2014, the Fed’s balance sheet grew from $900 billion to $4.5 trillion a fivefold increase. For all of its huffing and puffing, the recovery since June 2009 has been the weakest since World War II. What’s interesting is that the second weakest recovery occurred from 2001 to 2007. Although the Federal Reserve didn’t employ quantitative easing during that recovery, they did maintain negative real interest rates longer than ever before. This experiment resulted in less money going into the real economy and more flowing into assets – homes and stocks. The Fed’s theory was that higher asset prices would spur consumption and eventually translate into stronger economic growth. In 2005, home owners pulled more money out of the rising value of their home than the total increase in personal income. Think about that. Wage and job growth generated a smaller increase in personal income than home owners tapping their house value as an ATM. The sustainability of economic growth had become more dependent on rising home values, as opposed to business investment, job growth, and increased wages.

After home prices collapsed by more than 25% in many cities, the Fed was forced to use monetary policy as a tool to get home prices back up. This is why the Fed targeted mortgage backed securities as well as Treasury bonds in its Quantitative Easing programs and why the Fed felt it necessary to launch QE2 and QE3. Fed Chairman Bernanke has acknowledged that the Fed also wanted stock prices to rise in expectation that the wealth affect it would create would spill over into the economy in the form of higher consumption. Record high stock prices had a minimal economic impact but they did worsen income and asset inequality and have created more social tension in our society between the top 1% and the bottom 60%.

After home prices collapsed by more than 25% in many cities, the Fed was forced to use monetary policy as a tool to get home prices back up. This is why the Fed targeted mortgage backed securities as well as Treasury bonds in its Quantitative Easing programs and why the Fed felt it necessary to launch QE2 and QE3. Fed Chairman Bernanke has acknowledged that the Fed also wanted stock prices to rise in expectation that the wealth affect it would create would spill over into the economy in the form of higher consumption. Record high stock prices had a minimal economic impact but they did worsen income and asset inequality and have created more social tension in our society between the top 1% and the bottom 60%.

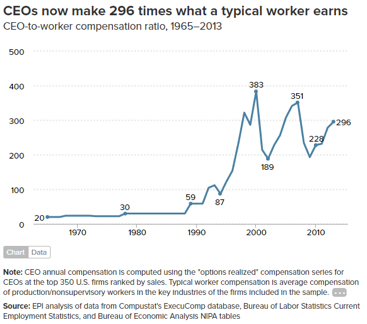

An analysis by the left leaning Economic Policy Institute of executive compensation at the largest 350 companies, compared to the average compensation of production workers at the same 350 companies, shows how much the change in the composition of executive compensation has skewed the ratio of compensation between the average worker and executives. CEO compensation includes salary, stock, stock options, as well as some pension perks. In the mid 1980’s, the average CEO made 30 times the production worker in their company. The great bull market in the 1990’s dramatically increased the value of stock options, especially at technology firms. The ratio of CEO compensation to the average worker soared to 383 to 1, a fourteen fold increase in less than 15 years. The 2001-2003 bear market gutted the value of stock options, especially at technology firms, causing the ratio of CEO to worker compensation to be cut in half. The ratio rebounded during the 2003-2007 bull market, only to fall again during the financial crisis. The S&P 500 has increased almost 30% from the end of 2013 when it closed at 1848, so the ratio is probably approaching the levels it reached in 2000.

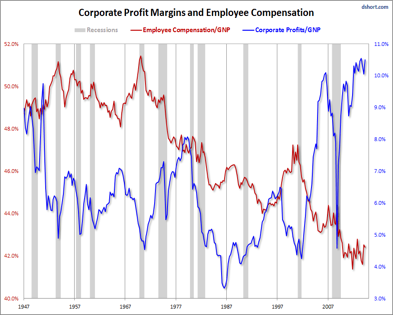

In all fairness to the Fed, the increase in executive compensation since the early 1980’s has been driven more by a pholosophical change within boardrooms than by monetary policy. The Fed earned at least an honorable mention though, after the initiation of QE2 and QE3 despite the fact the recovery was entrenched. Over the last 35 years maximizing shareholder value has been the dominant goal of executives of public companies and corporate director boards. The seed for this philosophy was planted in a New York Times Op-ed piece by Milton Friedman in 1971 making the case that corporate executives needed to have their incentives aligned with shareholders. According to Friedman, the best way to accomplish this was to primarily link executive’s compensation to the performance of the company’s stock. The secular bear market that lasted from 1966 to 1982 fomented shareholders’ frustration with poor stock returns and was a fertile environment for the seed Friedman planted to blossom. The Mission Statement of the Business Round Table in 1981 stated “Corporations have a responsibility, first of all, to make available to the public quality goods and services at fair prices, thereby earning a profit that attracts investment to continue and enhance the enterprise, provide jobs, and build the economy. The long term viability of the corporation depends upon its responsibility to the society of which it is a part. And the well being of society depends upon profitable and responsible business enterprises.” In 1997 the mission statement of the Business Roundtable stated that the principle objective of a business enterprise “is to generate economic returns to its owners” and if “the CEO and the directors are not focused on shareholder value, it may be less likely the corporation will realize that value.” The shift in emphasis from an enterprise to provide jobs that contribute to the well being of society in 1981 to a far narrower focus to generate economic returns to its owners in 1997 is clearly evident in how wages and profits as a percent of GDP has evolved since 1947. Corporate profit margins as a percent of GDP are near the highest level of the past 70 years, while worker compensation is near the lowest level since 1947. (Chart compliments of Doug Short Advisor Perspectives with data through 2014) I will be very surprised if the pendulum doesn’t begin to shift away from maximizing shareholder value toward better wages in the next five to ten years for one reason. The middle class needs a pay increase and the Federal government can’t afford a tax cut, but corporate America can allow profit margins to shrink modestly to pay higher wages.

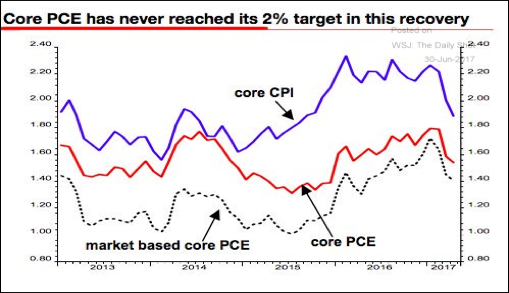

The Fed’s experiment with negative real interest rates during the 2001 – 2007 recovery and since 2009 suggests that it did not spur economic activity as measured by GDP growth but it did result in a misallocation of capital. Corporations have spent more than $4 triilion on stock buybacks since 2010, rather than investing in their future because the Fed had effectively debased the value of money with negative real interest rates. Ironically, this debasement did not result in hyperinflation or even a sustained rise in inflation, especially in the core PCE which is the Fed’s preferred inflation gauge. In May the core PCE was 1.5%. The federal funds rate is at 1.14% which is below inflation, so the Fed’s policy rate is still negative even after 4 rate increases since December 2015.

The Fed’s experiment with negative real interest rates during the 2001 – 2007 recovery and since 2009 suggests that it did not spur economic activity as measured by GDP growth but it did result in a misallocation of capital. Corporations have spent more than $4 triilion on stock buybacks since 2010, rather than investing in their future because the Fed had effectively debased the value of money with negative real interest rates. Ironically, this debasement did not result in hyperinflation or even a sustained rise in inflation, especially in the core PCE which is the Fed’s preferred inflation gauge. In May the core PCE was 1.5%. The federal funds rate is at 1.14% which is below inflation, so the Fed’s policy rate is still negative even after 4 rate increases since December 2015.

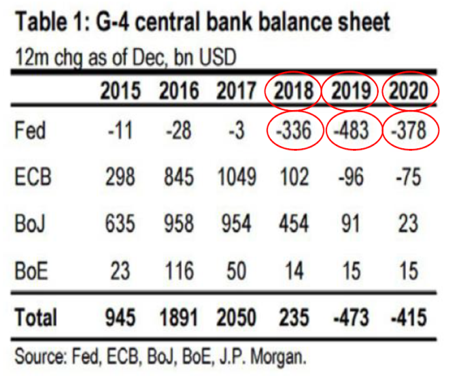

Like all good things the era of central bank monetary experimentation is coming to an end as is the tranquility associated with it. The Federal Reserve terminated QE3 at the end of 2014, and increased the federal funds rate once in 2015 and 2016 and twice in 2017. After the June FOMC meeting, the Fed provided an outline of how they might gradually shrink their balance sheet. Initially the Fed won’t roll over maturing Treasury bonds at $6 billion per month, and will increase it by another $6 billion every three months. Within a year, the Fed would be paring its balance sheet by $30 billion a month. For mortgage-backed securities (MBS), the Fed will proceed in the same manner but at a $4 billion clip. In twelve months, the Fed would be lowering its balance of MBS by $20 billion a month. If the Fed begins to shrink its balance sheet in January 2018, it will reduce it by $336 billion in 2018. The collective balance of the four major central banks will however continue to expand in 2018 as the Bank of Japan and ECB add to their balance sheets.

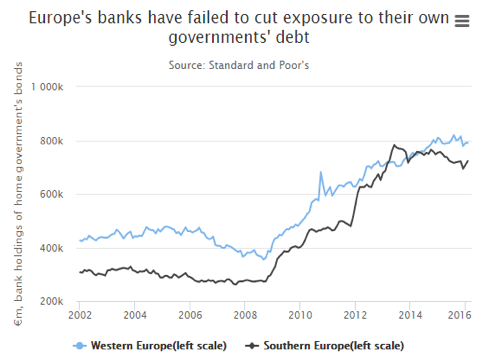

The European Central Bank was late to the QE party but became an active participant in 2016. The ECB also took the concept of negative real interest rates to an extreme as it pushed its policy rate to -.40% in March 2016. This action caused interest rates on sovereign bonds throughout Europe to fall below 0%. At the end of 2016, $9.1 trillion of bonds sported yields below 0%. According to Fitch Ratings the amount of 7-year bonds with a negative yield declined from $2.6 trillion on June 27, 2016 to $500 million on March 1, 2017. The ECB’s gambit of driving rates below 0% has to be the biggest example of the greater fool theory in history, even larger than the Tulip Bulb craze in 1637. A buyer of a bond with a negative yield pays more than $1,000 for a bond that will return $1,000 upon maturity and is thus guaranteed to lose money. There will be significant losses on European sovereign bonds as interest rates rise, and the ECB could be the biggest loser of all since it owns more bonds than institution. European banks are also large holders of sovereign debt. Current regulations push banks to hold their own governments’ bonds. Sovereign debt is deemed by regulators to be risk-free, meaning banks do not have to hold capital against the risk of a default. Banks also have to hold large volumes of liquid assets – those which can be sold immediately if need be – which include government bonds. The potential problem is a bank having to sell their sovereign bonds if rates are higher than when the bonds were originally purchased. These sales would create a loss for which the bank holds no reserve to offset the loss.

The European Central Bank was late to the QE party but became an active participant in 2016. The ECB also took the concept of negative real interest rates to an extreme as it pushed its policy rate to -.40% in March 2016. This action caused interest rates on sovereign bonds throughout Europe to fall below 0%. At the end of 2016, $9.1 trillion of bonds sported yields below 0%. According to Fitch Ratings the amount of 7-year bonds with a negative yield declined from $2.6 trillion on June 27, 2016 to $500 million on March 1, 2017. The ECB’s gambit of driving rates below 0% has to be the biggest example of the greater fool theory in history, even larger than the Tulip Bulb craze in 1637. A buyer of a bond with a negative yield pays more than $1,000 for a bond that will return $1,000 upon maturity and is thus guaranteed to lose money. There will be significant losses on European sovereign bonds as interest rates rise, and the ECB could be the biggest loser of all since it owns more bonds than institution. European banks are also large holders of sovereign debt. Current regulations push banks to hold their own governments’ bonds. Sovereign debt is deemed by regulators to be risk-free, meaning banks do not have to hold capital against the risk of a default. Banks also have to hold large volumes of liquid assets – those which can be sold immediately if need be – which include government bonds. The potential problem is a bank having to sell their sovereign bonds if rates are higher than when the bonds were originally purchased. These sales would create a loss for which the bank holds no reserve to offset the loss.

It is said that a bell doesn’t ring at a market top. But in the era of central bank monetary experimentation the global bond market heard a bell on June 27. Mario Draghi made a number of comments that strongly hinted that a change in the ECB’s QE program is coming. “Deflationary forces have been replaced by reflationary ones. All the signs now point to a strengthening and broadening recovery in the euro area. Political winds are becoming tailwinds. There is a newfound confidence in the reform process, and newfound support for European cohesion, which could help unleash pent-up demand and investment.” As usual for any central banker, Draghi emphasized that any changes would be gradual. “Any adjustments to our stance have to be made gradually, and only when the improving dynamics that justify them appear sufficiently secure.” The global bond market wasn’t gradual in its response as bond yields jumped. Since June 26, the yield on the 10-year German Bund has soared from .244% to .571% on July 7, while yields rose more in France, Spain and Italy, and the 10-year Treasury bond yield climbed from 2.137% to 2.396%.

It is said that a bell doesn’t ring at a market top. But in the era of central bank monetary experimentation the global bond market heard a bell on June 27. Mario Draghi made a number of comments that strongly hinted that a change in the ECB’s QE program is coming. “Deflationary forces have been replaced by reflationary ones. All the signs now point to a strengthening and broadening recovery in the euro area. Political winds are becoming tailwinds. There is a newfound confidence in the reform process, and newfound support for European cohesion, which could help unleash pent-up demand and investment.” As usual for any central banker, Draghi emphasized that any changes would be gradual. “Any adjustments to our stance have to be made gradually, and only when the improving dynamics that justify them appear sufficiently secure.” The global bond market wasn’t gradual in its response as bond yields jumped. Since June 26, the yield on the 10-year German Bund has soared from .244% to .571% on July 7, while yields rose more in France, Spain and Italy, and the 10-year Treasury bond yield climbed from 2.137% to 2.396%.

Central bankers established new frontiers in monetary policy in response to the financial crisis and then continued to go where central banks had never gone before. Now they must navigate the unwinding of negative interest rates and bloated balance sheets without impairing economic growth or destabilizing financial markets. They must accomplish these tasks without a play book since no central banker has ever been down this road. Effectively, Janet and Mario must perform a Reverse 3 1/2 Somersaults in the Tuck Position from the 33 foot high dive platform after reading a couple of books about diving. To assume they can pull this off without a hitch is foolhardy since the risk for a Taper Tantrum Sequel is high.

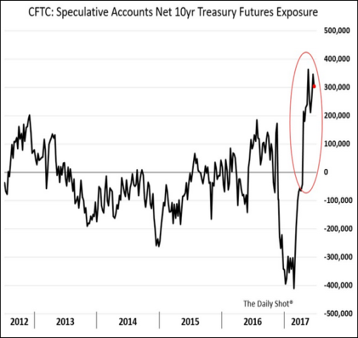

One of the reasons I thought bond yields were likely to fall from their peak in mid March was the record short position speculators had established in anticipation of higher interest rates. As rates fell, speculators were forced to cover their short positions which only propelled yields lower and bond prices higher. Now speculators have the largest long position in years in anticipation of lower interest rates. As rates climb the decline in bond prices could accelerate as these positions are liquidated putting even more downward pressure on bond prices. During Taper Tantrum I, which was ignited by comments from Fed Chairman Bernanke, the yield on the 10-year Treasury bond soared from 1.70% in May 2013 to 3.03% on December 31, 2013, an increase of 1.33%. Speculators in May 2013 were holding a long position that was 1/3 of what they hold now.

One of the reasons I thought bond yields were likely to fall from their peak in mid March was the record short position speculators had established in anticipation of higher interest rates. As rates fell, speculators were forced to cover their short positions which only propelled yields lower and bond prices higher. Now speculators have the largest long position in years in anticipation of lower interest rates. As rates climb the decline in bond prices could accelerate as these positions are liquidated putting even more downward pressure on bond prices. During Taper Tantrum I, which was ignited by comments from Fed Chairman Bernanke, the yield on the 10-year Treasury bond soared from 1.70% in May 2013 to 3.03% on December 31, 2013, an increase of 1.33%. Speculators in May 2013 were holding a long position that was 1/3 of what they hold now.

During the first Taper Tantrum in 2013, the 10-year Treasury yield rose by about 1.30%. From the low of 1.32% in July 2016, the 10-year Treasury yield increased to 2.62% in March 2017, an increase of 1.30%. From the recent low of 2.10%, an equal rise of 1.30% suggests the potential of the 10-year yield climbing to 3.40%. An attack on the high of 3.03% in December 2013 is almost certain in coming months. This indicates that a secular bear market in bonds is not only possible but likely.

Is a Secular Bear Market in Bonds Possible? (Originally posted on Linked-In On June 1, 2017)

During the 35 year secular bull market that began in October 1981, there were a number of sharp increases in yields in which bond prices fell. But investors who held on were bailed out by the secular bull market and eventually recovered all the losses and with gains to show for their patience. In a secular bear market, patience is rewarded with more losses, as yields trend higher after any dip. This painful lesson was learned by bond holders during the 35 year secular bear market of 1946-1981. Just as bond investors could not imagine how the yield on the 10-year Treasury bond would decline from 15.68% in 1981 to 1.32% in July 2016, it is just as difficult to anticipate what events and economic conditions could cause yields to rise materially from current levels. The coming government funding crisis is likely to play a role. The key point is respecting that secular bear markets occur and investors must be prepared to alter their investment strategy in order to deal with a bear market in bonds. The buy and hold approach which has served investors and financial advisors well since 1981 may be the wrong strategy, if the bond market is on the cusp of the next secular bear market.

On April 10, 1912 everyone boarding the Titanic knew they were getting on the largest passenger ship ever built. Before Mr. and Mrs. Albert Caldwell boarded, a Titanic crewman told them “Not even God could sink this ship.” What the Caldwell’s, the crewman, and everyone else aboard the Titanic didn’t know was that at 11:40 p.m. on April 14 the Titanic would hit an iceberg and sink at 2:20 a.m., less than 3 hours after striking the iceberg. Today, most Americans don’t realize that the U.S. economy is sailing toward a financial iceberg of excessive debt and unfunded government promises and programs. The Titanic was commandeered by a capable Captain. The two political parties commandeering the future of the United States have squandered the last two decades ducking their responsibility of educating and warning the American people of the coming government funding crisis so it could minimized. The coming collision between demographics and projected spending in Social Security, Medicare, Medicaid, and every other government program has the potential to cause an upheaval in the social, political, and economic foundations of this country. Although the outcome is not preordained, time is running short. In 2016 the Trustees for the Medicare and Social Security programs estimated that Medicare’s trust fund will exhaust its reserves in 2028, and Social Security will follow in 2034. Medicare covers 55 million Americans, while 49 million are receiving Social Security benefits, and both programs will cover more people as Baby Boomers age. The increasing cost of both programs is driven by the aging of the U.S. population, so increasing economic growth can’t provide a total solution. Medicare and Social Security accounted for 41% of federal spending in 2016, up from 36% in 2011. The demographic headwinds facing the Social Security program underscore the problem. In 2008, there were 3.2 workers for each Social Security beneficiary. In 2016, the ratio of worker to beneficiary fell to 2.8, and is expected to fall to 2.2 during the next 20 years. If Congress does nothing before 2034, a 21% reduction in benefits will be necessary to stabilize the Social Security trust fund.

The longer Congress waits to act, the more draconian the ‘solutions’ will need to be and potentially divisive. The policy actions needed are likely to prove a drag on economic growth and require some amount of sacrifice for a large number of Americans. This is why addressing government entitlement spending is considered the third rail of politics. The sad reality is that both political parties are more interested in holding onto power, than doing what’s best for the country. A combination of benefit cuts, tax increases, means testing of benefits received, and a later retirement age will be needed to sustain Social Security and Medicare. Younger generations will be asked to sacrifice their standard of living so older generations can receive most of the government benefits promised. It is easy to see why the magnitude of the coming changes has the potential to cause an upheaval in the social, political, and economic foundations of this country.

Risks for the Financial Markets

On May 17, 2007, Fed Chairman Ben Bernanke provided this assessment of subprime mortgages. "We believe the effect of the troubles in the subprime sector on the broader housing market will likely be limited, and we do not expect significant spillovers from the subprime market to the rest of the economy or to the financial system. The vast majority of mortgages, including even subprime mortgages, continue to perform well. Past gains in house prices have left most homeowners with significant amounts of home equity, and growth in jobs and incomes should help keep the financial obligations of most households manageable." On June 27, 2017 Fed Chairperson Janet Yellen was asked about the potential of another financial crisis. “Would I say there will never, ever be another financial crisis? You know, probably that would be going too far, but I do think we’re much safer, and I hope that it will not be in our lifetimes, and I don’t believe it will be.”

It is not possible to know whether the coming government funding crisis will merely be an extended period of disequilibrium, a major dislocation, or lead to a financial crisis. What is fairly certain is that financial markets will be buffeted as this country wrestles with the social, political, and economic challenges the government funding crisis represents. This period of turmoil will present equity and bond investors with a high level of uncertainty, stress, volatility, and the risk of large losses.

Bonds

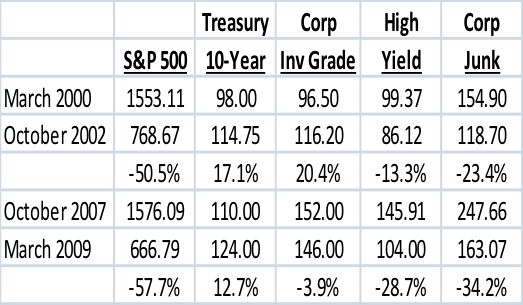

Financial advisors and investors who had a traditional allocation of 60% stocks and 40% bonds during the bear markets of 2000-2002 and 2007-2009 were partially insulated from equity losses that exceeded 50% in each bear market. Treasury bonds provided gains to offset losses, while investment grade corporate bonds performed well, especially in the 2000-2002 bear market. Even High Yield and Junk bonds helped cushion the equity losses, although they did lose money.

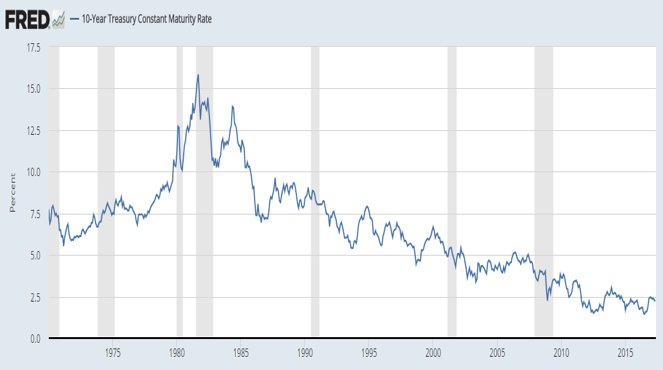

Given this recent history financial advisors and investors are likely to expect Treasury bonds to perform similarly in the next bear market. There are two reasons why financial advisors might not rely on this outcome. Interest rates peaked in 1981 and trended lower in a 35 year secular bull market. During this long bull market, each high in Treasury rates was below the prior high and each low was below a prior low. What makes this 35 year time frame interesting is that the 35 year secular bull market from 1981 was preceded by a 35 year secular bear market that began in April 1946. During that secular bear market, the yield on the 10-year Treasury bond rose from 2.19% to 15.68% in October 1981. It’s possible that the low in the 10-year Treasury yield at 1.32% in July 2016 may have marked the end of the secular bull market and the beginning of a new bear market in Treasury bonds. Even if this proves to be true, the initial increase in Treasury rates is likely to be gradual. Pension funds and global investors are likely to buy Treasury bonds as yields tick higher. Buying is likely to emerge if the yield on the 10-year Treasury bond reaches 3.0%, 3.5%, and 4.0%, as these round levels will appear to offer value relative to the historically low yields in recent years.

Given this recent history financial advisors and investors are likely to expect Treasury bonds to perform similarly in the next bear market. There are two reasons why financial advisors might not rely on this outcome. Interest rates peaked in 1981 and trended lower in a 35 year secular bull market. During this long bull market, each high in Treasury rates was below the prior high and each low was below a prior low. What makes this 35 year time frame interesting is that the 35 year secular bull market from 1981 was preceded by a 35 year secular bear market that began in April 1946. During that secular bear market, the yield on the 10-year Treasury bond rose from 2.19% to 15.68% in October 1981. It’s possible that the low in the 10-year Treasury yield at 1.32% in July 2016 may have marked the end of the secular bull market and the beginning of a new bear market in Treasury bonds. Even if this proves to be true, the initial increase in Treasury rates is likely to be gradual. Pension funds and global investors are likely to buy Treasury bonds as yields tick higher. Buying is likely to emerge if the yield on the 10-year Treasury bond reaches 3.0%, 3.5%, and 4.0%, as these round levels will appear to offer value relative to the historically low yields in recent years.

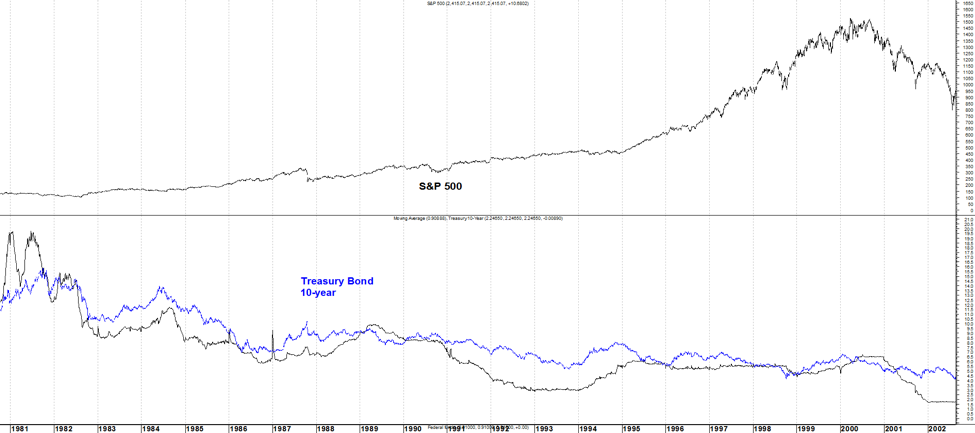

The second reason is that the negative correlation between Treasury bonds and stocks is a relatively new phenomenon. During the 1940’s, 1950’s, 1960’s, 1970’s, 1980’s, and 1990’s, bond and stock prices were fairly correlated. Although stocks typically ignored the initial increase in Treasury yields, they eventually succumbed and a bear market followed. As the charts below illustrate, Treasury yields moved in response to changes in the Federal funds rate. When the Federal funds rate rose above the yield on

The second reason is that the negative correlation between Treasury bonds and stocks is a relatively new phenomenon. During the 1940’s, 1950’s, 1960’s, 1970’s, 1980’s, and 1990’s, bond and stock prices were fairly correlated. Although stocks typically ignored the initial increase in Treasury yields, they eventually succumbed and a bear market followed. As the charts below illustrate, Treasury yields moved in response to changes in the Federal funds rate. When the Federal funds rate rose above the yield on

the 10-year Treasury bond, a yield curve inversion was created, indicating a tight monetary policy. A yield curve inversion led to bear market declines in 1966, 1969-1970, 1973-1974, and 1981-1982. Interest rates declined once the Federal Reserve eased monetary policy, which launched a new equity bull market.

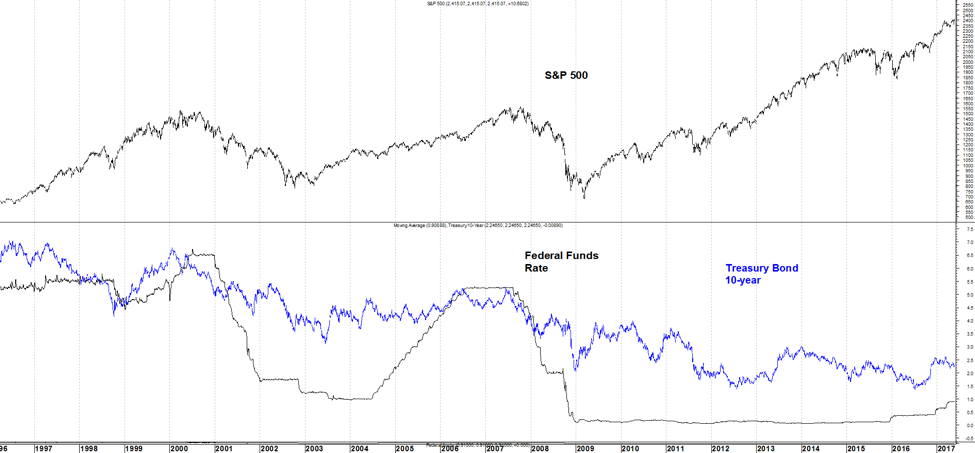

After the secular peak in interest rates in 1981, yield curve inversions have been infrequent. An increase in interest rates preceded bear markets in 1983-1984, the stock market crash in 1987, and a shallow decline in 1994. The 2000-2002 bear market was preceded by a yield curve inversion, after the Federal Reserve increased the Federal funds rate from 4.5% to 6.5%. The financial crisis in 2008 was also preceded by a yield curve inversion, as the Federal Reserve increased the Federal funds rate from a historic low of 1.0% in June 2004 to 5.25% in July 2006. This inversion was unique in that the yield on the 10-year Treasury bond only rose from 4.7% in June 2004 to 5.2% in June 2007, despite the 4.25% increase in the Federal funds rate. Fed Chairman Alan Greenspan referred to this as a ‘conundrum’.

In coming years, the Federal Reserve will be more constrained in how much they will be able to increase the Federal funds rate given the high level of debt. The ratio of total debt to GDP has soared from $1.65 for each dollar of GDP in 1982 to $3.55 of debt for each dollar of GDP in 2016. Rising interest expenses from higher interest rates will prove a burden on over indebted consumers, companies, and the federal government. It will take a smaller increase in rates to slow the economy in coming years than in the past. This suggests the coming secular bear market will not be as devastating as the 1946-1981 bear market. The economy will simply not tolerate the yield on the 10-year Treasury bond rising to 8.0%, let alone the 1981 peak of 15.68%.

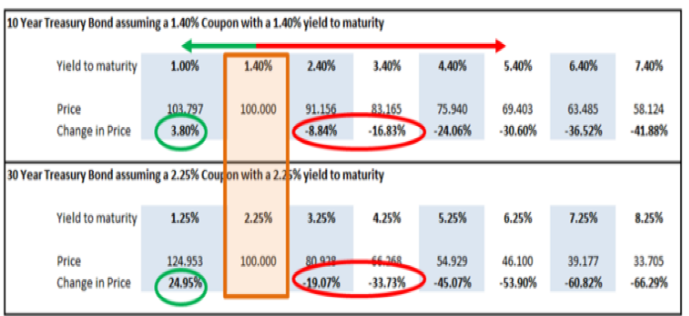

In reviewing the chart of the 10-year Treasury bond, an increase to near the 2007 high of 5.20% seems plausible within the next decade. Although yields are not likely to rise as much as in the prior bear market, losses could still be significant as the nearby table illustrates. When the yield of the 10-year Treasury bond rose from 1.40% in July 2016 to 2.40% in December 2016, the price of the bond declined by -8.84%. Should the yield rise to 3.4%, it will decline by another 7.99%, bringing the total decline to -16.83%. And if the yield climbs to 5.20%, the total loss would increase to over -28.0%. Treasury bonds with maturities longer than 10 years would experience even larger losses. This discussion is meant as a reference with actual results dependent on numerous factors.

The key point is respecting that bear markets occur and investors must be prepared to alter their investment strategy in order to deal with a potential secular bear market in bonds. The buy and hold approach which has served investors and financial advisors well since 1981 may be the wrong strategy, if the bond market is on the cusp of the next secular bear market. This suggests that investors and financial advisors should consider adopting a tactical approach for a portion of their bond assets. A tactical strategy could minimize losses during periods when yields are rising, and potentially add capital gains when bond yields fall.

The key point is respecting that bear markets occur and investors must be prepared to alter their investment strategy in order to deal with a potential secular bear market in bonds. The buy and hold approach which has served investors and financial advisors well since 1981 may be the wrong strategy, if the bond market is on the cusp of the next secular bear market. This suggests that investors and financial advisors should consider adopting a tactical approach for a portion of their bond assets. A tactical strategy could minimize losses during periods when yields are rising, and potentially add capital gains when bond yields fall.

In March of 2017, I thought the yield on the 10-year Treasury bond could fall from 2.60% to under 2.20%, as the economy displayed signs of slowing and a record short position held by institutional investors expecting higher interest rates in the Treasury bond futures were forced to cover. The 10-year Treasury yield fell to 2.177% before rising to 2.42%. The pattern in the 10-year Treasury yield bond suggests the yield could fall below 2.177% and approach 2.0%. However, the coming low in the yield could represent a higher low relative to the July 2016 low of 1.32%, and set the stage for the next move up in yields before the end of 2017. This suggests a review of the allocation to bonds and the investment strategy employed in managing bond market risk by investors and financial advisors is appropriate.

Bond yields have moved higher since this was published on June 1, so investors and financial advisors should have a greater sense of urgency to establish a new game plan on how to manage risk during a bear market in bonds now that Central Banks’ era of tranquility has likely ended.

Stock Market

In the short term, the S&P could be vulnerable to a correction of 5% or so as the market adjusts to rising interest rates. Interest sensitive sectors like utilities, consumer staples, and real estate are already down and likely to decline further. The high flying technology sector has so far corrected 4% from its high on June 9 and could dip another 4% to 6% before establishing a trading low. The financial stocks have already rallied nicely due to lower regulations, the Fed’s rate hikes, and a wider yield curve spread since June 27, but could be vulnerable to some profit taking if earnings come in light as I expect.

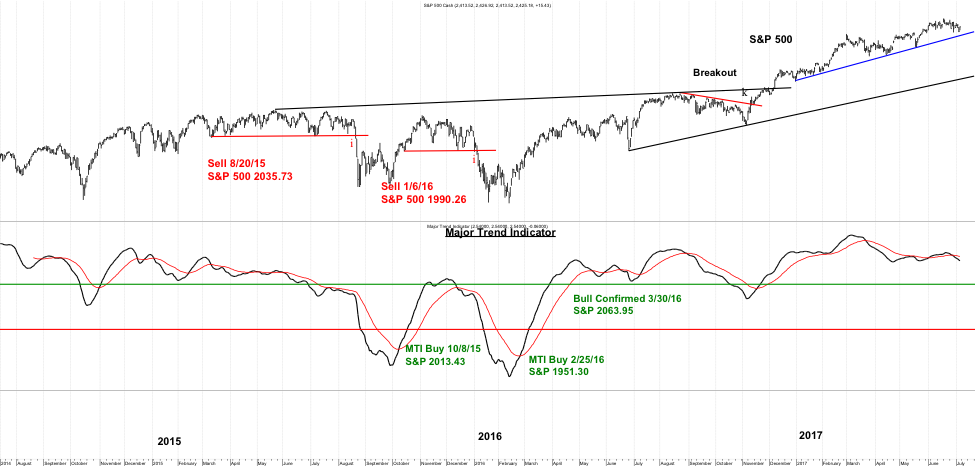

In recent years, market strategists have said that low interest rates justify a higher multiple for S&P 500 earnings. As interest rates climb, it will be more difficult to justify higher stock prices based on an expansion in the S&P 500’s P/E, which means earnings will have to do the heavy lifting. However, initial rate hikes have rarely been enough to derail a bull market and I don’t think this time will prove any different. The majority of long term technical indicators are still in good shape. The NYSE advance/decline line has recently made a new high. This is important since the majority of bear markets going back to 1928 have been preceded by a negative divergence in the A/D line. A divergence in the A/D line in October 2007 was one of the reasons I turned bearish and expected a bear market in 2008. My proprietary Major Trend Indicator (MTI) is still supportive of an ongoing bull market since it is comfortably above the green horizontal line. Notice how it fell below the green line prior to the declines in the summer of 2015 and early 2016. Finally, the S&P 500 is making higher highs and higher lows and is above the black trend line connecting the Brexit low in June 2016 and the early November low. The overall message from the charts and technical indicators is that after a correction, the S&P 500 is likely to at least test its prior high of 2453 and probably make a new high above 2500 before year end.

Jim Welsh

760-710-1956

@JimWelshMacro