Fundamentals not headlines ultimately drive financial markets. Although it is always tempting to listen to the news, successful investing depends (perhaps more than ever) on a dispassionate review of fundamentals. We’ve attempted to sift through the current noise to highlight what we think is important and not, and summarized them as “The Three Ps” of politics, profits, and probabilities.

Politics: ignore it.

Politics is about what should be. Investing is about what is. At RBA, we invest based on what “is.” Our sole goal is to invest successfully for our clients, and not to advocate a particular political position.

One might have liked President Obama or not, but there was a major bull market during his two terms. One may like President Trump or not, but the bull market is continuing. If one structured portfolios based on one’s views of what should be, one has missed all or part of the 8+ year bull market. Period. End of story.

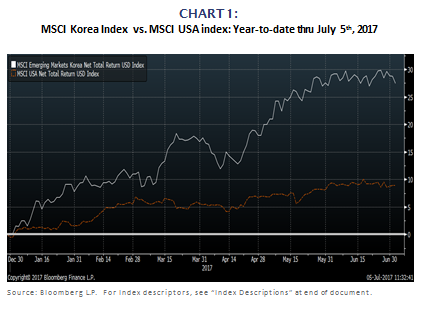

We pointed out last month that the recent performance of the South Korean stock market is glaring evidence of how listening to politicians can obscure potentially exciting investment opportunities. Although politicians have focused on the geopolitical risks associated with North Korea, the stock markets have focused on the fundamentals of South Korea. The South Korean stock market is up more than 25% year-to-date (in USD terms) and roughly tripled the return of the US stock market! (see Chart 1)

There may indeed be geopolitical risks associated with North Korea, but investors need to remember that fundamentals and not politicians’ desires to alter geopolitics ultimately drive stock markets.

Source: Bloomberg L.P. For Index descriptors, see “Index Descriptions” at end of document.

Profits: crucially important

Perhaps the primary distinction between RBA’s investment process and those of other firms is that RBA focuses on profit cycles and not economic cycles. That is a subtle, but extraordinarily important, difference because history shows the financial markets watch profit cycles whereas most investors follow economic cycles.

Profit cycles are more important than economic cycles because profits, and not GDP, are the heart of equity investing. When one is a partial owner of a company, as one would be when holding the stock of a company, then one’s sole concern is the profitability of their company and not the economic output of the entire country.

Our groundbreaking research in the early 1990s1 demonstrated that profit cycles were the essential factor behind size, style, sector, country, and asset rotation. RBA’s investment process today combines profits, liquidity, and sentiment based partly on this time- tested research.

Most investors focus on economic cycles and, as a result, can miss significant investment opportunities. There have been two dramatic examples just in the last five years or so:

1. It has been popular to suggest that the Fed’s immense liquidity injection into the US economy is the only reason the US stock market has appreciated. Investors see a strong bull market with US tepid real GDP growth of roughly 2% and conclude that the bull market must be highly speculative. However, these observers are missing that corporate profits became the largest portion of US GDP in history during the bull market (see Chart 2).

The bull market can more easily be explained if one examines profit cycles. The combination of record central bank liquidity and profits becoming the largest proportion of GDP better explains the bull market, and suggests the market is not as speculative as many believed.

2. It was consensus after the last recession that emerging markets were “growth” stock markets. Investors saw GDP growth that was 2-4 times the growth rate of the US economy. Yet, emerging market stocks underperformed US stocks for the next 5 years. That underperformance is easily explained if one considers profit cycles instead of economic cycles. The emerging markets’ profits growth was among the worst in the world (see chart 3).

When it comes to macro fundamentals, it may be critically important to ignore economic cycles and strongly concentrate on profit cycles.

Source: Richard Bernstein Advisors LLC, BEA.

Source: Richard Bernstein Advisors LLC, Bloomberg L.P., MSCI.

Probabilities: think realistically

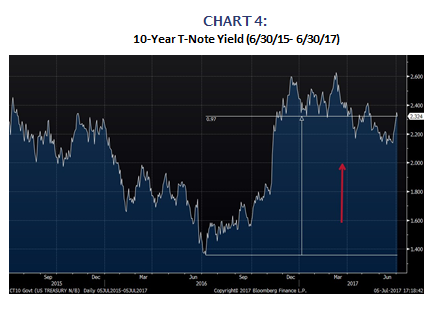

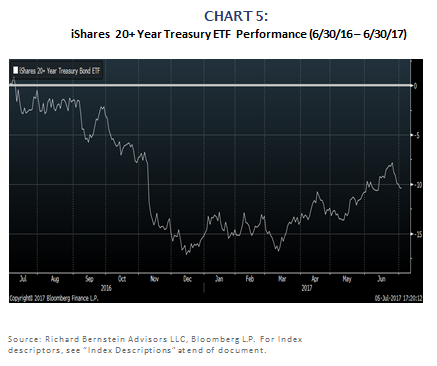

We think there is a reasonably high probability that the 10-year T-Note rate will be higher one year from today. One should not fall into a false sense of security by responding that people have been forecasting higher rates for some time and it hasn’t happened. One year ago, the 10-year rate was below 1.40%. Today, it is above 2.25%. 2.25% is indeed higher than 1.40%, so rates are indeed rising! (See Chart 4) In fact, investors have lost roughly 10% in the past year in long-term Treasuries (See Chart 5).

Source: Richard Bernstein Advisors LLC, Bloomberg L.P

Why would rates go up? Consider the following probabilities:

- What is the probability that there is some economic stimulus from Washington, DC? We think it’s reasonably high because the Republican House of Representatives will have to show results for the mid-term election in November 2018.

- What is the probability that the budget deficit gets larger? Again, we think it’s reasonably high because any stimulus package will necessarily expand the deficit before an increase in aggregate growth might cause the deficit to contract. There are lags between policy implementation and results, and deficits always expand during those lag periods.

- What is the probability that inflation is dead? We think it’s low. Inflation expectations have receded from last December’s, but they remain above the lows of a year ago and have recently started to climb again.

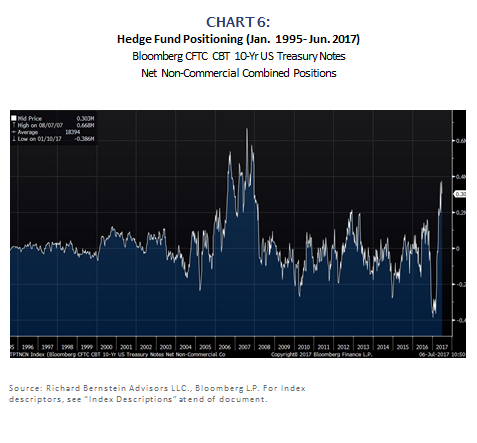

- What’s the probability that consensus is wrong? Again, we think it is reasonably high. Flows into bond funds and even hedge fund positioning demonstrates an overwhelming consensus that rates will fall. Chart 6 shows hedge funds' near-record long positioning in long-term Treasury bond futures.

Source: Richard Bernstein Advisors LLC., Bloomberg L.P.

The Three Ps

It’s a difficult period to determine what is important for investing and what isn’t. Just remember the three P’s.

Politics – Ignore it.

Profits – Critical to analyze.

Probabilities – Dispassionately assess.

INDEX DESCRIPTIONS:

The following descriptions, while believed to be accurate, are in some cases abbreviated versions of more detailed or comprehensive definitions available from the sponsors or originators of the respective indices. Anyone interested in such further details is free to consult each such sponsor’s or originator’s website.

The past performance of an index is not a guarantee of future results.

Each index reflects an unmanaged universe of securities without any deduction for advisory fees or other expenses that would reduce actual returns, as well as the reinvestment of all income and dividends. An actual investment in the securities included in the index would require an investor to incur transaction costs, which would lower the performance results. Indices are not actively managed and investors cannot invest directly in the indices.

US: MSCI US. The MSCI US is a free-float-adjusted, market- capitalization-weighted index designed to measure the equity-market performance of the United States.

Emerging Markets: MSCI Emerging Markets (EM) Index. The MSCI EM Index is a free-float-adjusted, market-capitalization- weighted index designed to measure the equity-market performance of emerging markets.

South Korea: MSCI Emerging Markets Korea Index. The MSCI EM Korea Index is a free-float-adjusted, market-capitalization-weighted index designed to measure the equity-market performance of South Korea.

10-Year Treasury Note: The Current United States 10-Year Government Note issued by the United States Treasury. Issue date: 5/15/2017, Maturity Date: 5/15/2027.

Long-term Treasuries: iShares 20+ Year Treasury Bond ETF. The iShares 20+ Year Treasury Bond ETF is an exchange-traded fund incorporated in the USA. The ETF seeks to track the investment results of an index composed of U.S. Treasury bonds with remaining maturities greater than twenty years.

Hedge Fund Positioning: Bloomberg CFTC CBT 10-Yr US Treasury Notes Net Non-Commercial Combined Positions. The Commitments of Traders (COT) reports provide a breakdown of each Tuesday’s open interest for markets in which 20 or more traders hold positions equal to or above the reporting levels established by the CFTC. A trader must report his or her position if at the daily market close, their position is at or above the CFTC’s reporting level in any futures month or option expiration. A trader is determined to be commercial or non- commercial using the following rational: All traders’ reported futures positions in a commodity are classified as commercial if the trader uses futures contracts in that particular commodity for hedging as defined in the CFTC’s regulations (1.3(z).

Corporate Profits IVA: Inventory Valuation Adjustment. The inventory valuation adjustment (IVA) is an adjustment made in the national income and product accounts (NIPAs) to corporate profits and proprietors’ income in order to remove inventory “profits“, which are more like capital gains than profits from current production.

Corporate Profits CCA: Capital Consumption Adjustment. The capital consumption adjustment (CCA) is used to adjust gross domestic product for the wear and tear of capital during the course of production. The result of this adjustment is net domestic product. The CCA is also the difference between gross private domestic investment (i.e., the total amount of investment expenditures for capital goods) and net private domestic investment.

© Copyright 2017 Richard Bernstein Advisors LLC. All rights reserved. PAST PERFORMANCE IS NO GUARANTEE OF FUTURE RESULTS

Nothing contained herein constitutes tax, legal, insurance or investment advice, or the recommendation of or an offer to sell, or the solicitation of an offer to buy or invest in any investment product, vehicle, service or instrument. Such an offer or solicitation may only be made by delivery to a prospective investor of formal offering materials, including subscription or account documents or forms, which include detailed discussions of the terms of the respective product, vehicle, service or instrument, including the principal risk factors that might impact such a purchase or investment, and which should be reviewed carefully by any such investor before making the decision to invest. Links to appearances and articles by Richard Bernstein, whether in the press, on television or otherwise, are provided for informational purposes only and in no way should be considered a recommendation of any particular investment product, vehicle, service or instrument or the rendering of investment advice, which must always be evaluated by a prospective investor in consultation with his or her own financial adviser and in light of his or her own circumstances, including the investor’s investment horizon, appetite for risk, and ability to withstand a potential loss of some or all of an investment’s value. Investing is subject to market risks. Investors acknowledge and accept the potential loss of some or all of an investment’s value. Past performance is, of course, no guarantee of future results. Views represented are subject to change at the sole discretion of Richard Bernstein Advisors LLC. Richard Bernstein Advisors LLC does not undertake to advise you of any changes in the views expressed herein.

© Richard Bernstein Advisors

Read more commentaries by Richard Bernstein Advisors