At Templeton Emerging Markets Group, we believe emerging market (EM) small-capitalization (small-cap) stocks represent an attractive proposition in the current investment climate. However, there are some common misconceptions regarding the asset class that conceal key strengths we believe an active manager could capitalize on. Here, I join my colleagues Stephen Dover, chief investment officer of Templeton Emerging Markets Group, and Chetan Sehgal, director of Global Emerging Markets/Small-Cap Strategies, to talk about investing in this space.

Overall, we believe small-cap stocks in emerging markets offer attractive prospects for active managers. A multitude of mispriced securities, market inefficiencies and a paucity of research provide considerable investment opportunities, in our view.

The Current Market Backdrop

So far in 2017, EM small-cap performance has been buoyant, with many countries and industries in the asset class advancing. Confidence in the market backdrop, economic environment and corporate earnings have improved across EMs. That confidence has come despite challenges such as actual and potential US interest-rate increases, uncertainty brought about by the new US administration and global geopolitical issues.

Addressing Some Common Misconceptions Surrounding EM Small Caps

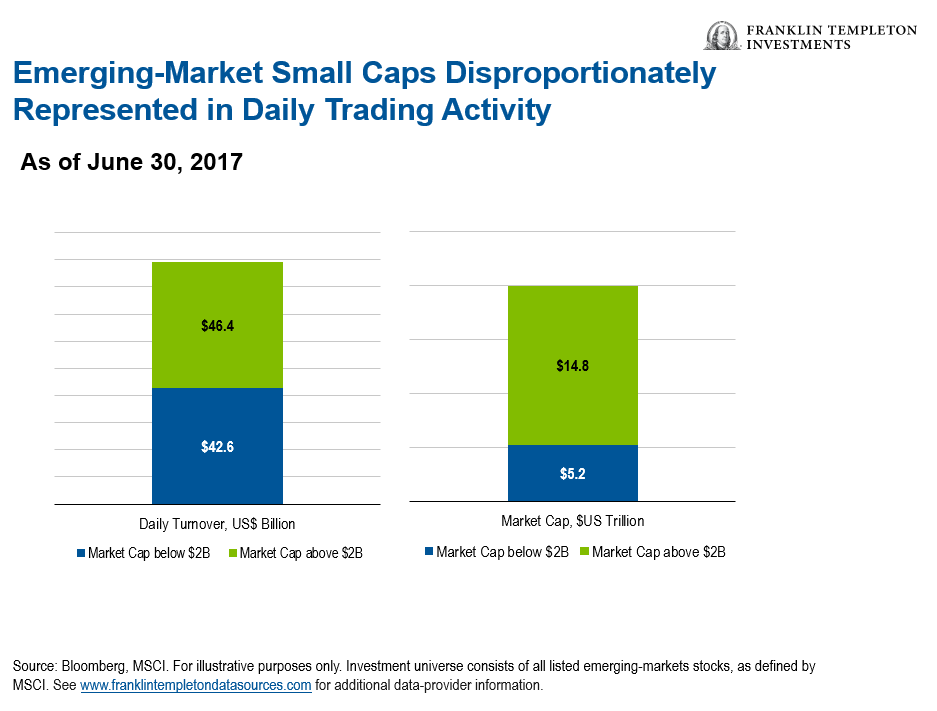

It Is Not a “Niche” Asset Class. Despite broad perceptions, in our view, EM small caps are far from being a niche investment. The asset class represents more than 20,000 companies with an aggregate market capitalization of over US$5 trillion and daily turnover of over US$40 billion, as the chart below demonstrates.1 Liquidity within EM small-cap markets is comparable to that of EM large caps.

Accordingly, we think the sheer size of the EM small-cap investment universe is a key advantage for active managers, providing abundant opportunities to uncover companies we think represent value. Ownership of EM small caps disproportionately sits with retail investors. Retail investors tend to trade more frequently than foreign institutional investors because the former usually have a far shorter investment horizon—boosting liquidity as a result. A good example of this is India, where investors have a vast number of smaller companies to choose from, and the skew of ownership is toward local investors.

A key difference between developed-market small caps and EM small caps is that EM small caps in many markets are often still significantly important locally. A market capitalization of close to US$2 billion could represent a leading company in a certain country, index or sector—perhaps a well-established business with a long and successful track record. Many of these companies are family owned or controlled, and many have stable profiles when compared with developed-market small caps.

It Is Not Necessarily a More Volatile Investment

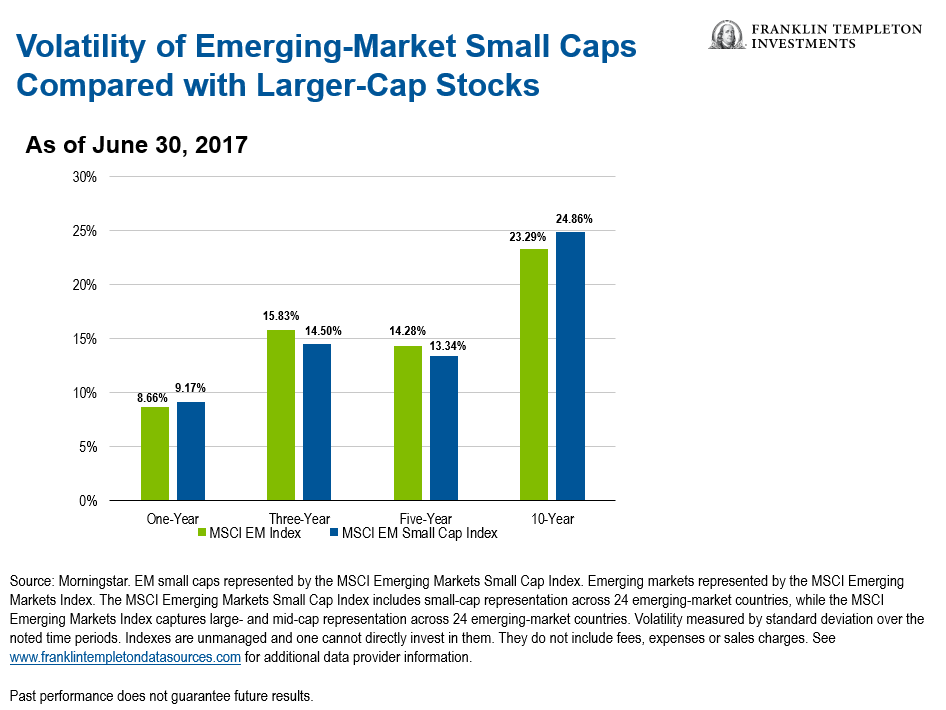

Another key misconception about investing in EM small caps is that volatility is higher than their larger-cap counterparts. Like all investments, EM small caps come with real and perceived risks. These include greater price volatility (particularly over the short term), relatively small revenues, limited product lines and a small market share. However, many of these risks are those associated with the EM equity universe overall, such as increased volatility relative to developed markets.

An analysis of standard deviations illustrates the assumption that EM small caps are much more volatile than larger-cap EM stocks does not always hold true. (See chart below)

Although individual stocks can indeed be very volatile, the correlations2 between different EM small-cap companies are often lower, which we believe in is due in part to the expansiveness and diversity of businesses within this investment space. The same factors that might impact a South Korean television and online shopping company’s stock, for example, would not likely impact an Indian cement company. This can help reduce correlation risk at the asset-class level.

Small-Cap Opportunities for Active Investors

Overlooked and Under-researched. Not only do many investment managers overlook EM small caps, they are also notably under-researched on the sell side. This reflects not only the vast number of companies to cover, but also the relative lack of information available. Unsurprisingly, the result is that the average number of stock research recommendations for EM small caps is much lower than for larger-cap stocks.1

Also, many small-cap stocks have little or no research coverage. For a large number of EM small-cap stocks outside of the benchmark MSCI index, research availability is even more limited. This can give a critical advantage to an active manager who can directly research such companies, especially if they have people on the ground in the region to evaluate them first hand. The probability of finding a relatively unknown off-index EM small-cap stock being mispriced is far greater than for a large company with many analysts producing research recommendations on it.

Recapturing Access to Local Exposure to Complement Existing EM Portfolios

Reflecting on the general long-term success of emerging markets, as global economies and as an equity asset class, most of these countries have become ever-more integrated into the world economy. Consequently, the largest and most successful EM companies have often expanded beyond their domestic markets to export and invest globally. Accordingly, domestic factors are no longer the primary drivers of the share prices of many of these stocks. Examples of such companies can include electronics, auto-industry or consumer-related names that derive a substantial portion of their revenues from developed economies rather than those in which they are based.

In contrast, EM small caps generally offer the very exposures that originally enticed many investors to emerging markets in general. Domestic demand, favorable demographics, local reform initiatives and innovative niche products are often the primary determinants of growth.

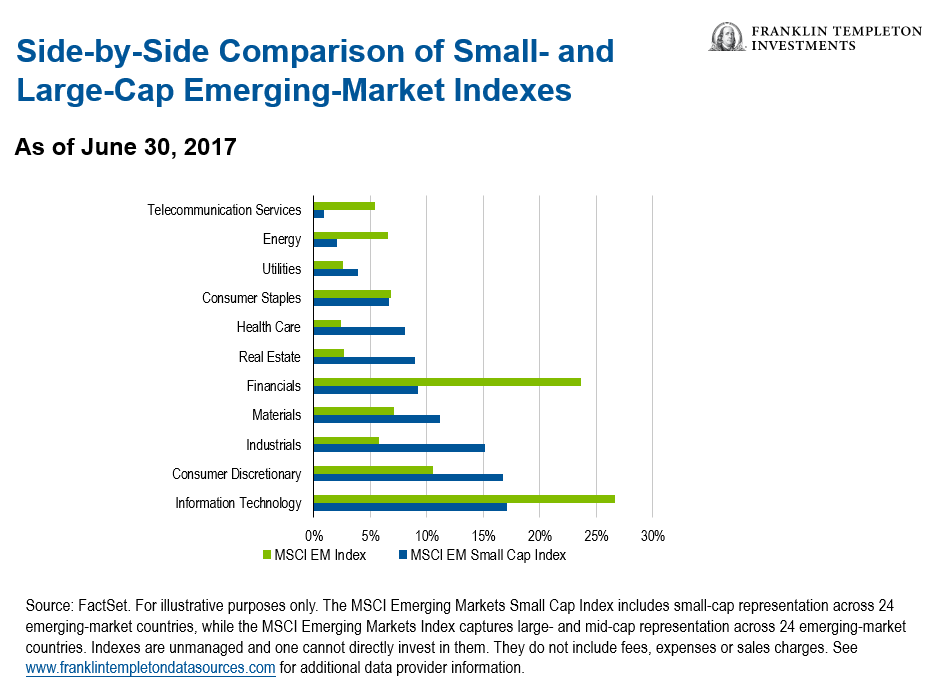

Consequently, the sectors to which EM small-cap investors are exposed differ notably from those of larger-cap stocks. The MSCI Emerging Markets Index is disproportionately dominated by exposures in information technology and financials, as indicated in the chart below. These sectors are typically more closely impacted by global or country-level macroeconomic trends.

In addition, state-owned enterprises are often more prevalent among larger-cap stocks. While we find many such state-owned companies to be well managed, the interests of the top owners are not always entirely aligned with those of minority investors.

In contrast, EM small-cap exposures are typically concentrated in higher-growth sectors, such as consumer discretionary and health care. Often these companies are more locally focused and many are relatively dominant players in smaller industries. The most successful EM small caps will leverage such local strength to expand internationally, supporting their transition into mid- or even large-cap companies over time.

Even within a given sector, economic exposures can differ substantially. For example, in the materials sector, mining companies by their nature are generally large-cap names and are impacted significantly by factors external to their home country, such as global commodity prices. EM small-cap materials companies include businesses such as cement producers, with greater exposure to local economic development and demand dynamics. Accordingly, diversifying into EM small caps can provide exposures that may complement an existing larger-cap-oriented EM allocation.

Finding Growth in a Low-Growth World

Emerging markets represent a possible bright spot in a sometimes uncertain world-economic landscape. Although global growth rates have consistently disappointed since the 2008 financial crisis, in April 2017 the International Monetary Fund (IMF) projected an expansion in global gross domestic product (GDP) growth from the 2016 level, to 3.5% in 2017.4 For advanced economies, the IMF’s GDP growth expectation for 2017 is at 2%.5 However, as has consistently been the case, the expected growth rate for EMs together with other developing markets, at 4.5%, sits solidly above the global rate.6

In such a low-growth world, investing in EM small caps may provide exposure to many of the fastest-growing companies in the fastest-growing countries globally.

Sales growth of EM small caps has also been higher than their larger-cap counterparts.7 It is also worth reiterating that this topline growth is typically organic and derived from local market dynamics, rather than being driven by global macroeconomic factors.

In addition to organic growth, EM small caps may also see share-price appreciation from being added to an index, thus attracting passive investor flows, and with additional sell-side research attention likely to increase active fund flows, too. They also may be potential merger-and-acquisition targets. These are growth drivers that are, to a great extent, independent of macroeconomic considerations.

Uncovering Success

Perhaps what is most important to recognize is that there are numerous EM small-cap companies that will likely remain small, whether due to corporate governance issues, poor quality of management, lack of market growth or other factors. The role of an active manager is to seek to determine which EM small-cap companies will succeed over the long term, with a view to reducing downside risk and thus enhancing risk-adjusted returns. With such a vast number of under-researched and under-owned companies in which to invest, a focus on bottom-up fundamentals can result in the construction of portfolios with highly attractive quality metrics at valuations lower than the EM small-cap index.

Our Active Focus

At Templeton Emerging Markets Group, we believe the EM small-cap space is fertile ground for active managers who can focus on risk management and zero in on long-term growth drivers for the asset class. Our EM small-cap research is driven by an extensive on-the-ground team of over 50 analysts in 20 offices globally, which allows us to have regular face-to-face meetings with prospective investments and our investee companies and gain first-hand understanding of the dynamics of the local markets in which they operate.

Our strong research efforts, with a focus on corporate governance and risk management, support our aim to deliver on the structural reasons for EM small-cap investing—seeking companies we believe are best positioned to benefit from the demographics and rising wealth of EM consumers, with sustainable and defendable business models.

Through our bottom-up approach, we look to invest in companies with good management teams where we feel conviction they can make the right strategic choices. Price is also crucial to our approach, with a value orientation driving our philosophy for EM investing, which has been honed over several decades

The comments, opinions and analyses expressed herein are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. Because market and economic conditions are subject to rapid change, comments, opinions and analyses are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy.

Important Legal Information

All investments involve risks, including the possible loss of principal. Investments in foreign securities involve special risks including currency fluctuations, economic instability and political developments. Investments in emerging markets, of which frontier markets are a subset, involve heightened risks related to the same factors, in addition to those associated with these markets’ smaller size, lesser liquidity and lack of established legal, political, business and social frameworks to support securities markets. Because these frameworks are typically even less developed in frontier markets, as well as various factors including the increased potential for extreme price volatility, illiquidity, trade barriers and exchange controls, the risks associated with emerging markets are magnified in frontier markets. Stock prices fluctuate, sometimes rapidly and dramatically, due to factors affecting individual companies, particular industries or sectors, or general market conditions. Smaller company stocks have historically had more price volatility than large-company stocks, particularly over the short term.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

__________________________________________________

1. Source: Bloomberg, as of 6/30/17.

2. Correlation measures the degree to which two investments move in tandem. Correlation will range between 1 (perfect positive correlation where two items have historically moved in the same direction) and -1 (perfect negative correlation, where two items have historically moved in opposite directions).

3. Source: Bloomberg, as of June 30, 2017. EM small caps represented by the MSCI EM Small Cap Index. Emerging markets represented by the MSCI Emerging Markets Index. Indexes are unmanaged and one cannot directly invest in them. They do not include fees, expenses or sales charges.

4. Source: IMF World Economic Outlook database, April 2017. There is no assurance that any forecast, projection or estimate will be realized.

5. Source: Ibid.

6. Source: Ibid.

7. Source: FactSet. EM small caps represented by the MSCI EM Small Cap Index. Emerging markets represented by the MSCI Emerging Markets Index. Indexes are unmanaged and one cannot directly invest in an index. They do not include fees, expenses or sales charges.

© Franklin Templeton Investments

© Franklin Templeton Investments

Read more commentaries by Franklin Templeton Investments