SUMMARY

- Will Bond Markets Need Saving?

- Brazil Still Hasn’t Come Clean

- Why The Fed Will Keep Tightening

I was raised by parents who lived through the Great Depression. They preached the ethic of thrift to my brother and me with fervor. We both began working before we were teenagers, and every nickel that we earned went into a savings account. Once a month, we’d parade into the bank to get our passbooks updated with the latest interest we had earned and parade out with a sense of pride.

Times have certainly changed since then. The fraction of young people who work while going to school has fallen sharply in the last generation, and nickels aren’t worth as much as they used to be. Passbooks have become a thing of the past, and few bank clients visit tellers anymore.

Perhaps the most significant change from the “good old days” is that my fellow baby boomers and I will soon begin spending the savings we have accumulated during our lifetimes. As this process accelerates across time and across geography, it will have a profound impact on global consumption and investment patterns. And it could create problems for countries that are indebted.

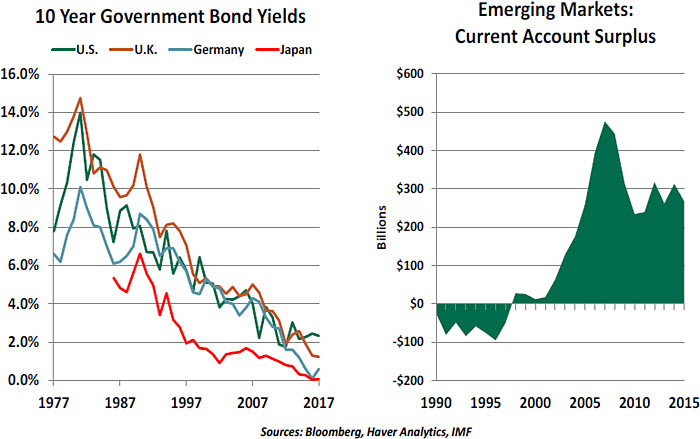

Long-term interest rates in developed markets have been on a 35-year secular decline, despite the fact that governments in developed markets have gone much more deeply into debt during that interval.

Many theories have been advanced to explain the fall in yields. Around the world, the commitment of central banks to controlling price levels have certainly strengthened, culminating in the adoption of formal inflation targets. Inflation expectations have been tamed, and the term premia demanded by fixed income investors has been reduced. More recently, the potential onset of secular stagnation has been added to the list of factors depressing borrowing costs.

Former U.S. Federal Reserve Chairman Ben Bernanke has taken a completely different tack. Beginning with a 2005 speech, and consistently thereafter, he has posited that growing pools of global savings have been the main root cause of falling long-term interest rates.

After the Asian financial crisis of the late 1990s, governments in developing countries saw the value of accumulating reserves to buffer against sudden capital outflows. Current account surpluses (which capture the amount of financial capital that a country is sending overseas) in emerging markets began to grow, and an important fraction of these amounts was invested in the safety of long-term bonds issued by Western governments. China has been an especially significant participant in this process.

At the same time, the wealth of private investors in developing countries began to expand. Seeking portfolio diversification and hard currencies, many of the newly rich also found value in developed-market debt. As their means and their anxiety about their domestic markets have increased, the appeal of Treasuries, gilts, and bunds has grown.

The nations receiving these inflows have been quite happy to accept them. Inbound foreign investment has limited debt servicing costs (for both governments and their citizens) and made it possible to finance rising debt levels. While there has been periodic anxiety over the potential that China might threaten to sell its U.S. Treasuries as a way of gaining leverage with the United States, it would be very difficult for China to find alternative markets that are as deep and liquid.

Unfortunately, the savings glut may be on the verge of diminishing. Official reserves in Asia and the Middle East have been dwindling as countries use them to address domestic challenges. Changes to global trade patterns, which are at risk from Brexit and the international posture of the U.S., could diminish the export earnings that have helped swell emerging market coffers.

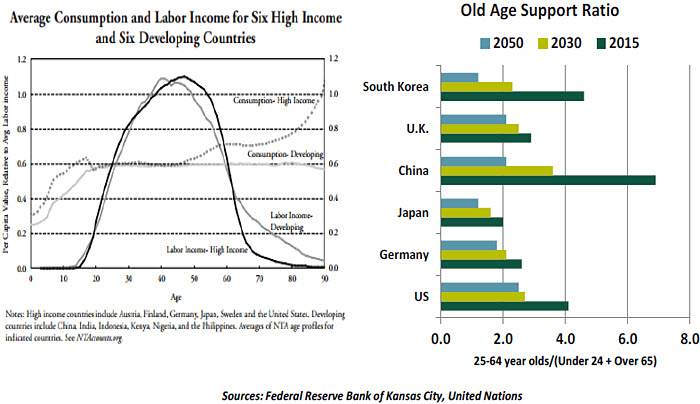

Most significantly, though, is the role that demographics will play in the global savings cycle over the coming decades. As shown in the left-hand chart below, people generally experience three phases during their lifetimes. The first is a period of development and education, where consumption exceeds income. The second is an interval of peak earnings, where savings accumulate. Those savings are then employed to sustain consumption in the third phase, which is retirement.

If populations were evenly distributed across age categories, the fraction of people in each phase would be constant over time. But because post-war generations in many countries were significantly larger than those adjacent to them, age profiles are now skewing toward the older. China is going through a similar progression because of its one-child policy, which was effective from 1979 to 2016.

In the years ahead, there will be millions of people moving from peak saving to peak dissaving. Several of Asia’s wealthiest nations, with some of the highest rates of saving in the world, will see a particularly steep transition. As retirees begin to liquidate their assets to support spending during retirement, the prices of those assets could fall. And if they are bonds, this means that the interest rates on those securities will rise.

If the availability of inexpensive overseas capital is curtailed, the interest burden for indebted countries would rise. This would add to annual deficits and, in the extreme, bring the sustainability of the debt into question.

It is premature to project disaster for either the bond market or sovereigns. The influence of demographics moves slowly, and other factors will certainly enter the picture in the coming decades. But governments might be wise to think more seriously about saving their nickels, euros, yuan and pounds. If they don’t, they may lose more than their senses of pride.

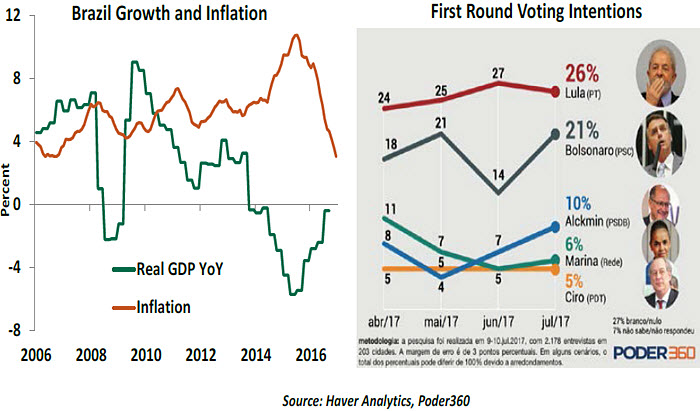

A Sad SambaAfter suffering three years of deep depression, the Brazilian economy recently got some good news when the International Monetary Fund upgraded Brazil’s outlook. However, an expected growth rate of 0.3% in 2017 is unlikely to do much for an economy that has contracted for three years running (gross domestic product is almost 8% smaller than it was at the start of 2014).

In the years leading up to the current crisis, the Brazilian economy had prospered, thanks to a combination of easy credit, generous government spending and strong commodity prices. As the first two became unsustainable and the commodity cycle turned, the euphoria around the Brazilian economy also died down. This coincided with the unearthing of numerous corruption scandals that implicated the top echelons of Brazilian polity and business. A slowing economy, rising prices, crumbling public services and a discredited leadership brought the public to the streets.

The country remains mired in a corruption scandal that has engulfed one ex-president, forced his successor to resign, and might still lead the incumbent to step aside. Even if current President Michel Temer is not forced to resign, he will likely be shown the door by the electorate in next year’s elections. Despite his unpopularity with voters (his approval ratings remain in single digits) and his alleged role in the corruption scandal, Temer has remained popular with the markets due to his sincere efforts towards reforming the economy.

The public unrest has died down over the last year due to a combination of public fatigue, disenchantment and stabilization of prices. Financial markets, too, have recovered since the slump witnessed in the spring on 2016, something that has allowed the central bank to loosen monetary policy. The economy is showing signs of life, but given the precarious position of President Temer, he is unlikely to go ahead with some necessary (but unpopular) reforms. The social security system is in particular need of attention.

Brazilian Presidential elections are scheduled for October 2018, and if the current polling trends hold, they are likely to cause jitters in the financial markets. Populist former President Luiz Inácio Lula da Silva, known simply as Lula, is likely to run another term, something that will allow him to get immunity from the corruption charges he currently faces. Lula’s party, the left wing Workers’ Party (PT), has been leading the polls for a while now. Coming second is the far-right Social Christian Party (PSC,) and Jair Bolsonaro is likely to be its candidate. Bolsonaro is closely allied to the Brazilian armed forces, and is likely to take a tougher stance on crime. Neither candidate is likely to inspire much confidence to follow through on tough economic reforms.

Despite improvements over the last year, Brazil has been an exception to the economic stability of the wider emerging markets universe. However, it is not the only one: South Africa and Turkey have also performed poorly. The former bears a close resemblance to Brazil, where spectacular corruption at the top and a commodity slump has brought about policy paralysis and an economic slowdown. Turkey is not too dissimilar, with its reliance on easy credit to keep the economy afloat. Although Turkey has its own political problems, which some might say are more grievous than those of Brazil or South Africa, President Erdoğan is unlikely to go anywhere in the foreseeable future.

But there is hope. In 2013, India witnessed the pernicious combination of slow growth, rising prices, large corruption scandals, policy paralysis and widespread public protests. A change in government not only delivered a change in mood, but has brought about significant reforms and macroeconomic stability - helped in no small measure by low oil prices. For Brazil, a paradigm shift is also possible, if there is a catalyst.

Too Easy

The Federal Reserve concluded its deliberations this week without making any changes to U.S. interest rates and without initiating the balance sheet reductions that had been

outlined in June. Its statement indicated this process would begin “relatively soon,” which we interpret to mean shortly after the September Federal Open Market Committee (FOMC) meeting.

The FOMC likely invested a good deal of time trying to understand inflation’s recent retreat, a puzzling development at such a late stage of the business cycle. Pending a good explanation, some within the FOMC have expressed hesitance to proceed with the normalization of American monetary policy.

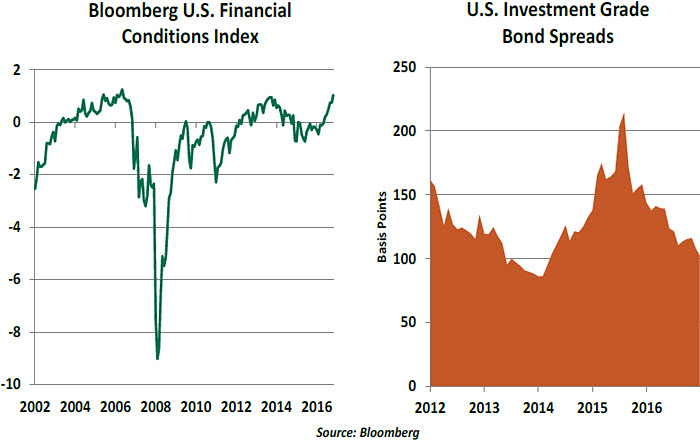

But the group probably also spent an important portion of its time together discussing financial conditions, which are nearly as easy as they were immediately prior to the 2008 financial crisis.

Monetary policy ultimately affects economic activity through its impact on the availability and cost of capital. By many measures, leverage has become cheaper and more readily available over the past year, even as the Fed has been raising short term rates and hinting at trimming its asset holdings. In particular, credit spreads have fallen by half in the past six months.

There are certainly good reasons why corporate bond yields have been on the decline. Business profits have been healthy, and so are most corporate balance sheets. The risk of default seems remote. The global economic outlook looks steady, so the good times could continue for a while. But some of the money going into the debt sector is arriving primarily because other asset classes are viewed as less attractive. Most feel that U.S. equities are not cheap, and cash yields are still relatively low.

The question is whether credit is priced for perfection. Spreads got very narrow ten years ago, amid confidence that the business cycle had been tamed. We know how that turned out, and the Fed risks a similar fate by leaving monetary conditions too easy for too long. It would be best to take out insurance against that outcome by staying the course of policy normalization.

© Northern Trust

www.northerntrust.com

© Northern Trust

Read more commentaries by Northern Trust

At the same time, the wealth of private investors in developing countries began to expand. Seeking portfolio diversification and hard currencies, many of the newly rich also found value in developed-market debt. As their means and their anxiety about their domestic markets have increased, the appeal of Treasuries, gilts, and bunds has grown.

At the same time, the wealth of private investors in developing countries began to expand. Seeking portfolio diversification and hard currencies, many of the newly rich also found value in developed-market debt. As their means and their anxiety about their domestic markets have increased, the appeal of Treasuries, gilts, and bunds has grown.

In the years ahead, there will be millions of people moving from peak saving to peak dissaving. Several of Asia’s wealthiest nations, with some of the highest rates of saving in the world, will see a particularly steep transition. As retirees begin to liquidate their assets to support spending during retirement, the prices of those assets could fall. And if they are bonds, this means that the interest rates on those securities will rise.

In the years ahead, there will be millions of people moving from peak saving to peak dissaving. Several of Asia’s wealthiest nations, with some of the highest rates of saving in the world, will see a particularly steep transition. As retirees begin to liquidate their assets to support spending during retirement, the prices of those assets could fall. And if they are bonds, this means that the interest rates on those securities will rise.

The FOMC likely invested a good deal of time trying to understand inflation’s recent retreat, a puzzling development at such a late stage of the business cycle. Pending a good explanation, some within the FOMC have expressed hesitance to proceed with the normalization of American monetary policy.

The FOMC likely invested a good deal of time trying to understand inflation’s recent retreat, a puzzling development at such a late stage of the business cycle. Pending a good explanation, some within the FOMC have expressed hesitance to proceed with the normalization of American monetary policy.