Why should anyone care about productivity? Although a seemingly dry concept, it is arguably the most significant driver of economic growth. When businesses and workers increase their productivity, they boost supply, putting downward pressure on prices. Higher productivity should also translate into higher wages. The combination of improved pay and lower prices should drive improved economic activity and higher living standards.

With demographic trends being weak in developed economies – the labor force is expected to fall in the coming decade in the US, Europe and Japan – strong productivity is key to achieving long-term sustainable growth for the Western economy.

The bad news is that we have been facing a long-term, structural decline in productivity growth. If this continues, it will damage future economic prospects and compel central banks to keep interest rates low for years to come. As a result, investors may need to factor in a challenging macroeconomic environment ahead.

Defining the productivity challenge

But what is productivity? The standard, though not only, measure of productivity is labor productivity – the output per hour worked divided by the labor input per worker. In other words, you divide what you get out by what you put in.

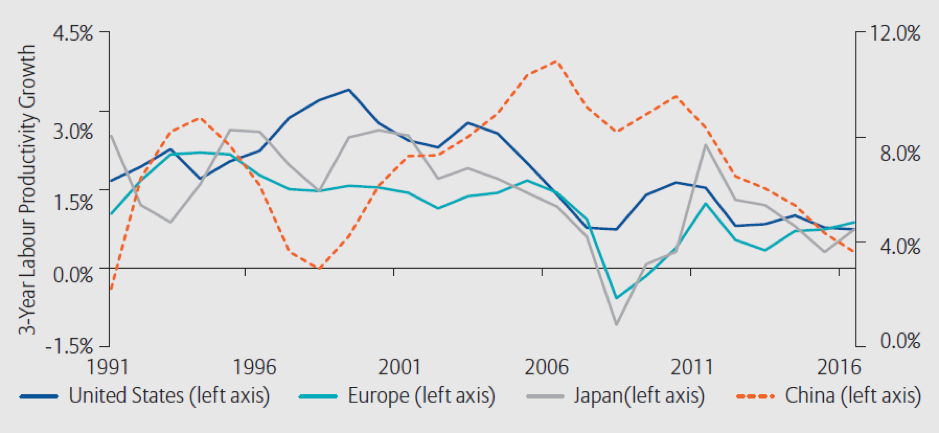

The numbers shown in the accompanying charts depict a worrying trend: Labor productivity growth has been trending downward for decades. In the US, despite a spike around the turn of this century, the overall trend is down. On a three-year centered average, productivity growth has dipped to 3.6% a year in China, compared with 10.9% in 2006.

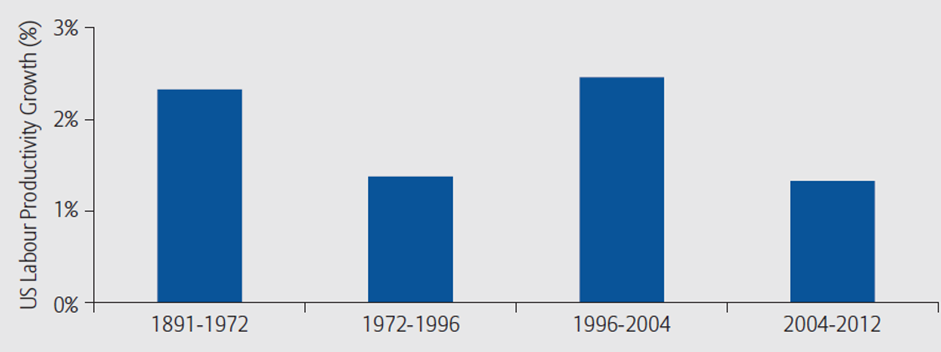

America has productivity problems

The world’s biggest economy’s labor productivity growth is below its 1970s level, reflecting the productivity malaise plaguing developed economies.

Source: “Is US Economic Growth Over? Faltering Innovation Confronts the Six Headwinds,” Robert J. Gordon, National Bureau of Economic Research, August 2012. Chart shows annual labor productivity growth from 1891-2012.

Why does this matter? Because, in a nutshell, lower productivity translates into lower gross domestic product (GDP) – a key measure of an economy’s overall size and health. As economic growth weakens, living standards may fall. These numbers raise pressing questions. For starters, how can productivity growth be falling when we seem to be working harder than ever? Besides, isn’t technology enabling us to be ever more efficient? And if labor productivity growth is dropping, how can we turn it around?

Why productivity growth is falling

In today’s global economy, troublesome supply and demand factors are pushing productivity lower. Economists disagree on which factors are most relevant – as economists always do – but the supply factors most often cited include:

- Diminishing returns from high-tech developments. Robert Gordon is among those economists arguing that the technological innovations with the biggest positive impact on productivity – such as electricity, the combustion engine and telephones – were invented during the second industrial revolution, which ended more than 100 years ago. Today’s innovations contribute less to improvements in living standards than those earlier breakthroughs.

- The global workforce is shrinking. Low unemployment rates, slowing growth, and an ageing population add up to a clear drag on productivity, particularly for Western companies. As baby-boomers drop out of the labor force – but not out of the total population – the hours worked per capita are shrinking. Output per capita is also falling as a result.

- An older workforce tends to be a less productive one. While it’s difficult to establish a precise relationship between age and productivity – because many different factors are at play – research suggests that people are typically at their most productive until around 55 years old. As populations age, this has implications for overall productivity levels. It also highlights an increasing social need to secure jobs for older workers, who are increasingly being forced to postpone retirement.

- Low interest rates allow unproductive use of capital. Some economists argue that sustained low interest rates, especially following the financial crisis – and, arguably, beforehand too – have helped to distort the price for money, leading to a misallocation of resources. Think, for example, of so-called zombie companies – those unproductive firms that are ailing financially. Low interest rates offer them life support by allowing them to borrow cheaply and roll over debt. In a normal rate cycle they may no longer exist. In addition, low interest rates may, paradoxically, deter investment by companies, because the “opportunity cost” of leaving the cash on balance sheet is so low.

- Startup activity has been falling for decades. The current hype around technology startups masks a less encouraging fact about an overall decline in startup activity. In the US alone, the number of new companies as a share of all businesses actually dropped 44% between 1978 and 2012. While new companies typically play a disproportionate role in boosting innovation, productivity and job creation, the US startup rate is, in fact, in long-term decline.

In addition to these key issues related to the supply of goods and services, the productivity challenge is amplified by demand factors:

- Uncertainty and deglobalization are dragging demand lower. Demand is being weighed down due to the rise in political uncertainty, the move away from globalization and high levels of leverage in the global economy – among other factors.

- Low rates mean debt-fueled shopping. Increasingly, demand is not driven by product manufacturing or corporate requirements but by online services and an end consumer who is paying for it through access to debt, which is issued by a central bank that is attempting to reflate its economy.

- Demographics are compounding the lack of demand. An ageing population consumes less, except for health care, and creates a capital shortfall that can be filled only through increasing amounts of leverage or debt.

Globally, productivity has been declining for years

Developed-market productivity growth has been falling for decades; China’s fell almost two-thirds in the last 10 years.

Sources: AllianzGI, Conference Board as at 12/31/2016. Chart shows 3-year centred average.

Can technology turn the trend around?

Given the clear downsides of lower productivity, and the limitations of using debt to spur growth, it seems to be imperative to find new ways to turn the productivity trend around.

On the face of it, new technologies should help to enhance productivity as the workforce shrinks and demand weakens. But today’s tech-based innovation is potentially less transformative than even the introduction of the desktop PC. In addition, much of the technology innovation we experience in our daily lives is focused on lifestyle and entertainment options, which contribute less to economic growth.

The technologies that represent the biggest potential wins for business – such as big data, artificial intelligence and the internet of things – are complex to implement and integrate, and may take years to come into their own. While there’s no cause for pessimism, we should not expect technology to be an automatic driver of productivity. Another challenge is the question of when to invest: Why spend money on IT now if something cheaper and more powerful will exist in two years’ time?

Incentivizing R&D

That said, investment and innovation are vital to solving the productivity puzzle. This means companies need to be incentivized to invest in research and development (R&D). They need to look to the long term. Those that focus only on achieving a higher stock price today – by clinging to legacy franchises and failing to disrupt themselves – may find they don’t have a franchise at all in the future. In addition – as we will address in a future article – industries can no longer rely on low-cost manufacturing in China and other emerging markets to mask productivity problems back home.

Governments have a key role to play in fixing this issue. True R&D is often derived from raw science and funded by the public sector, government and universities. Periods of innovation and productivity have often followed economic crises or war, and it is that kind of urgency – the need to find a solution quickly – that should inspire business, governments and investors to take up the challenge and define a new productivity paradigm for our age.

_____________________________________________________________________________________

Subscribe to Get Neil’s Insights Via Email

Neil Dwane’s insights are available as a monthly email subscription for financial professionals only. Your email address must be in our records for your subscription to take effect.

Follow Us on Twitter

For more investment insights and market perspectives from our global research network, follow @AllianzGI_US on Twitter or visit us.allianzgi.com.

Important Information

The material contains the current opinions of the author, which are subject to change without notice. Statements concerning financial market trends are based on current market conditions, which will fluctuate. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities. Forecasts and estimates have certain inherent limitations, and are not intended to be relied upon as advice or interpreted as a recommendation.

Past performance of the markets is no guarantee of future results. This is not an offer or solicitation for the purchase or sale of any financial instrument. It is presented only to provide information on investment strategies and opportunities.

Allianz Global Investors Distributors LLC, 1633 Broadway, New York NY, 10019-7585.

1 800 926 4456

us.allianzgi.com