One axiom of investing is that taking risk results in higher portfolio returns over the long-term, but hiding in safe haven investments during times of stress is prudent. Fortunately, the global economy expands more than it contracts, so it has paid through time to avoid safe havens and take risk. For example, our research in the early-1990s clearly showed that lower quality stocks outperformed higher quality stocks over the long-term, but investors had to be willing to accept the risk that goes along with such volatile investments’ higher returns. Low quality investments, like smaller capitalization stocks and “junk” bonds, show similar long-term return and volatility characteristics.1

A strong and vocal consensus has recently formed that it is again time to hide. Although we don’t agree with the assessment that a bear market is at hand, it is both interesting and disconcerting to see that global investors apparently no longer see the United States as a global safe haven. Of course, treasuries have rallied based on investor fear, but US assets in general are being devalued relative to those outside the United States.

The weak dollar

The recent 11-12% decline in the US dollar (see Chart 1) during a period of increasing fear seems extremely important. The recent fall in the value of the USD is not unprecedented at all, but the juxtaposition of the weakness and increasing investor fear seems unusual.

Forecasts of non-US growth being superior to US growth and the related fund flows can explain some of this. However, the USD’s fall appears more worrisome when one examines the USD relative to the currencies of global “hot spots”.

CHART 1: Dollar Index Spot

Charts 2 and 3 compare the US dollar to the South Korean won (KRW) and the Japanese yen (JPY). One would think the KRW would be quite weak given the saber rattling of North Korea, but that isn’t the case. The KRW has been flat versus the USD since North Korea started its string of recent missile tests in April. Meanwhile, the JPY has actually appreciated versus the USD despite that North Korea recently tested a missile that actually flew over Japan.

CHART 2: South Korean Won - USD Spot

CHART 3: Japanese Yen - USD Spot

Source: Bloomberg Finance L.P. For Index descriptors, see "Index Descriptions" at end of document.

One might suggest that Asian fundamentals are better than US fundamentals, and that the weakness in the USD versus these currencies reflects the relative improvement of Asian fundamentals rather than a loss of confidence in the US assets. That more optimistic view may indeed be true, but it doesn’t explain the USD depreciation versus regions where fundamentals are not as attractive as they are in the US.

Chart 4 shows the appreciation of the euro (EUR) versus the USD. European fundamentals are improving somewhat, but are not as strong as those in the US. In addition, European monetary policy remains much looser than US monetary policy despite both regions’ central banks’ incremental restraint.

CHART 4: Euro - USD Spot

Source: Bloomberg Finance L.P. For Index descriptors, see "Index Descriptions" at end of document.

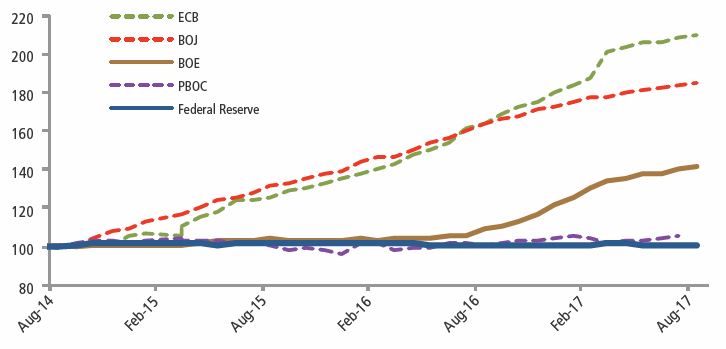

Chart 5 shows major central banks’ balance sheet growth. Whereas the Fed’s balance sheet growth has been flat for some time, the ECB’s balance sheet has continued to grow. One would think that the combination of better US fundamentals and tighter monetary policy would be supportive of the USD, but clearly that has not been the case.

CHART 5: Central Bank Balance Sheet Expansion Past 3 Years as of 8/31/2017

Source: Richard Bernstein Advisors, LLC., Federal Reserve, European Central Bank, The People's Bank of China, Bank of Japan, Bank of England, Bloomberg Finance L.P. * PBOC lags a month

Gold breaks out…in USD

Gold has broken out in USD terms, but not in terms of other major currencies. Chart 6 shows the year-to-date performance of gold in USDs and in EURs. In USD, gold is up about 17% year-to-date, whereas it is up only 3% in EUR.

This chart (Chart 6) truly questions the “safe haven” status of the US. Again, the performance disparity of gold in US dollars is not necessarily unusual, but investors should take note that the current performance spread does not appear fundamentally driven. Inflation expectations in the US have not been robust either on an absolute basis or relative to expectations of European inflation. Rather, it seems that the US is perceived to be riskier than other countries.

CHART 6: Gold

Source: Bloomberg Finance L.P. For Index descriptors, see "Index Descriptions" at end of document.

We remain bullish

While one cannot be certain about the US’s stated willingness to use military options in Latin America, the Middle East, or Asia, we remain more bullish than consensus. US and global fundamentals remain healthy, liquidity is ample, and investor sentiment largely remains morose.

Nonetheless, one has to wonder whether global investors are losing religion. Could the US be losing its safe haven status? Ultimately, we don’t think so, but there are certainly some strange things happening these days which taken all together could be a good argument that investors no longer believe the US is the safe haven.

INDEX DESCRIPTIONS:

The following descriptions, while believed to be accurate, are in some cases abbreviated versions of more detailed or comprehensive definitions available from the sponsors or originators of the respective indices. Anyone interested in such further details is free to consult each such sponsor’s or originator’s website.

The past performance of an index is not a guarantee of future results.

Each index reflects an unmanaged universe of securities without any deduction for advisory fees or other expenses that would reduce actual returns, as well as the reinvestment of all income and dividends. An actual investment in the securities included in the index would require an investor to incur transaction costs, which would lower the performance results. Indices are not actively managed and investors cannot invest directly in the indices.

Dollar Index Spot. The Dollar Index Spot (DXY) US.

South Korea Won – USD Spot : The South Korean won (KRW) is the official currency of The Republic of Korea (South Korea). The US dollar (USD) is the official currency of the United States of America. KRWUSD Spot Exchange Rate = Price of 100 KRW in USD

Japanese Yen – USD Spot : The Japanese yen (JPY) is the official currency of Japan. The US dollar (USD) is the official currency of the United States of America. JPYUSD Spot Exchange Rate - Price of 1 JPY in USD

Euro– USD Spot: The euro (EUR) is the official currency of the European Economic & Monetary Union. The US dollar (USD) is the official currency of the United States of America. The EURUSD Spot = Price of 1 EUR in USD.

Gold in USD: The Gold Spot price is quoted as US Dollars per Troy Ounce.

Gold in Euros: The Gold Spot cross rate in Euros.

© Copyright 2017 Richard Bernstein Advisors LLC. All rights reserved. PAST PERFORMANCE IS NO GUARANTEE OF FUTURE RESULTS

Nothing contained herein constitutes tax, legal, insurance or investment advice, or the recommendation of or an offer to sell, or the solicitation of an offer to buy or invest in any investment product, vehicle, service or instrument. Such an offer or solicitation may only be made by delivery to a prospective investor of formal offering materials, including subscription or account documents or forms, which include detailed discussions of the terms of the respective product, vehicle, service or instrument, including the principal risk factors that might impact such a purchase or investment, and which should be reviewed carefully by any such investor before making the decision to invest. Links to appearances and articles by Richard Bernstein, whether in the press, on television or otherwise, are provided for informational purposes only and in no way should be considered a recommendation of any particular investment product, vehicle, service or instrument or the rendering of investment advice, which must always be evaluated by a prospective investor in consultation with his or her own financial adviser and in light of his or her own circumstances, including the investor’s investment horizon, appetite for risk, and ability to withstand a potential loss of some or all of an investment’s value. Investing is subject to market risks. Investors acknowledge and accept the potential loss of some or all of an investment’s value. Past performance is, of course, no guarantee of future results. Views represented are subject to change at the sole discretion of Richard Bernstein Advisors LLC. Richard Bernstein Advisors LLC does not undertake to advise you of any changes in the views expressed herein.

© Richard Bernstein Advisors LLC