Separately, transaction volume, which is a major driver of financing demand, remains well above historical averages despite having declined since early 2016. In fact, volume this year is still expected to be the fourth-highest on record, according to Moody’s/RCA. Institutional investors have generally continued to increase their CRE allocations. Private equity real estate funds have over $250 billion of dry powder, a record, according to Preqin.

The confluence of these factors should create attractive opportunities for more flexible lenders not constrained by the regulatory requirements or risk constraints faced by banks and insurance companies.

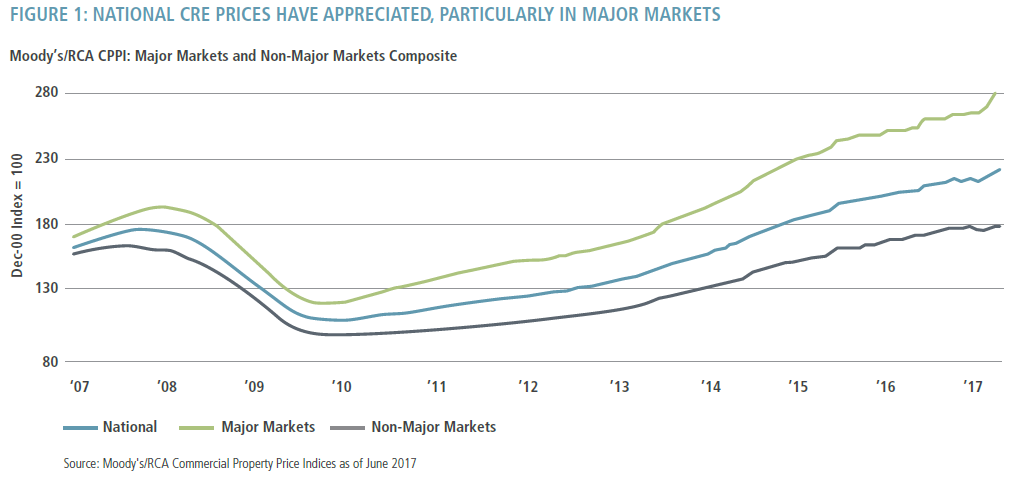

Q: Nine years after the global financial crisis, where do you see the greatest unmet borrower needs?

Thompson: As Devin discussed, banks have grown conservative by necessity. This has resulted in property buyers having to invest more equity than in the pre-crisis period. While banks previously loaned up to 70% against value, loan-to-value (LTV) ratios today are capped closer to 60% to 65%. Much of this is driven by regulations and by the Office of the Comptroller of the Currency (OCC), which in 2016 raised concerns about growing concentration risk and loosening underwriting standards in banks’ CRE credit loan portfolios. Banks have since tightened up where they lend, whom they lend to, and at what levels they are lending.

In addition, as Devin mentioned, the banks are much less active in the CMBS new issue market, and as a result, have held more whole loans on their balance sheets than pre-crisis.

As the “credit box” continues to contract, the list of “have-nots” continues to grow. Borrowers with the greatest needs have assets outside top markets - in areas such as Brooklyn, Austin, Dallas and Seattle - but have significant size and liquidity. They typically require loans with LTV ratios above 65%, own transitional/non-income-producing properties, lack established relationships with banks, or seek floating-rate financing.

Q: Are these borrowers the source of the most attractive opportunities today?

Thompson: Yes, outside of the top-tier markets, there are limited options for borrowers seeking 65%–80% leverage on loans greater than $50 million. A recent example is an office building in Brooklyn with direct views of Manhattan. The asset, a historic landmark, was redeveloped by a global institutional sponsor and is stabilized. The $250 million first mortgage loan would have a 70% LTV. Based on recent comparables, we would expect this to result in a 10% levered yield.

Q: How do investors avoid the mistakes that led to the last downturn in real estate?

Thompson: We believe there are three critical elements to CRE credit underwriting. First is having a disciplined and systematic approach to loan terms and covenant packages. One needs to be willing to walk away from a deal if taking it means giving up important lender protections. Second is sponsor quality, where we focus on borrowers with strong capital reserves and a long-term view of their position in real estate markets. Finally, we use our real estate team and experience as an active real estate equity investor, supplemented, as necessary, with our local market relationships, to form a detailed, robust view of the value and risks associated with the underlying real estate asset. We do not rely on appraisals. We believe that adhering to these principles helps to mitigate losses and gives loan portfolios the potential to perform materially better in times of economic stress.

Q: What differentiates PIMCO’s approach to CRE debt investing?

Chen: We are an experienced team of real estate investors – we’ve been investing in both the real estate equity and debt markets over many years and cycles. In the process, we have developed a deep understanding of real estate underwriting and a broad network of local contacts.

Our real estate team is part of an organization in which credit research is a critical component of our overall investment DNA. We benefit from PIMCO’s status as one of the world’s largest CMBS investors, which gives us access to an immense source of data that informs us of market dynamics. The firm’s credit research team also provides a key advantage – we work closely with our colleagues who cover corporate credit to assess the risk of any major tenant exposure in our real estate holdings. The ability to assess the full spectrum of risk for a property, whether it be “bricks and mortar” real estate issues or the likelihood of a major tenant defaulting, is critical to our underwriting process.

We combine this bottom-up analysis with top-down insights, which reflect our firm’s views on macroeconomic factors such as economic growth, interest rates, demographics and employment. Our views on markets and macroeconomics are refined at our regular cyclical and secular forums, which bring together PIMCO investment professionals and outside experts from around the world for several days of intense debate. These forums are particularly helpful in identifying trends or risks that may affect real estate capital markets or property types.

PIMCO has made significant investments to develop proprietary analytics. We believe these give our CRE lending platform a competitive advantage and provide a unifying framework for evaluating investment opportunities. We work closely with our analytics team to determine relative value and to help ensure that pricing properly reflects the structure of the loan. For instance, our analytics team helps us appropriately price into our loans the optionality of borrower behavior – i.e., the likelihood that the borrower extends the maturity date or pays off the loan before maturity. This is a critical element of loan structuring for transitional assets, one which is too often ignored.

Finally, we see a significant advantage to being a “one-stop” lender to borrowers who do not fall neatly into the box required by traditional, regulated lenders. To those borrowers, we are able to offer flexibility, speed and certainty of execution.

For more information about PIMCO alternative strategies, please contact your account manager.

Past performance is not a guarantee or a reliable indicator of future results. All investments contain risk and may lose value. Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. Investments in commercial real estate debt and mortgage loans are subject to risks that include prepayment, delinquency, foreclosure, risks of loss, servicing risks and adverse regulatory developments, which risks may be heightened in the case of non-performing loans. Mortgage- and asset-backed securities may be sensitive to changes in interest rates, subject to early repayment risk, and while generally supported by a government, government-agency or private guarantor, there is no assurance that the guarantor will meet its obligations. The value of real estate and portfolios that invest in real estate may fluctuate due to: losses from casualty or condemnation, changes in local and general economic conditions, supply and demand, interest rates, property tax rates, regulatory limitations on rents, zoning laws, and operating expenses. Management risk is the risk that the investment techniques and risk analyses applied by PIMCO will not produce the desired results, and that certain policies or developments may affect the investment techniques available to PIMCO.

Forecasts, estimates and certain information contained herein are based upon proprietary research and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Statements concerning financial market trends are based on current market conditions, which will fluctuate. There is no guarantee that these investment strategies will work under all market conditions or are suitable for all investors and each investor should evaluate their ability to invest long-term, especially during periods of downturn in the market.

This material contains the opinions of the manager but not necessarily those of PIMCO and such opinions are subject to change without notice. This material has been distributed for informational purposes only. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America L.P. in the United States and throughout the world.

©2017, PIMCO.

© PIMCO

Read more commentaries by PIMCO