K2 Advisors seeks to add value through active portfolio management, tactical allocation and diversification across four main hedge strategies: long/short equity, relative value, global macro and event driven. In their fourth-quarter (Q4) 2017 outlook, K2 Advisors’ Research and Portfolio Construction teams share the key market events they have an eye on. We believe offering these insights will help investors better understand the rationale for owning retail mutual funds that invest in hedge strategies.

Two Sides to Every Story—and the Truth

In a recent Bloomberg interview, legendary investor Howard Marks of Oaktree Capital said that investing is “never black or white, in or out, risky or safe.” He suggested that investing is about continually calibrating your portfolio across a spectrum of risk—from aggressive to defensive. We could not agree more.

The media likes to hear market calls. They like pundits who say “get out now,” “buy now,” or “it’s time,” etc. We don’t believe anyone can ever be that certain. Most of the time the correct action is somewhere in between. We can never know what the future will hold, but we can get a sense of potential outcomes by looking at what the past gave us, and where we stand in the present. The amount you have invested, your exposures across various asset classes and sectors and the presumed riskiness of each in the context of the current market. These are all things we can consider.

So where do we stand today? From our perspective things are looking a bit frothy. Again, this is not a market call. This rally could continue on for another year or even longer—who could know? What we do know is where we are relative to historical context.

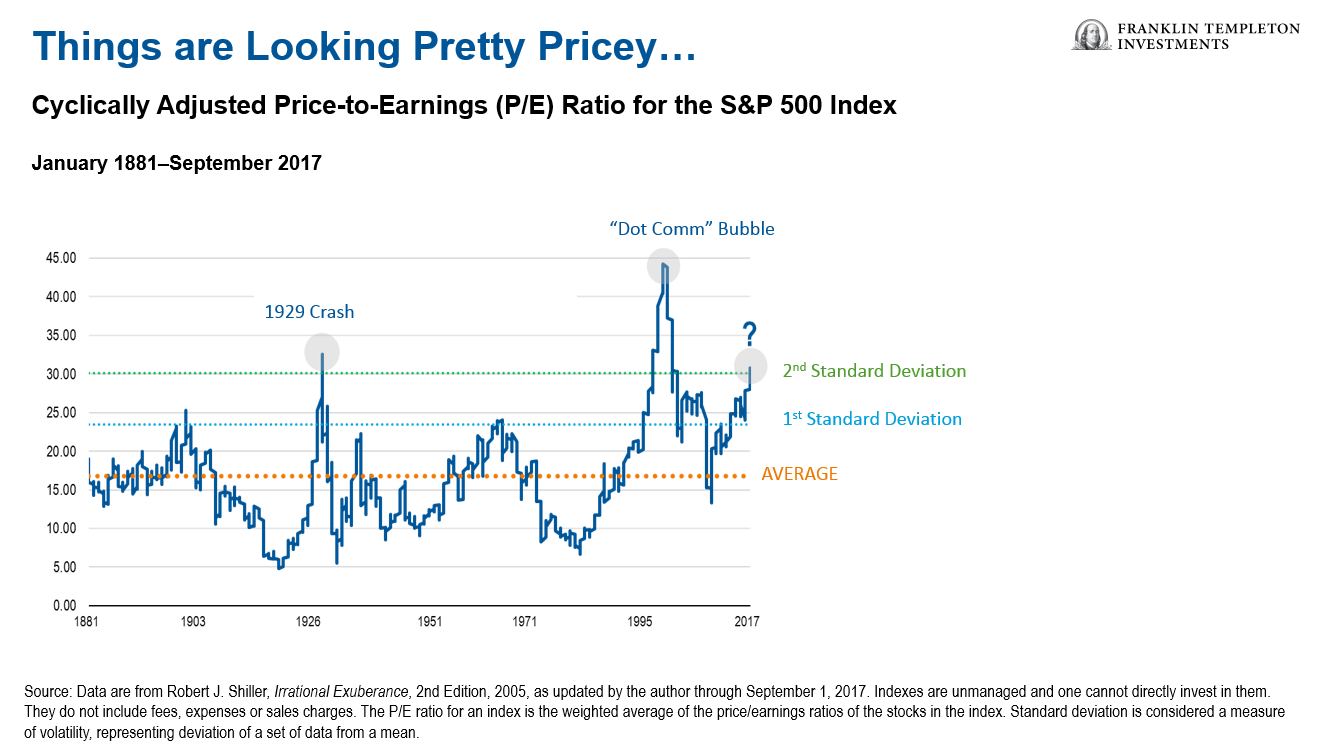

Consider the equity markets, for example. The chart below shows the Cyclically Adjusted Price-to-Earnings ratio (CAPE), which is a way of assessing the value of stocks in the S&P 500 Index.

The CAPE has only been this high three times before: 1929 (leading to the Great Depression), 1999 (during the dot-com bubble), and in 2007 (during the housing bubble leading up to the Great Recession).

The point is, while we cannot predict market tops or bottoms, we can be prudent in how we position portfolios contextually. Perhaps now is the time to consider dialing back risk to some degree. We believe the easy money in this cycle has already been made.

Perhaps it’s time to “risk adjust” portfolios and emphasize “alpha markets,” where hard work and skill may add to returns without significantly adding to risk exposures.

Quality “beta markets” that may offer lower-risk and steadier returns are, in our view, in short supply today. As Marks said, “it’s always about how it’s priced. . . . when we’re getting value cheap, we should be aggressive; when we’re getting value expensive, we should pull back.”

Inflation expectations appear flat and may even be drifting lower. Perhaps we should have waited for more data to see if the recent drop in inflation is indeed “transitory” as Federal Reserve (Fed) Chair Janet Yellen’s statements seem to suggest. Perhaps not. Only time will tell.

Dialing up Long/Short Equity Global

We maintain a constructive outlook for long/short equity investing, despite our measured outlook on overall market levels. We have adjusted our focus from Europe to global non-sector.

We believe certain trends such as stocks reacting to fundamentals, lower stock correlations, and increased dispersion are likely to continue to be tailwinds for long/short equity performance over the next 12 months. Corporate earnings and economic growth also remain robust—most notably in the United States.

In addition, rising interest rates have resulted in short rebates turning positive for the first time in more than eight years for many managers. We expect this to persist.

The Fed and other central banks have been pumping tremendous liquidity into the system since 2008, compressing spreads globally and really driving risk-asset flows. In our view this is poised to end, and when it does, it will be an inflection point in the markets.

Just like the Fed, the Bank of England has telegraphed to the market that it is going to pull some liquidity out of the system. We expect the same from the European Central Bank.

Relative Value – Fixed Income

In our view, the high-yield market has never been more interest-rate sensitive. Investors have been lulled into complacency, with the consensus view that rates will stay lower for longer. This is a very different narrative from the thinking when US President Donald Trump was first elected.

While rates have remained low, duration1 is still a significant and prevalent risk in many fixed income investors’ portfolios. We believe that relative value fixed income managers, such as long/short credit managers, are well positioned to mitigate this risk given their shorter duration portfolios. We expect these managers can generate alpha from rising sector dispersion as rates rise, which we fully expect.

Macro Commodity Trading Advisor (CTA) on the Rise

We define global macro CTA as intermediate-to-long-term systematic investing and trend following. We think it’s an interesting time to be in the strategy because we are just starting to come out of a technical drawdown. In our experience, that’s been one of the better entry points to be in the strategy. The Btop50 Macro/CTA Index has had four sizable drawdowns in its 30-year history, and June 30, 2017, was the bottom of the fifth such drawdown.2 We view the recovery as already underway, beginning in July and August 2017. The average recovery from the bottom of the prior four major drawdowns was 21.8% over the following 12 months.3 Of course, past performance cannot guarantee future results.

In short, the strategies appear to us to have entered a recovery phase, benefiting from stronger trending markets and an improved correlation environment.

Comments, opinions and analyses expressed herein are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. Because market and economic conditions are subject to rapid change, comments, opinions and analyses are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy.

This information is intended for US residents only.

What Are the Risks?

All investments involve risks, including possible loss of principal. Investment in these types of hedge-fund strategies is subject to those market risks common to entities investing in all types of securities, including market volatility. There can be no assurance that the investment strategies employed by hedge fund and liquid alternative managers will be successful. It is always possible that any trade could generate a loss if the manager’s expectations do not come to pass. Hedge strategy outlooks are determined relative to other hedge strategies and do not represent an opinion regarding absolute expected future performance or risk of any strategy or sub-strategy. Conviction sentiment is determined by the K2 Advisors’ Research group based on a variety of factors deemed relevant to the analyst(s) covering the strategy or sub-strategy and may change from time to time in the analyst’s sole discretion.

For more information on any of our funds, contact your financial advisor or download a free prospectus. Investors should carefully consider a fund’s investment goals, risks, sales charges and expenses before investing. The prospectus contains this and other information. Please read the prospectus carefully before investing or sending money.

_________________________________

1. Duration is a measurement of a bond’s sensitivity to interest-rate movements.

2. Source: Bloomberg LP. Data from January 1987 to August 2017. See www.franklintempletondatasources.com for additional data provider information. Indexes are unmanaged and one cannot directly invest in them. They do not include fees, expenses or sales charges. Past performance is not an indicator or a guarantee of future performance.

3. Ibid.

© Franklin Templeton Investments

© Franklin Templeton Investments

Read more commentaries by Franklin Templeton Investments