Templeton Emerging Markets Group has a wide investment universe to cover—tens of thousands of companies in markets on nearly every continent. While we are bottom-up investors, we also take into account big-picture context. Here, I share the team’s overview of what has happened in the emerging-markets universe in the third quarter of 2017, including some key events, milestones and data points to offer some perspective.

Three Things We’re Thinking about Today

- Corporate earnings for emerging-market companies have been showing strong and synchronized growth, driving compelling fundamentals for emerging-market equities. For example, several Chinese internet companies have reported earnings that consistently exceeded market forecasts in recent quarters. In Europe, a rebound in commodity prices has led to positive earnings revisions for metal-and energy-related companies in Russia.

- We view China’s automobile market favorably. The rise of China’s upper middle class has continued to drive luxury car demand in the country, as buyers pay more attention to vehicle performance and product quality. Even though China is the largest market globally for cars, vehicle ownership rates in the country remain quite low in comparison with developed markets, indicating potential for further growth.

- India’s economic growth remains strong in a global context, despite a slight deceleration in the second quarter of 2017. Consumer demand has been a key growth driver over the past few quarters and demand arising from the festival season in October could further support growth in the latter part of 2017.

Outlook

We remain optimistic about opportunities among emerging-market equities in the current climate, while remaining mindful of potential risks. Tensions on the Korean peninsula have caused some investors to worry. An outbreak of violence could have global ramifications, with a particular impact on North Asia. However, this threat has been in existence for a long time, and most investors familiar with the region have become accustomed to it.

For our part, we continue to proceed with our value-oriented investment process, taking into consideration market sentiment. We believe it is important for investors to be globally diversified through portfolios that include exposure not just to South Korea or Asia but also to other parts of the world.

Overall, we believe the investment case for emerging markets continues to center around demographics, a rising middle class and domestic consumption. The most striking development recently, though, is the dramatic transformation of many emerging-market companies that used to depend on “old-economy” models (such as commodities or infrastructure) moving into more innovative, value-added products and services.

The technology space is especially interesting to us in this regard, with several emerging-market companies becoming leading players in the development of world-class technology.

Regional Outlook

As at 30 September 2017

Emerging Markets Key Trends and Developments

Emerging-market equities significantly outperformed their developed-market counterparts in the third quarter of 2017, with the MSCI Emerging Markets Index surging 8.0% compared with a 5.0% gain in the MSCI World Index, both in US dollars.1 This outperformance came despite a slight pullback in September, the first month of decline for emerging-market equities in 2017.

For the quarter as a whole, some of the main drivers of emerging-market performance included generally encouraging economic data from China, signs of economic recovery and hopes for reform in Brazil, a strong rebound in global commodity prices based on firming demand, and emerging-market currency strength against the weaker US dollar.

The Most Important Moves in Emerging Markets This Quarter

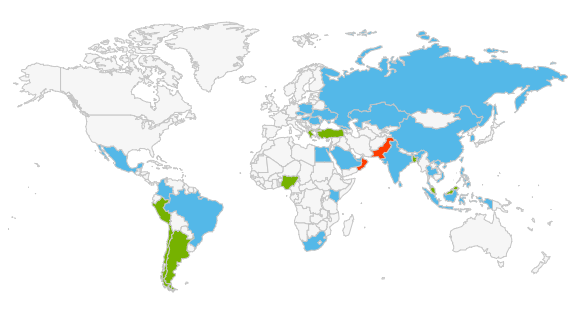

Amid a general rally in global equities and a return of investor confidence, the largest emerging markets—Brazil, Russia and China—were among the top performers in the third quarter.

Brazil posted a substantial double-digit gain, fueled by easing monetary policy, appreciation in the real against the US dollar, hopes for continued reform and higher commodity prices. In Latin America, Chile and Peru were also notable performers, on encouraging political developments, progress in second-quarter economic growth, and, for Chile, stronger copper prices.

A solid earnings season buoyed Russia, along with a rally in oil prices and appreciation in the ruble. In Europe, Hungary and Poland also gained ground. However, Greece was an outlier, recording a double-digit decline, especially toward the end of the quarter on worries about asset quality in its banking sector.

A robust earnings season also drove China’s market. Additional factors included inflows from foreign investors and solid second-quarter economic growth, the latter supported by strength in industrial production, retail sales and fixed-asset investment.

In Asia, Thailand’s market saw a double-digit gain on the back of stronger-than-expected economic growth driven by exports and tourism. In contrast, Pakistan was among the worst performers in emerging markets overall, impacted by a sharp mid-quarter decline due to political turmoil.

Markets in Africa gained moderately in the third quarter. Although South Africa rose, it underperformed its global peers as it continued to be impacted by weakness in the rand, political uncertainty and investor outflows.

Frontier-market stocks also moved higher over the quarter, performing largely in line with their emerging-market counterparts.2 However, performance across individual markets was much more widely dispersed. Markets such as Kuwait, Kenya and Argentina recorded significant gains. Meanwhile, Nigeria lost ground, affected by the naira’s sharp devaluation in August. Sri Lanka and Ukraine were also among markets that declined.

Mark Mobius’ comments, opinions and analyses are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. Because market and economic conditions are subject to rapid change, comments, opinions and analyses are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy.

Important Legal Information

All investments involve risks, including the possible loss of principal. Investments in foreign securities involve special risks including currency fluctuations, economic instability and political developments. Investments in emerging markets, of which frontier markets are a subset, involve heightened risks related to the same factors, in addition to those associated with these markets’ smaller size, lesser liquidity and lack of established legal, political, business and social frameworks to support securities markets. Because these frameworks are typically even less developed in frontier markets, as well as various factors including the increased potential for extreme price volatility, illiquidity, trade barriers and exchange controls, the risks associated with emerging markets are magnified in frontier markets. Stock prices fluctuate, sometimes rapidly and dramatically, due to factors affecting individual companies, particular industries or sectors, or general market conditions.

______________________________________________________________

1. Based on the MSCI Emerging Markets Index versus the MSCI World Index, US dollar terms. The MSCI Emerging Markets Index captures large- and mid-cap representation across 24 emerging-market countries. The MSCI World Index captures large- and mid-cap performance across 23 developed markets. Indexes are unmanaged and one cannot directly invest in them. Past performance is not an indicator or guarantee of future performance.

2. Based on the MSCI Frontier Markets Index, which captures large- and mid-cap representation across 30 frontier markets countries. Indexes are unmanaged and one cannot directly invest in them. Past performance is not an indicator or guarantee of future performance.

© Franklin Templeton Investments

© Franklin Templeton Investments

Read more commentaries by Franklin Templeton Investments