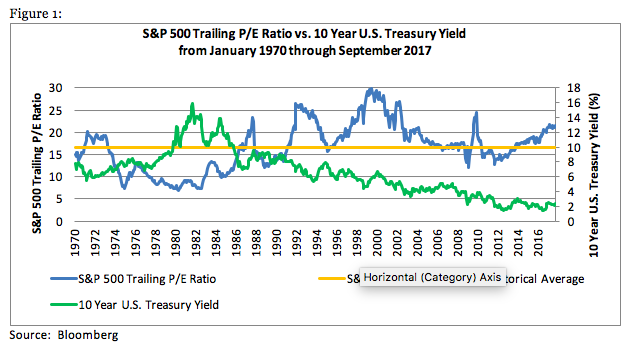

During the third quarter, the economy continued its slow, low inflationary expansion and the equity market continued to gain ground. Real Gross Domestic Product (GDP) expanded by an estimated 2.5%, and inflation hovered around 2.0%. Corporate earnings grew by an estimated 2.8% and the S&P 500 Index (S&P 500) tacked on another 4.5%. At this point eight years into an economic expansion and bull market, we think there are four critical questions that investors ought to be asking:

- Can the economic expansion continue?

- Can inflation remain quiescent?

- Will the Federal Reserve (the Fed) be measured in tightening monetary policy?

- Are equity valuations too high?

In a nutshell, we believe that the slow growth, low inflation trajectory will continue a while longer and, as a result, the Fed can maintain a very measured pace unwinding its unprecedented monetary ease. Typically, economic expansions do not die of old age but rather begin to suffer from excesses and an inflationary build up that then cause the Fed to slam on the monetary brakes. At the moment, we do not see evidence of excesses nor do we see the kind of inflationary acceleration that would alarm the Fed.

We should note, however, that the U.S. economic expansion has been joined by expansions around the world. Such synchronized global economic growth has the potential to cause commodity prices to surge and thereby tilt the inflationary curve upwards. Add to this the possibility that Janet Yellen could be replaced with a more hawkish Fed chairperson who would advocate for a more rapid and forceful Fed tightening. In other words, if we are wrong about a continued low inflation, moderate interest rate environment, it would likely be because inflation ramps higher and the Fed responds with more aggressive tightening.

As we wrote in last quarter’s Investment Outlook, the combination of globalization and the digital revolution has created structural shifts in the economy that have significantly dampened inflation. Globalization allows companies to source labor where it is cheapest and the digital revolution enables companies to drive down costs. To recapitulate what we detailed last quarter, the digital revolution has led to significant re-ordering of the economy.

First, the internet has given consumers an unprecedented ability to compare prices, thereby limiting retailers’ abilities to charge higher prices. Second, the digital revolution has enabled businesses to streamline their processes, thereby driving down costs. This affects not only manufacturing and services but also the extraction and production of commodities such as oil and gas from shale formations and even the production of power from wind and solar. For example, by 2020 wind and solar are estimated to be the lowest cost sources of energy without subsidies. Third, the digital revolution has undermined labor’s ability to demand higher wages. Workers in the “gig” economy are often part-time and rarely unionized. Workers in more traditional industrial roles can be replaced with robots and others with artificial intelligence.

All this is not to say that inflation can never heat up – because, of course, it will at some point – but that there are new structural impediments that are working to postpone higher inflation. At some point, tight labor markets will lead to wage gains. Short-term supply/demand imbalances can still cause commodity prices to fluctuate. The weather will affect food production and hence prices. At the moment, though, inflationary pressures remain tame. Should this change, we will change our tune.