Pinocchio: Am I a real boy?

The Blue Fairy: No, Pinocchio. To make Geppetto's wish come true will be entirely up to you.

Pinocchio: Up to me?

The Blue Fairy: Prove yourself brave, truthful and unselfish, and someday you *will* be a real boy.

Investors are struggling to achieve long-term return targets in today’s low yield environment. To close the gap, many investors feel forced into concentrated equity portfolios.

There is a much better way.

The fathers of modern finance, like Harry Markowitz and Bill Sharpe, showed that investors can achieve their return objectives with much more resilient portfolios. By maximizing diversification, and scaling exposure to the portfolio along the Capital Market Line, investors can achieve even aggressive return targets with much less risk of deep, sustained losses.

This is more than just a great theory. ReSolve puts the techniques to work every day for real investors in our funds, and at the ReSolve Online Advisor in our Adaptive Asset Allocation and Global Risk Parity mandates. In fact, the Global Risk Parity is a superb example of this approach in action.

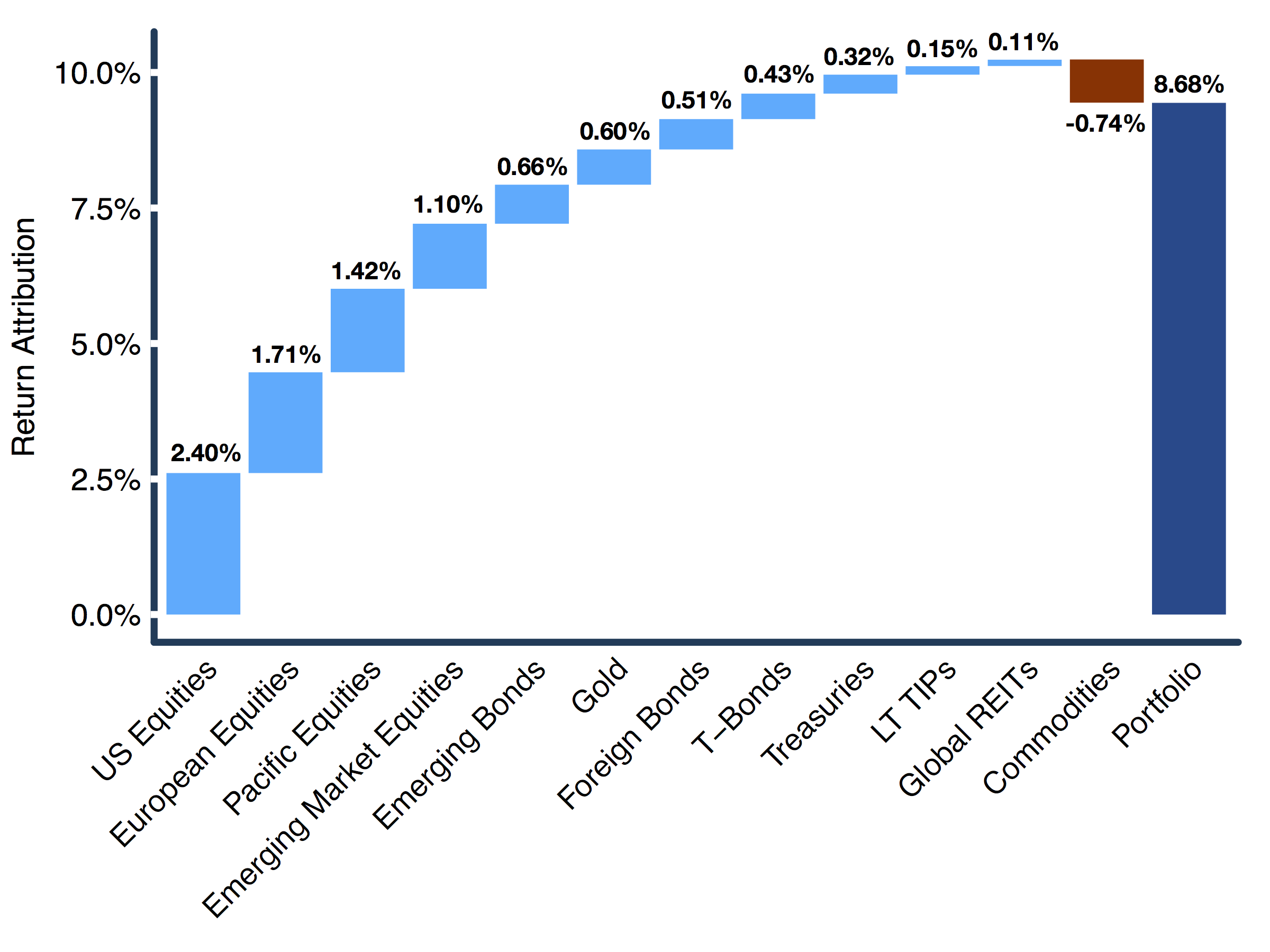

The ReSolve Global Risk Parity strategy is designed to create the most diversified portfolio possible from the world’s major asset classes, including regional equity and government bond markets, and diversified commodities. Figure 1 shows the assets held in the portfolio from January 1st through August 31 2017, and the total return that each asset has contributed to the portfolio. Note that the index held 13 different assets in the portfolio over this period, which collectively produced 8.68% cumulative growth.

Figure 1. Return attribution for ReSolve Global Risk Parity Index (USD), January 1 – August 30 2017

Source: The performance data above represents the performance composite of all ReSolve Global Risk Parity: 6% Volatility (USD) mandates managed by ReSolve Asset Management Inc. Indicated returns of one year or more are annualized. Past performance is not indicative of future performance.

This portfolio accrued most of its returns from holding a diversified basket of global equities. However, by also holding bonds and commodities, the portfolio is more diversified, which means it was positioned to benefit from a wider variety of outcomes, including ones that would not have been favourable for equities. It also had lower volatility than a pure equity portfolio.

Admittedly, this diversified portfolio did not achieve the same returns as a pure global equity portfolio, which gained 15.46%. But investors in the pure equity portfolio also accepted the risks of this portfolio. These risks include a maximum peak-to-trough loss of over 50% in the last decade, and a peak-to-trough loss of over 80% in the Great Depression.

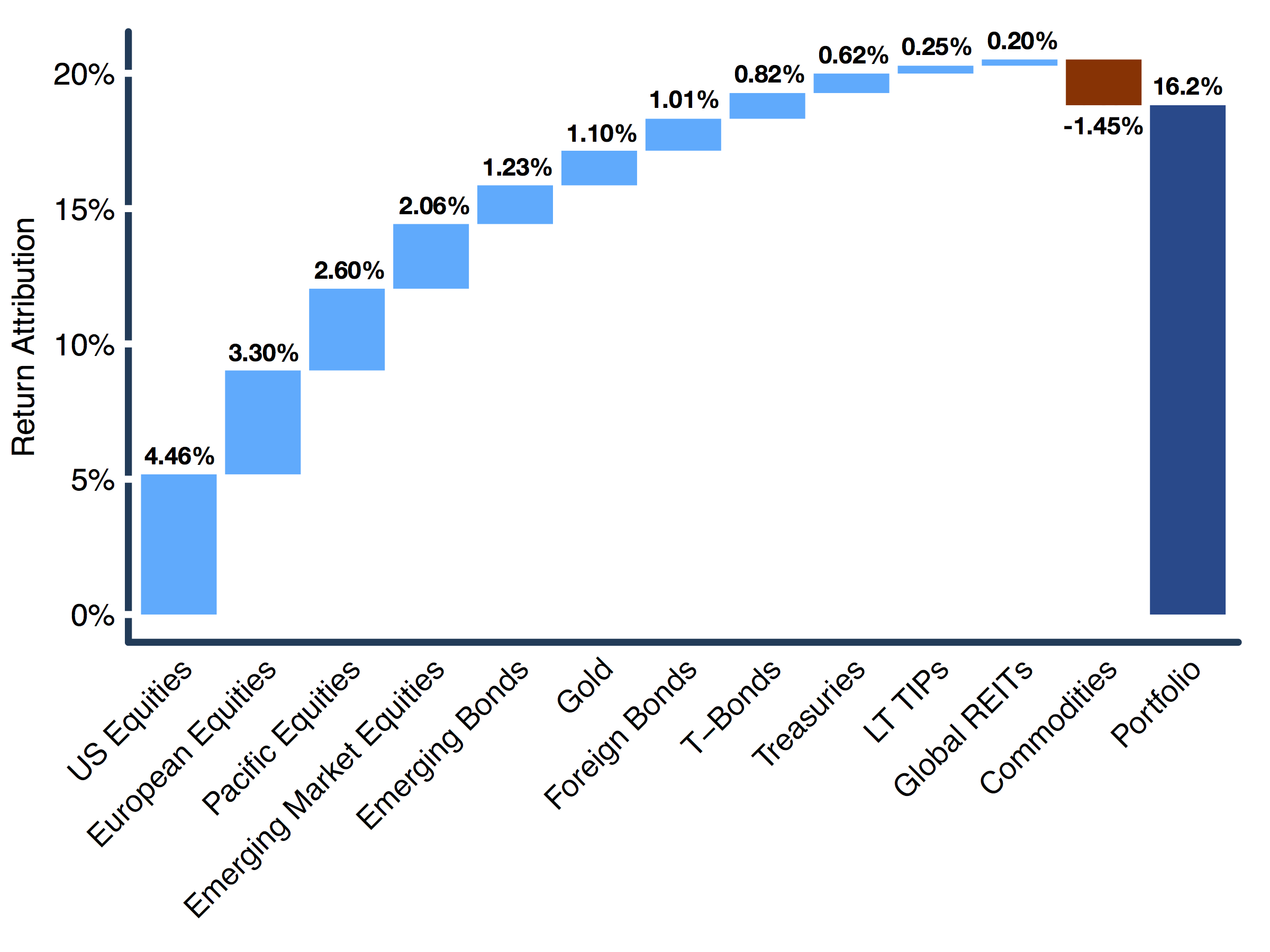

Incredibly, it is possible for investors in highly diversified portfolios to achieve even better returns than investors in concentrated equity portfolios by using the very techniques espoused by the fathers of modern finance. Consider that investors in the ReSolve Global Risk Parity 12% Volatility strategy have earned over 16% year-to-date, with the same diversified portfolio constituents.

Figure 10. Return attribution for ReSolve Global Risk Parity 12% Volatility Index (USD), January 1 – August 30 2017

Source: The performance data above represents the performance composite of all ReSolve Global Risk Parity: 12% Volatility (USD) mandates managed by ReSolve Asset Management Inc. Indicated returns of one year or more are annualized. Past performance is not indicative of future performance.

These same techniques have produced even higher returns for some of ReSolve’s more aggressive and active Adaptive Asset Allocation mandates.

Everything Old is New Again

Investors can be forgiven for believing that the charts above amount to a modern form of financial alchemy. And they would be partly right. But the formulations for this alchemy were documented over 50 years ago, by financial luminaries with some of the most recognizable names in finance to this day.

The real mystery is – why aren’t more investors thinking about the problem this way? Why aren’t you?

Don’t worry, we put together a highly accessible whitepaper that explains exactly how you can achieve the results above using time-tested techniques championed by the greatest minds in finance, and used for decades by some of the world’s most successful hedge funds. In particular, you’ll learn:

- The difference between portfolios formed along the Efficient Frontier and the Capital Market Line

- How portfolios formed along the Capital Market Line are designed to meet return objectives with substantially less risk

- Real-life practical examples of this methodology that you can use right now to improve investment outcomes in the short and long-term.