ReSolve Asset Management

From All-Weather to All-Terrain Investing for the Stormy Decade Ahead

This article explores how the addition of specific liquid alternative strategies produces an “All-Terrain” portfolio with the potential for improved long-term performance across a wider range of market environments.

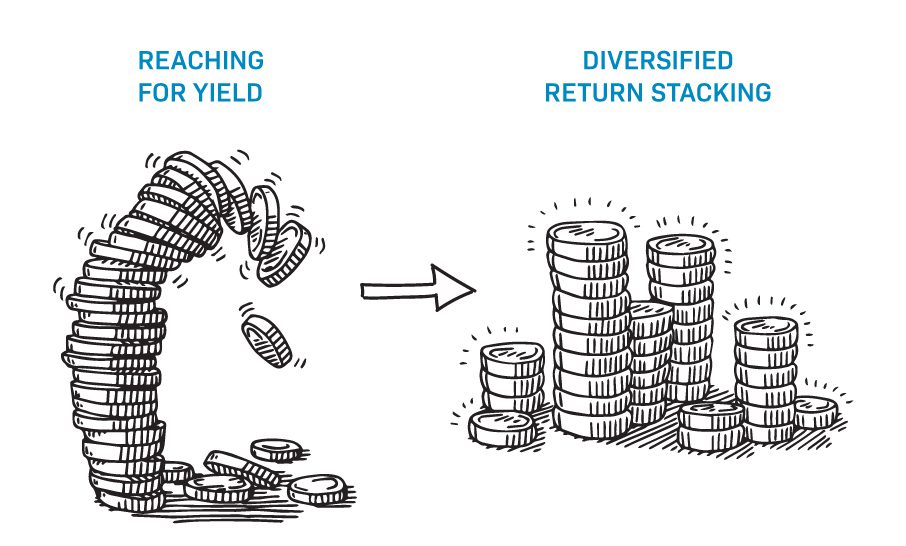

Return Stacking: Strategies for Overcoming A Low Return Environment

Reducing exposure to equities and bonds to accommodate non-correlated assets or alternative strategies may reduce risk, but at the expense of lower potential returns and painful tracking error. We introduce a novel investment concept, accessible to all investors, which is designed to seek higher returns with less risk and low tracking error by using new products which, in combination, can provide more than $1 of exposure for every dollar invested. The proposed solution harnesses the full potential of traditional portfolios plus the opportunity for higher returns and risk reduction from non-correlated investments. We show how to maximize “Return Stacking™” opportunities by choosing alternative fund managers already engaging in capital-efficient strategies.

Bond Pains and Commodities Gain

Global risk assets rose in the wake of positive developments on the two main fronts that have dominated headlines over the past 12 months – pandemic and stimulus.

Risk Parity in the Time of COVID

Consistent with misapprehensions expressed during other recent market crises, there has been a chorus of alarmist speculation about the actions and state of risk-parity strategies during the current crash. We felt it would be helpful to revisit the concept of risk parity and take a snapshot of how a typical global risk parity strategy might have been expected to behave this year.

The Importance of Asset Allocation vs Security Selection

Virtually nobody disputes that Asset Allocation has the greatest impact on portfolio performance and yet most Advisor-designed portfolios are dominated by active funds trying to “win” through security selection.

If you want to construct resilient portfolios that can thrive under most market conditions (including periods like the 2008 Global Financial Crisis), it’s time to consider global adaptive asset allocation. We’ve prepared this exclusive whitepaper to explain why. Don’t miss it!

2017 Year-End Review

It’s tempting, and quite natural, to want to attribute strong performance in any given year to superhuman work ethic, insight, or talent. The fact is, our superb results this year reflect less on the value of our strategies, and more on the role of luck on short-term investment results. What made 2017 a perfect positive storm for certain multi-asset strategies? And what features make certain multi-asset strategies more likely to prosper in the years ahead? All this and a lot more insights in ReSolve’s 2017 Annual Review

Skis and Bikes: The Untold Story of Diversification

In most parts of Canada we have very distinct seasons. Some months of the year are temperate and relatively dry, while other months are cold and snowy. As a result, most Canadian towns of any size have stores that sell skis and bikes.

Skis And Bikes: The Untold Story Of Diversification

“The “free lunch” of diversification is that it allows investors to keep more of their money invested in high return assets while lowering the overall risk of the portfolio. Learn how to build explosion resistant, bulletproof portfolios to weather the markets’ most hostile environments. We guarantee you’ve never learned about diversification like this before.

Yes, You Can Eat Sharpe Ratios

Investors are much more likely to achieve their target returns, regardless of investment environment, by investing in diversified portfolios with scaled exposure along the Capital Market Line. We showcase a live case study and describe steps investors can take to achieve very attractive results.

Yes - You Can Eat Sharpe Ratio

Investors are struggling to achieve long-term return targets in today’s low yield environment. To close the gap, many investors feel forced into concentrated equity portfolios.

Dynamic Asset Allocation for Practitioners, Part 3: Risk-Adjusted Momentum

In this article, we examine whether it pays to account for differences in the path assets take to produce their momentum. All other things equal, do investors express a short-term preference for assets that have produced their returns with less risk, where risk is measured broadly as having delivered a smoother ride?

Dynamic Asset Allocation for Practitioners, Part 2: Multi-Asset Momentum

In our last post, we covered the importance of a well-designed investment universe as a precondition for thoughtful diversification. In this second article on Dynamic Asset Allocation for Practitioners, we will explore several methods for measuring price momentum to compare and contrast their utility under different portfolio concentration and asset universe specifications.

Dynamic Asset Allocation for Practitioners Part 1: Universe Selection

In 2012 we published a whitepaper entitled “Adaptive Asset Allocation: A Primer” in which we built upon the simple, robust momentum framework proposed by Mebane Faber in his 2009 study “Relative Strength Strategies for Investing.”

Bank of America Trashes Risk Parity Funds, Launches One a Month Later

In August 2016, Bank of America Merrill Lynch (BAML) wrote a research note characterizing risk parity as one of the central causes of equity market losses in late 2015. The note had all the hallmarks of a compelling plot line, replete with weapons of mass destruction, billion-dollar bets, and evil villains.

Reminder: Valuations are Useless for Market Timing

Adam Butler introduces a simple but novel innovation for modeling equity market valuations. There are reasons to believe average valuations should rise through time in response to changes in market structure. We discuss the conditions that might lead to higher valuations through time, and present a model to account for it.