When Brent crude was around USD 50 per barrel, we explained why we expected the price of oil to grind slowly higher. In our view, solid global demand, renewed supply constraints and still-significant underinvestment made a clear case for investing in the energy sector.

With oil now edging toward USD 60 per barrel, some investors are taking a fresh look at a sector that we have been constructive on for some time. Yet the consensus view on oil is still bearish – a stance that we believe is not supported by the facts.

Multiple factors are constraining the oil supply

Global demand remains resilient at 97 million barrels a day, but oil fields are being steadily depleted. Oil producers collectively need to add about 7-8 million barrels a day in new production to keep up with demand growth and production declines, but that is difficult to do with prices so low. Increased production requires increased investment – and many firms simply lack the capital to expend after the 2014-2015 collapse in prices. Even though the price of oil has nearly doubled since January 2016, producers still have little scope to invest to grow production or are loathe to do so given price volatility. Short-term survival is winning out over long-term investments.

There is also a geopolitical angle to the argument for higher oil prices. In May, members of the Organization of the Petroleum Exporting Countries (OPEC) agreed to extend production cuts as a way to boost prices. Yet falling tax revenues are forcing some petro-states to drain the sovereign wealth buffers they built up during the good times. This makes their institutions more vulnerable, which raises the risk of social upheaval. Turmoil in areas such as Libya, Venezuela, Algeria and the Iraqi region of Kurdistan could easily stoke fears of supply constraints – and push up prices.

US shale gas looks better than shale oil

Given that almost none of the large oil-producing nations are happy with the current price of oil, and that OPEC itself has traditionally had the power to rebalance markets, one question arises: What is throwing the traditional supply/demand relationship off kilter?

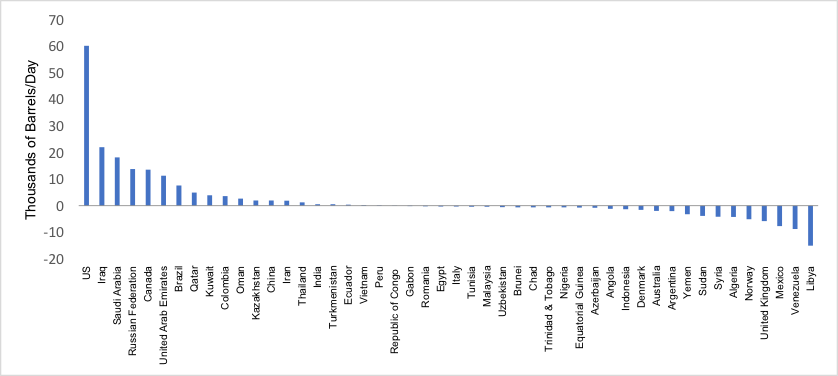

The answer is the US shale industry, which has transformed the world order for energy in just five years. By using new technologies to unlock vast reserves of shale oil and gas, US firms caused oil prices to halve, US consumer energy spending to hit multi-decade lows and OPEC to lose much of its market cartel power.

We believe the veritable bonanza in natural gas that the US shale industry created will have profound consequences for many gas projects globally, with the US cementing its status as a low-cost producer sitting atop huge reserves. In our view, the supply growth of US natural gas, driven by shale gas, is not only prolific, but sustainable.

But the boom in US shale oil, which currently represents about 60 per cent of all oil-supply growth since 2008, looks less sustainable to us. We challenge the market consensus that this shale-oil growth will be maintained or even accelerated at lower and lower production costs. US shale oil is higher up the cost curve on a full cycle-adjusted basis than the market assumes.

Can US Shale Continue Its Sky-High Growth?

Country-by-country share of world oil production growth, 2016 vs 2008

Source: BP Statistical Review of World Energy. Data as at 23 June 2017.

For the shale-oil industry to grow, it must overcome a steep initial decline curve by constantly drilling more wells. However, new wells are being added at an increasingly slower pace as oil-service resources tighten and profitability issues re-emerge. The cost of drilling itself is going up by 10-20 per cent this year, according to some estimates – more evidence that US shale operators need higher prices just to stay operating.

Yet the US shale industry is by and large a cash-flow-negative one, reliant on funding from banks and investors to provide enough cash to stay in business. Indeed, US energy companies have issued approximately USD 100 billion in high-yield bonds in an attempt to raise the capital they need for investment. The problem is that this also raises the spectre of another boom-and-bust event for the industry, particularly in a rising-interest-rate environment.

For their part, US shale producers are seizing opportunities to hedge when prices go up, securing some of their operating cash flows and partially safeguarding future production. Without higher prices and the chance to hedge, many US shale companies will find it increasingly challenging to stay in business. For the first time, we are also beginning to see increasing evidence of US energy and production (E&P) companies becoming more disciplined with their capital, with many pledging to invest at levels at or below their cash flows. This should bolster E&P returns and reduce future growth in oil supply.

Investment implications

We believe that excessive optimism over the prospects for US shale oil has contributed to unnecessarily low valuations for many global energy companies. Without this dream of US energy independence in the market, we believe energy names would be more highly valued. This, in turn, would enable the energy sector to offer stronger returns to investors – and it would enable energy companies to make much-needed investments in their businesses to address the prospect of oil-price spikes on supply shortages.

Subscribe to Get Neil’s Insights Via Email

Neil Dwane’s insights are available as a monthly email subscription for financial professionals only. Your email address must be in our records for your subscription to take effect.

Follow Us on Twitter

For more investment insights and market perspectives from our global research network, follow @AllianzGI_US on Twitter or visit us.allianzgi.com.

Important Information

The material contains the current opinions of the author, which are subject to change without notice. Statements concerning financial market trends are based on current market conditions, which will fluctuate. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities. Forecasts and estimates have certain inherent limitations, and are not intended to be relied upon as advice or interpreted as a recommendation.

Past performance of the markets is no guarantee of future results. This is not an offer or solicitation for the purchase or sale of any financial instrument. It is presented only to provide information on investment strategies and opportunities.

Allianz Global Investors Distributors LLC, 1633 Broadway, New York NY, 10019-7585, us.allianzgi.com, 1 800 926 4456.

291331