ECONOMY

GDP growth slowed in the fourth quarter to 1.9% down from 3.5% in the third quarter. Both numbers were skewed by trade data. Third quarter GDP was lifted by .7% from the export of soybeans to South America, while imports shaved -1.7% from fourth quarter GDP. Since GDP attempts to measure gross domestic production, the Bureau of Economic Analysis (BEA) subtracts imports since they were produced outside of the U.S. While the BEA’s methodology is understandable, it can be misleading. While imports are not produced in the U.S., they are a reflection of U.S. demand. Final demand, which excludes trade, grew by 2.5% in the fourth quarter compared to 2.1% in the third quarter. Business investment rose 2.4% versus 2.1% in the third quarter. This is an encouraging sign since business investment has consistently lagged during this recovery. For the year, GDP grew 1.6%, the slowest since 2011 and down from 2.6% in 2015. The good news is the economy was stronger in the second half of the year and in better shape than the fourth quarter GDP suggested.

Although 2016 finished on a firmer note, it is still reasonable to expect the economy to slow in the first quarter. Year over year income growth was 2.5% at the end of 2016. While up from the 2.3% increase in 2015, the gain was modest, and not likely to cover the higher expenses most consumers will be paying in coming months. Health care costs continue to rise faster than income growth, which was clear to everyone paying higher insurance premiums for the first quarter of 2017. Energy costs have risen significantly since the first quarter of 2016 and this winter has been moderately colder than last winter. Heating homes, apartments, and driving cars is consuming more of consumer’s income in the first quarter of 2017. Mortgage rates are up, housing activity has slowed, and adjustable rate mortgage rates are taking a bigger bite out of paychecks. Since the election consumer confidence has jumped and consumers spent 4% more celebrating Christmas. This is probably why final demand was stronger in the fourth quarter, but consumers will likely start paying down credit card balances in the first quarter.

While the prospect of lower taxes for consumers and corporations has cheered equity investors, tax rates have not been lowered yet, so consumers don’t have more net pay to spend. Even if the tax cuts are made retroactive to January 1, 2017, which is very likely, consumer spending will be constrained in 2 the first quarter by all the issues just discussed. Corporations are likely to spend a little less in coming months, until the details for the depreciation of equipment investments and corporate tax rates are clarified. Companies that may be affected by the potential border adjustment tax are likely to be cautious and spend less. This could include a large range of companies that incorporate a portion of their supply chain outside the U.S. for even a small part of the final product sold in the U.S. Changes in the value of the Dollar impact the domestic economy about 9 months after a significant change. Between May and the end of 2016, the Dollar rose by more than 12%, so the drag will begin to hit by the end of the first quarter and carry through the third quarter. The recent 3% decline in the Dollar won’t become a positive until the fourth quarter.

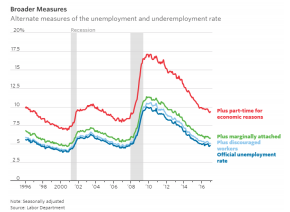

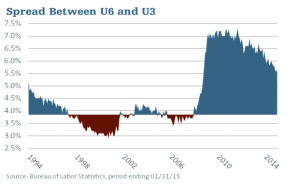

As the official unemployment rate fell from 6.6% in January 2014 to 5.9% in September 2014, the Federal Reserve and many economists forecast that wage growth would begin to pick up as the labor market tightened. In March 2015 I analyzed the spread between the U3 official unemployment rate (dark blue line) and the U6 unemployment rate (red line). The U6 rate includes all unemployed workers reflected by the U3 rate, but also includes people working part time but would prefer full-time employment. In January 2017 the official unemployment rate was 4.8% and the U6 rate was 9.4%. The U6-U3 spread was 4.6% (9.4 – 4.8). Based on the current spread, modest wage gains will continue in coming months, but won’t really pick up steam until the U6-U3 spread drops below 3.85%. The following discussion explains why annual wage increases above 3.3% aren’t likely until the spread narrows more from its current level.

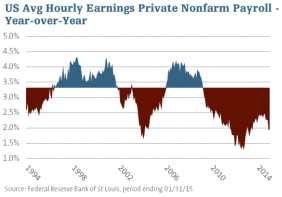

In March 2015 I wondered if wages were affected by changes in the U6-U3 spread. The Labor Department’s U6 data begins in January 1994. To exclude the impact of the financial crisis on the U3 and U6 rate, I used the data from January 1994 through August 2008 to calculate the average spread between the U6-U3 rates. The average spread for this period was 3.85%. I used data from the Federal Reserve Bank of St. Louis to calculate the average increase in wages. Between January 1994 and August 2008, the average annual increase in wages was 3.32%.

When I compared changes in the U6-U3 rate spread to changes in average earnings, I found that wage growth consistently grew faster than 3.32 when the U6-U3 rate spread was below 3.85%. A spread below 3.85% indicated that the labor market was indeed tight which boosted wage growth. Conversely, when the U6-U3 rate spread was above 3.85% wage growth grew less than 3.22%. After the financial crisis in 2008, the U6- U3 rate spread soared to over 7.0% and average wage growth fell below 1.5%. Between 2010 and the end of 2015, average wage growth failed to increase from 2.2%, even as the official unemployment rate fell.

In 2014, the Fed and many economists misread the decline in the U3 unemployment rate as an indication that the labor market was tightening enough to support higher wage growth. As you can see (Chart on pg.2), the U6-U3 rate spread remained well above the 3.85% spread, which explains why wage growth was so tepid. From January 2015 and January 2016, the U6-U3 rate spread narrowed from 5.6% to 4.6%. Although the spreading was still above 3.85%, it had narrowed enough to begin to exert some upward pressure on wages. During 2016, wage growth did improve modestly and I expect a further improvement in 2017. If the U6-U3 spread continues to narrow in coming months from January 2017’s level of 4.6%, wage growth could accelerate.

Trump and GDP Growth

One of Trump’s campaign promises was that his economic program would result in annual GDP growth of 4% and maybe 5%. While it’s possible the economy could produce a single quarter of 4% GDP growth in 2018, the odds of sustained 4% growth before 2020 are virtually nil. The two primary drivers of GDP growth over time are population growth and the level of productivity. The correlation between GDP growth and population growth is straight forward. If a country’s population grows by 2.0%, demand for goods and services should over time enable GDP to grow 2%. As a country’s labor force becomes more productive, the economy grows faster. For instance, productivity would increase by 2%, if the number of widgets produced by the same number of workers increased from 100 per hour to 102 per hour. The increase in widgets would thus add to GDP growth. If U.S. GDP growth is going to exceed 4%, it will be because population growth plus the increase in productivity totals more than 4%. How likely is that in the next four years?

In the years after World War II, 2.5 babies were born for every 1,000 women in the U.S. After the baby boom ended in 1964, the birth rate plunged and was down to 16 per 1000 women by the late 1970’s. After a bounce up to 16.7 in 1990, the downtrend resumed. At the end of 2014, the birth rate was down to 12.5 per 1000 women and was unchanged from that rate in 2015. In 2016, the birth rate fell to 7 per 1000 women, so the trend lower has continued, and 2016 was the lowest birth rate since 1937! The population growth rate can be supplemented by immigration. However, given the Trump administration’s view on immigration, it seems unlikely that immigration will meaningfully add to U.S. population growth in coming years.

The five year average of productivity growth jumped from 1.2% in 1997 to 3.5% in 2004. It has since trended lower and in 2016 was holding near .7%. Based on population growth of 1.25% (12.5 per 1000 women) and .7% productivity growth, GDP trend growth would be expected to be near 2%. Armed with this information it isn’t surprising that GDP growth during the eight years President Obama was in office averaged 1.8%. Since the recession ended in June 2009, GDP growth averaged 2.1%. 4 Unless a baby boom takes hold and an unforeseen surge in productivity materializes, GDP growth won’t be growing 4% anytime soon.

Labor Market Productivity

An increase in business investment can increase productivity, but it may not help the labor market as much as in the past, if there aren’t enough trained workers to utilize new technologies. One solution to improve productivity and reduce the number of workers in the U6 category of underemployment would be to increase job training programs for those with a high school education or less. The unemployment rate for those with less than a high school rate was 7.5% in January 2017, three times the level for those with a college degree. Getting a college degree is not the answer it once was. College costs have soared in the last decade, which is why there is now more than $1.3 trillion in student debt. Too many kids are graduating with degrees there is no demand for in the economy, so they are forced to take jobs that are outside their degree. For recent college graduates ages 22-27, almost 45% were underemployed as of March 2016, as were 34.4% of all college graduates (ages 22-65). Workers with a high school diploma had an unemployment rate of 5.3% in January, but I suspect workers with just a high school education are probably working more than one part time job to make ends meet and would prefer a full time job. This helps explain why 39.5% of 18 – 34-year-olds are still living with their parents. This is the second highest percent since 1900, and only behind the high in 1940 after the Depression.

According to Accenture, doubling the pace of strategic retraining efforts would reduce the share of jobs vulnerable to automation. Accenture says it is up to corporate leaders to help workers hone their skills for jobs that rely on human capabilities such as social and emotional intelligence. According to a recent survey by The Wall Street Journal and Vistage International, more than 60% of small businesses are spending more time training workers than they were a year ago. This proactive training is in a response to a rising tide of applicants lacking the required skills. According to a survey by the National Federation of Independent Businesses, the share of small businesses with few or no qualified applicants for job openings was 44% in November a 17-year high. According to a new report from the McKinsey Global Institute, robots will replace just 5% of all occupations through automation by 2055, less than what many expect. McKinsey predicts automation could increase global productivity by .8% to 1.4% annually during the next 40 years.

President Trump has rarely mentioned the role technology has played in eliminating many middle class jobs over the last 15 years. Instead, he has focused on unfair trade deals as being the culprit for the jobs lost. Globalization has certainly played a significant role, but so has technology and technology will continue to do so in coming decades. The sooner the government and corporate America make retraining ‘job one’, the sooner more workers will be prepared to adapt as technology evolves. Our country has control over allocating resources for training. The same cannot be said for renegotiating trade deals with countries that will resist changes that will hurt their own workers.

Commercial Real Estate

The Federal Reserve’s January 2017 Senior Loan Officer Opinion Survey was released on February 7 and it contained valuable information about commercial real estate. Since the first quarter of 2016, banks have significantly tightened their lending standards for multi-family apartment buildings. In the fourth quarter of 2015 only 7.4% of banks had increased lending standards. Since mid-2016, more than 30% of large banks tightened standards every quarter, which means standards have been progressively raised.

Since the end of 2015, demand for multi-family loans has declined from an increase of 20.6% to 7.2% of banks reporting a decline in demand. The increase in lending standards by banks has likely been in response to an increase in the vacancy rate for apartments and falling rate of increase in rent growth. Upward pressure on the vacancy rate and downward pressure on rents is likely to increase in 2017. According to Axiometrics Inc., 378,000 new apartments are expected to be completed across the country this year, which is 35% more than the 20 year average.

Commercial real estate volume fell by $58.3 billion in 2016, according to data firm Real Capital Analytics. The 11% decline was the first annual decrease since 2009. According to Reis Inc., 30 metropolitan areas experienced an increase in vacancy in 2016 versus 2015, as more retail stores closed. Total returns from commercial real estate rose 9.2% in the twelve months through September 30, 2016. The total return as of September 30, 2015 was 13.5%, so last year’s falloff was large and the lowest total return in six years. The Green Street U.S. Commercial Property Index has been flat since mid-2016, after rising 107% from its March 2009 low. I don’t think it is a coincidence that the Green Street Index stalled just as banks got serious about tightening lending standards.

The fundamental outlook for commercial real estate is likely to deteriorate in coming quarters, and technical analysis of an ETF that is concentrated in real estate looks less than positive. The iShares Real Estate ETF (IYR) seeks to track the investment results of the Dow Jones U.S. Real Estate Index. The fund generally invests at least 90% of its assets in securities of the underlying index and in depositary receipts representing securities of the underlying index. The underlying fund measures the performance of the real estate sector of the U.S. equity market and may include large-, mid- or small-capitalization companies, and components primarily include real estate investment trusts ("REITs").

The real estate sector topped out in July 2016 just as interest rates were bottoming. From the peak in July and the bottom in early November, the iShares Real Estate ETF (IYR) declined -16.1%, the Cohen & Steers Real Estate ETF (ICF) dropped -17.3%, and Vanguard’s Real Estate ETF (VNQ) lost -17.1%. In terms of price, IYR lost $13.69 from its July peak of $85.80. A 50% retracement from the low of $72.11 would have carried IYR back to $78.95. On January 6, it topped at $78.83, so the rebound may be over. If the economy slows in the first quarter as I expect and Treasury bond interest rates fall a bit, IYR may be able to reach $80.57, which is the 61.8% retracement of the $13.69 decline from the July peak. Based on the chart pattern, I think IYR is likely to decline to below $69.00, which would test the red trend line connecting the low in 2014 and low in 2015. If the next decline is equal to the $13.69 drop between July and early November, IYR could drop to $65.14 - $66.88, which brackets the $65.88 low in February 2016. From current price levels, this would represent a decline of 12% to 16%. Given the weakening fundamentals and negative chart pattern, investors should assess any allocation to the real estate sector.

Trade

During the last 15 years, U.S. consumers have broadly been the beneficiary of globalization, as U.S. companies imported goods that cost less. Lower prices helped stretch the paycheck of middle class workers whose median income peaked in 2000. The downside of globalization was the loss of middle class jobs to countries that had a lower cost of production due to lower wages. President Trump has 7 vowed to bring back jobs as he renegotiates trade pacts so they establish free and fair trade. No one knows the details of the coming changes in trade, but one thing seems certain. U.S. consumers will be paying more for goods produced outside the U.S. Whether it is due to a border adjustment tax or targeted tariffs, the cost of imported goods will be more expensive. I don’t see how this will be good for economic growth, unless wage growth accelerates significantly, which doesn’t seem likely. If this scenario plays out, Trump’s most ardent supporters will be negatively affected as Trump fulfills one of his primary campaign promises. I doubt they will appreciate the irony.

In the January issue of Macro Tides, I discussed Trump’s view of the Dollar and suggested that Trump might not hesitate to talk the Dollar down sometime in 2017. The only surprise is that he didn’t even wait until he was in office to do it. In an interview with the Wall Street Journal published on January 17, he described the Dollar as “too strong.” He also said the U.S. might need to “get the Dollar down” if a change in tax policy pushes it up. “Having a strong Dollar has certain advantages, but it has a lot of disadvantages.”

Trump has called China “The single greatest manipulator that’s ever been on this planet.” As I noted last month, that comment stretches the truth. The Yuan appreciated 25.5% against the Dollar between January 2007 and July 2015, before falling 10% against the Dollar through 2016. Since May 2014, the Yuan has appreciated by 19.4% against the Euro and 35.9% versus the Yen through 2016. If China is a currency manipulator, they haven’t been very good at it. On the other hand, Japan has depreciated the Yen by 33% since September 2012, and the Euro has lost 24% of its value versus the Dollar since May 2014. On January 31, Trump’s trade advisor Peter Navarro accused Germany of using a “grossly undervalued” Euro to exploit the U.S. Later that day, in a meeting with pharmaceutical executives at the White House, Trump went after China and Japan. “Every other country lives on devaluation. They play the devaluation market and we sit here like a bunch of dummies.”

Trump’s comments have had an effect on the Dollar as it has fallen from 103.80 on January 3 to 99.23 two days after Navarro’s and Trump’s comment on January 31. I was expecting the Dollar to drop from 103.80 to 100.00 based on a negative RSI divergence as it ran up to 103.80 and that 90% of traders were bullish the Dollar, suggesting it had become a crowded trade. Despite the drop under 100.00, the door is still open for the Dollar to rally to one more new high above 103.80, before a multi-month decline to below 93.00 takes hold. I have thought the final rally (Wave 5) in the Dollar was more likely to be spurred by weakness in the Euro, rather than a hawkish Fed. There are important elections coming in March (Netherlands) and April (France), which could prove far more disruptive than Brexit. A close below 98.60 would pretty much eliminate the new high potential. It’s possible that the high in January at 103.80 was more important than I originally thought, and that the bull market from the low in the Dollar in March 2008 is over. If that’s the case, the Dollar is likely to rally to 101.50 – 102.20, before it rolls over in earnest. A close below 100.00, after a failing rally to 101.50 -102.20, would likely confirm that January was THE top.

U.S. Stocks

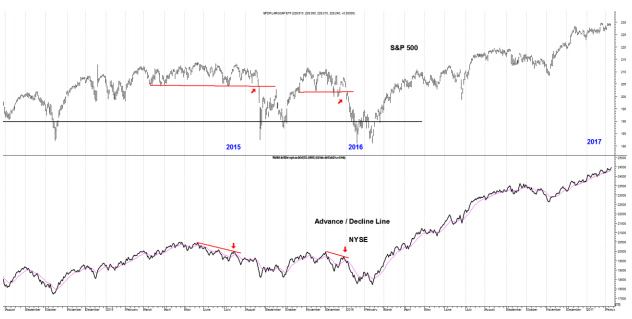

The Advance / Decline line continues to make new highs, which is especially noteworthy since bond yields have risen since the election in November. Look how weak the A/D line was back in the summer of 2015 and late 2015 as noted by the red arrows. This was one of the warning signs I noted in June and July 2015, just before the August 2015 swoon. The same pattern of weakness in the A/D line was repeated in late 2015, just before the sharp decline in early 2016. As you can see, the A/D line is in a strong uptrend. My guess remains that the market is vulnerable to a modest correction by the end of the first quarter. If the S&P drops 3% or so from the high at 2310, a decline to 2235 is likely at a minimum. The current strength in the A/D line suggests the S&P is likely to rally to higher high before Labor Day. A correction greater than 7% is not likely until the A/D line lags and records a lower high, as it did in the summer of 2015 and December 2015.

Jim Welsh

@JimWelshMacro

Read more commentaries by Macro Tides