Macro Factors and their impact on Monetary Policy, the Economy, and Financial Markets

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsThe Business Cycle Is Not Dead

It seems that after years of expecting inflation to rise to its 2.0% target the Federal Reserve and many economists have concluded it’s just not possible. The reasons most often cited are the Amazon Affect, Artificial Intelligence, weak wage growth, years of excess capacity, and transitory factors like the mobile phone price war in March 2017. In September Federal Reserve Chair Janet Yellen said that the inability of inflation to rise to the Fed’s 2.0% target was “a mystery” and that the Fed clearly did not understand why. This is an extraordinary public admission by a Federal Reserve Chair but echoes the sentiments of private economists who have also been mystified by the lack of inflation after the unemployment rate fell to 5.0% in September 2015. It also explains why the Federal Reserve increased its 2018 estimates for economic growth, lowered the estimate for the unemployment rate, but left its forecast for PCE inflation and Core PCE inflation unchanged for 2018 and 2019.

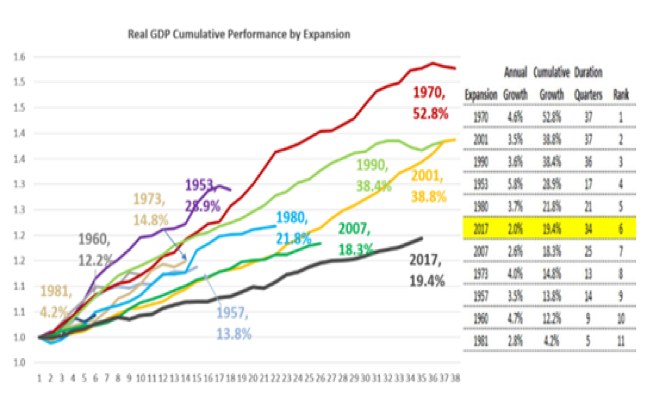

One factor that certainly played a role in keeping inflation tame longer than expected according to the Phillips curve was the plodding nature of the recovery since it began in June 2009. Of the eleven economic expansions since 1949, the current recovery is the weakest, as measured by annual GDP growth during each expansion averaging just 2.0%. If GDP growth persists through the end of 2018, which seems very likely, this recovery will be the longest on record at 38 months. A number of the expansions since 1949 that registered much stronger annual GDP growth were also far shorter in terms of time. This occurred because much stronger growth contributed to a more pronounced business cycle leading to higher inflation and a response by the Federal Reserve that included higher interest rates and tighter monetary policy. In the shorter but stronger recoveries since 1949 the Fed stepped on the brakes too hard which led to the demise of the expansion and recession.

The 37 month expansion that ended in 1970 was preceded by an increase in the federal funds rate from 5.80% in November 1968 to 9.20% in August 1969. The Federal Reserve was responding to a late business cycle jump in CPI inflation from 2.5% in April 1967 to 4.7% in December 1968. The 37 month expansion that ended in 2001 was accompanied by a pick-up in inflation from 2.0% in June 1999 to 3.7% in June 2000 which led the Fed to increase the federal funds rate from 4.75% in June 1999 to 6.50% in June 2000. The 1970 recession was precipitated by an aggressive tightening by the Federal Reserve (a 58.6% increase in the fed funds rate (9.2 minus 5.8 / 5.8), while the 8 month shallow recession in 2001 was preceded by a far less aggressive change in monetary policy (36.8% = 6.5 minus 4.75 / 4.75) but was exacerbated by the unwinding of the dot.com tech bubble.

The lesson from economic history is whether an expansion was strong or long lasting eventually the business cycle matured to a point that ignited a rise in inflation that was sufficient to evoke an increase in interest rates and a tightening in monetary policy that led to a recession and a bear market in stocks. After years of slow growth since 2009 there is a risk that many economists have dismissed the concept of the business cycle and its role in creating inflation. The fiscal stimulus from the Tax Reform Act will make the economy more cyclical in terms of the business cycle than at any time during this recovery. Inflation has the potential of surprising the Federal Reserve and many economists in coming months since they have thrown in the towel in expecting inflation’s return.

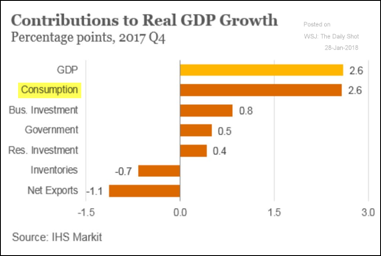

In its first estimate of fourth quarter GDP, the Bureau of Economic Analysis (BEA) reported that the economy grew by 2.6% down from 3.2% in the third quarter. Many economists had forecast an increase above 3.0% or higher. The Atlanta Fed’s GDPNow forecast had forecast growth of 3.4%, while the New York Fed had estimated Q4 growth at 3.9%. On the surface this report was a disappointment, especially for President Trump who would have loved to send out a Tweet trumpeting a third quarter of GDP growth above 3.0%. As often happens, this report had a lot of noise which weighed GDP down and overshadowed the underlying strength in the economy. After adding 0.79% in the third quarter, inventories were pared in the fourth quarter which lowered GDP by 0.67%. The rundown of inventories lowered fourth quarter GDP, but in the first half of 2018 inventories will be rebuilt and add to GDP. In calculating Domestic GDP, the BEA subtracts imports since those goods and services were produced outside the U.S. In the second quarter, the monthly trade deficit averaged $47,238 billion. It then fell 5.18% to $44,786 billion which added 0.36% to third quarter GDP. Based on the available data for October and November, the trade deficit jumped 11.0% in the fourth quarter so the BEA subtracted 1.13% from fourth quarter GDP. Stronger demand for goods and services is a sign of strength irrespective of where they were produced.If changes in inventory and trade were removed, GDP grew 2.05% in the third quarter and 4.4% in the fourth quarter.

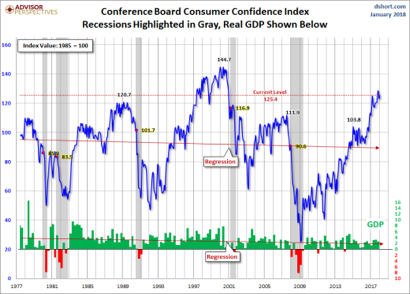

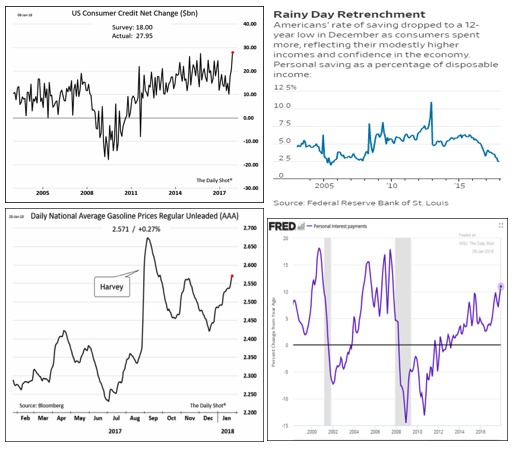

The strength in the fourth quarter was due to several factors. Hurricanes Harvey in late August and Irma in September caused an estimated $175 billion of damage. The recovery and rebuilding after these natural disasters certainly added to growth in the fourth quarter and will contribute to growth in the first half of 2018. Consumer Confidence has held near the highest levels in the past 40 years since the election, no doubt helped by the prospect of more take home pay. (Chart compliments of Doug Short, Advisor Perspectives) This has led consumers to spend and borrow more and save less. In November consumers charged up almost $28 billion which was the most in more than 15 years. I suspect the data for December will also show a healthy increase in credit card spending since holiday spending was the strongest in years. Although interest expense as a percent of disposable income is below the peaks set in 2006 and 2000, it has been climbing steadily and higher interest rates will lift it further. At the end of 2017 the savings rate fell to 2.4% the lowest since 2006. Since last June the cost for a tank of gas has jumped by more than 15.0%. Since the tax tables will be available in February most workers will begin to see the tax cut reflected in their February paychecks. The majority of consumers are likely to pay down some of their credit card debt, increase their savings, spend more on gasoline, and use what’s left for fun.

In the short run, the economy may not get the boost expected from the tax cut in the first quarter. As discussed in the January issue of Macro Tides, “Whether it’s the weather or the seasonal adjustment process used by the Bureau of Economic Analysis (BEA), first quarter GDP growth has consistently been weaker than in the other quarters. The average GDP growth in the first quarter from 2011 through 2017 was 1.16% compared to 2.60% in Q2, 2.46% in Q3, and 2.23% in Q4.” The weather for much of the country in January was worse than normal. If the cold, snow, sleet, and ice persist through February, many consumers will elect to spend more time indoors than at the mall.

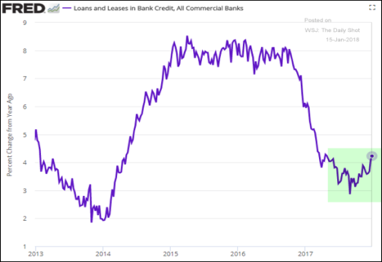

In anticipation of the improved environment for investment, company boards likely discussed in 2017 where they will target the increase in their investments but will need to approve them formally at a board meeting. Some investments will require additional planning before they can be started. This suggests the initial boost to investment will occur more in the second and third quarter than in the first quarter. As I noted in the January commentary, bank lending will provide a valuable barometer of changes in business investment and should begin to rise in the first half of 2018. After falling from an annual growth rate of 8% just before the election to just 1% in the fourth quarter of 2017, it has begun to rise as expected.

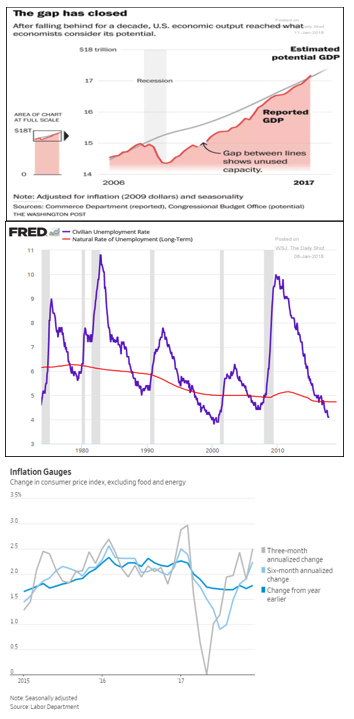

Despite the slow annual GDP growth rate since June 2009, the output gap between the economy’s potential and actual growth has finally been closed. This suggests that the economy is entering the final stage of the business cycle after 9 long years of mediocre growth. As the economy exceeds its growth potential, upward pressure on inflation will increase since excess capacity has been absorbed. As companies invest and increase capacity, the upward pressure on prices will be somewhat alleviated but this process will take time. In the short run, the fiscal stimulus will result in more inflation before the additional capacity is in place. The labor market has also reached a tipping point now that the U6 minus the U3 spread has narrowed sufficiently to result in better wage growth, as discussed in the November 2017 issue of Macro Tides. The Natural Rate of Unemployment has been below its threshold for more than a year which is another indication that labor market slack is disappearing. The pace of wage growth will also be boosted by the wage increases announced by large employers like WalMart (1.5 million workers) which will pressure other employers even outside of retail to raise pay to keep workers from defecting to WalMart and competitors fincreasing pay. An indication that wage growth has begun to accelerate should become more evident when the February employment report is released on March 9.

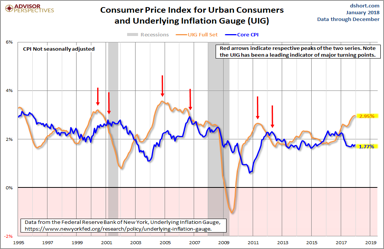

Although the core rate of Consumer Price Inflation (CPI) was unchanged at 1.8% in December, the 3 month and 6 month annualized change was 2.5% and 2.25% respectively. This indicates that pipeline inflation is likely to put upward pressure on core inflation in coming months. The New York Federal Reserve’s Underlying Inflation Gauge (UIG) is comfortably above the core rate of inflation. The UIG has been a good leading indicator of changes in core inflation since 1995 and it suggests core inflation is headed higher in coming months.

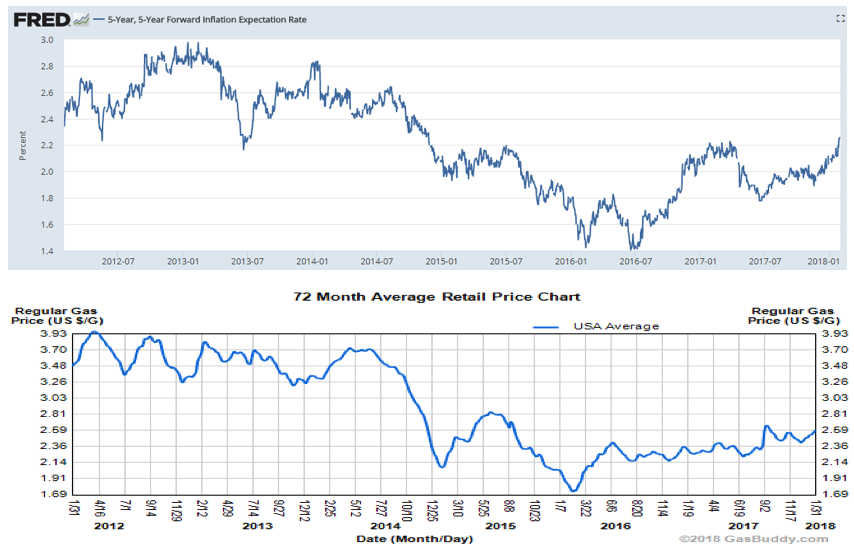

The Federal Reserve watches inflation expectations because they shape how households and companies act and thus can go a long way in determining where inflation actually ends up. Consumers accustomed to meager inflation will resist paying up for goods and services. Companies, in turn, will shun giving higher wages to their workers because they fear they’ll lose sales if they raise prices to cover added labor costs. It’s a vicious circle that has proven difficult for monetary policy makers to break. The correlation between gasoline prices and inflation expectations has been fairly high over time, since most drivers frequently visit a gas station so changes in gas prices are noted. When gasoline prices plunged in the second half of 2014 until early 2016, inflation expectations dropped significantly. As gas prices have recovered so have inflation expectations. There are other factors that also influence inflation expectations, so changes in gas prices are not the sole determinant. Inflation expectations have just exceeded the high recorded in early 2017 and mid 2015, even though gas prices are lower.

If wage growth accelerates in 2018 as I expect, companies will be forced to either absorb higher labor costs or raise prices. It will be worth monitoring how many companies raise prices since inflation expectations will climb as will price inflation in the real world and the Federal Reserve will take note. The chart of inflation expectations is close to signaling a ‘breakout’, if it pushes above the high on March 24, 2017 at 2.23%. On January 29, the 5-year Forward Inflation Expectation Rate closed at 2.26%. A breakout would suggest the Expectation Rate can climb to 2.60% in coming months.

In the 28 years since 1980 there have only been 6 years when all 46 countries followed by the OECD were growing: 1987, 2004, 2005, 2006, 2007, and 2017. Such broad synchronized growth is good for the global economy. After the passage of the Tax Reform Act, the IMF increased its estimate for global GDP growth in 2018 and 2019 by 0.2% and now expects growth of 3.9%. The IMF expects business investment to increase in the U.S. due to the reduction in corporate tax rates, and expects the increase in the budget deficit to provide additional fiscal stimulus. Another consequence of synchronized global growth is synchronized pressure on inflation through higher commodity prices and better wage growth. Historically, commodity prices have experienced significant increases at the end of prior business cycles and this cycle should prove no different.

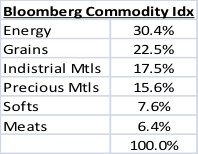

The Bloomberg Commodity Index (BCI) is a diversified blend of commodities as the nearby table illustrates and the symbol for the ETF that tracks the BCI is DJP. The long term chart of DJP shows it is approaching the black down trend line connecting the high in 2011 and 2014, just before oil prices swooned. DJP has broken above the blue trend line connecting the highs in October 2015, February and November 2017 which is positive. Near term the weekly RSI is just below 70 and the daily RSI reached 78.4 on January 24, which indicates that DJP is overbought. After a pullback to $24.50, there is a good chance DJP could break out above the long term black down trend line in coming months, which could be followed by a rally to near $30.00 or the green horizontal trend line near $34.50. A breakout would provide additional confirmation that higher inflation is coming.

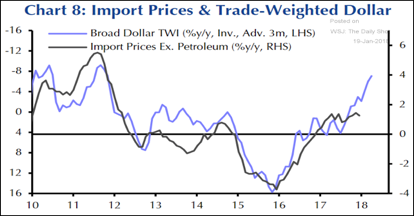

Other than for a brief period in 2014, import prices have subtracted from U.S. inflation and in early 2016 were negative by a whopping -16%. In early 2017 import prices began to rise and will get a big boost in 2018 based on the year-over-year decline in the Trade Weighted Dollar Index as shown by the blue line. The composition of the Trade Weighted Dollar Index is significantly different than the Dollar Index. The Euro only has a weighting of 17.2% compared to 57.6% in the Dollar Index, while the Chinese Yuan carries a weighting of 21.5% versus no representation in the Dollar Index. In 2017 the Trade Weighted Dollar lost 7.1% and has shed another -3.1% in January 2018.

Eurozone

In January the ECB lowered its monthly bond purchases from $60 billion to $30 billion which it plans to continue through September. At the ECB’s October meeting the ECB retained the link between asset purchases and inflation, stating purchases will continue until inflation moves closer toward its 2.0% target. In a November 21 interview ECB board member Benoit Coeure, who is the head of operations at the ECB said, “I expect this link to change when the governing council is sufficiently confident that net asset purchases are less needed for inflation to return towards 2 percent in a sustainable way. We were not ready to make that change in October, but I expect it will come at some point between now and September 2018.” After a speech in Dublin Ireland on January 31, Coeure said “We are not going to be too hasty. We are having a discussion on having a discussion. Any nuances in the Governing Council are as to when next to communicate.”

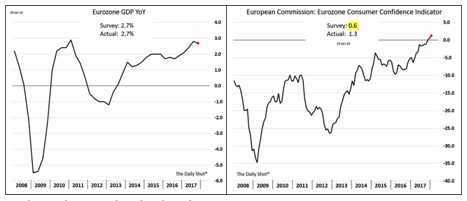

The ‘nuances’ between members of the Governing Council may be wider than Mr. Coeure was willing to acknowledge. On January 28, Klas Knot, who also heads the Dutch Central Bank, said in an interview on the television talk show Buitenhof, “The program has done what could realistically be expected of it. We don’t have to communicate yet that it will be over after September, but I think that’s where we’re headed.” Knot has a point. Economic growth in the Eurozone finished 2017 at 2.7% which is the fastest growth since early 2011 which is comparable to growth in the U.S. Consumer Confidence is the highest since 2000 and the EU’s unemployment rate at 4.3% is just above the U.S.’s rate of 4.1%. The primary difference between monetary policy in the U.S. and the Eurozone is the U.S. policy rate is 1.46% while the ECB’s policy rate is minus -0.40%.

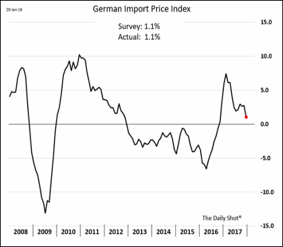

As noted by Mario Draghi after the ECB’s January 25 meeting, the ECB plans to maintain its QE program, “until the Governing Council sees a sustained adjustment in the path of inflation consistent with its inflation aim.” According to a flash estimate from Eurostat on January 31, Euro area annual inflation dipped to 1.3% in January, down from 1.4% in December 2017. Since the end of 2016 the Trade Weighted Dollar has lost -9.98% through the end of January, while the Dollar Index has dropped by 13.04%. Although the decline in the Dollar has been broad based, the difference between the Dollar Index and the Trade Weighted Dollar is in large part due to the 18.0% increase in the value of the Euro against the Dollar. Just as Dollar weakness is feeding import inflation into the U.S., the strength of the Euro is causing import prices to fall in the Eurozone. Since the beginning of 2017, Germany’s import inflation has plunged from 7.3% to 1.1% in December. This is not a welcome development for the ECB as it moves toward normalizing its monetary policy. When ECB policy maker Ewald Nowotny was asked about the Euro’s recent gains on January 17 he said it was ‘not helpful’. A week later Treasury Secretary Mnuchin stated, “Obviously a weaker dollar is good for us as it relates to trade and opportunities," and that the Dollar’s value in the short term is "not a concern of ours at all." Within minutes of Mnuchin’s comments the Euro rose by more than 1.0%. Since then policy makers, including ECB president Draghi, Executive Board member Benoit Coeure and Bank of France Governor Francois Villeroy de Galhau, have politely reminded U.S. officials of a global commitment to refrain from targeting exchange rates to gain a competitive advantage.

As discussed in the September Macro Tides, “When the Fed and ECB wanted to repress interest rates they could enlist the help of market participants to ride their coattails since investors would profit from the collaboration. Unwinding negative real interest rates and curtailing bond purchases will cause interest rates to rise and create losses for bond holders. Rather than being coconspirators, market participants will be combatants with the central banks and more importantly with each other.” As I noted in the December Macro Tides, “This is a significant change which has yet to manifest itself but is likely to emerge in 2018 as the bond vigilantes reclaim a role in the global bond market. If GDP growth is above 2.0% and inflation is closing in on 2.0%, why would anyone want to own a German 10-year Bund yielding less than .50%? This is the existential question bond managers in Europe and globally will ask themselves in the first half of 2018. This will lead them to decide to lower their European bond exposure before the ECB announces it is stopping its QE purchases and the urge/stampede to sell develops. An important clue that this is beginning will be provided when the yield on the 10-year German Bund closes above .50%. My guess is that this is likely to happen before June 30 and could be followed by an increase to .75% or .90% fairly quickly.” The yield on the 10-year German Bund closed above .50% on January 11 and quickly climbed to .763% on February 2.

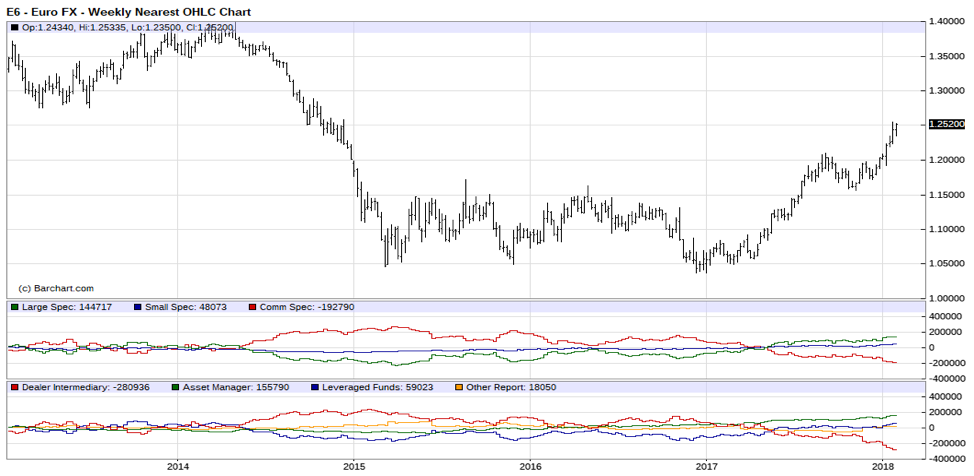

Based on technical analysis the Euro may be approaching an important top in coming weeks. As discussed in the January 29 Weekly Technical Review (WTR), “The Euro topped on May 5, 2014 at 1.3993 and dropped .3652 until bottoming on January 2, 2017 at 1.0341. A 61.8% retracement of that large decline would carry the Euro back up to 1.259. The longer term chart of the Euro suggests it could rally back to the down trend line connecting the highs of April 2008 at 1.6008, May 2011 at 1.4938, and May 2014 at 1.3993. This trend line comes in near 1.2770 and will decline modestly in coming weeks. This suggests that the Euro could make a major high between 1.25 and 1.2770 in the next month or so.” On February 1, the Euro closed at 1.2499. After Mnuchin’s weak dollar comment, the Euro rose to 1.2536 on January 25 before pulling back. The Euro should rally in five waves from the November 6 low of 1.1554. Last week’s high of 1.2536 on January 25 looks like the end wave 3. After a modest pullback, the Euro is likely to rally above last week’s high to complete the rally from November 6 and potentially the entire rally from the January 2017 low of 1.0340.”

When the Euro bottomed on January 2, 2017 sentiment toward the Euro was very negative. That has changed in a big way based on positioning in the futures market. As discussed in the December 18 WTR, positioning in the futures market is probably the best measure of sentiment since it shows how money is positioned. When positioning becomes extreme, with Large Speculators holding a large long or short position, the odds are high that the trend is about to change. Large Speculators are trend followers so by definition as a group they hold their largest long position as an uptrend is nearing a high and the largest short position after a large decline that is close to a bottom. The unwinding of large long positions held by Large Speculators contributes to a decline as they sell, and pushes prices higher as they buy to cover a large short position.

In March 2014 when the Euro was trading just below 1.40 and nearing a very important top, Large Specs held 39,634 contracts long. Conversely, when the Euro was bottoming in March 2015 just above 1.05, Large Specs were holding -220,963 contracts short in anticipation of lower prices (green line middle panel chart below). By August 2015 the Euro had rallied to just below 1.14. As the Euro was bottoming below 1.040 in December 2016, Large Specs were holding -114,556 contracts short. Rather than falling more, the Euro zoomed to 1.20 by August 2017. As of January 22, Large Speculators are long 144,717 contracts, which is their largest long position ever.

Commercials (red line middle panel chart above) typically take the opposite side of the trade that the Large Speculators hold. When Large Specs hold a large long position, the Commercials hold a large short position. As just described, Large Speculators are often wrong at intermediate turning points, which is why the Commercials are considered the ‘smart money’.

The green line in the middle panel illustrates the positioning of the Large Specs and how they were way too short at the important lows in March 2015 and December 2016. And now they are holding their largest long position ever. As you can see by the red line in the middle panel, the Commercials were long at the lows in the Euro in March 2015 and December 2016, after which the Euro rallied smartly. The Commercials now hold their largest short position ever (-192,790).

The combination of technical analysis and sentiment as measured by positioning in the futures market suggests a sizable decline in the Euro is coming, and will probably start in the first half of 2018. This is counter intuitive since the ECB is likely to first announce it is delinking its commitment to its 2.0% inflation target and its QE program, and early in the third quarter announce that it is lowering or eliminating it monthly bond purchases after September 30. Most traders (and ECB members) would expect those changes to cause the Euro to rise further, which is one reason the ECB is in no hurry to make any announcement. However, markets often don’t reward logic. Since January 3, 2017 the Dollar Index has declined by 13% even though the Federal Reserve has increased the federal funds rate by 75 basis points and is expected to raise it by another .25% at its March meeting.

Dollar

Since the Euro comprises 57.6% of the Dollar index, a sizable decline in the Euro will contribute to a meaningful rally in the Dollar. In 2017, the Dollar fell sharply and equity markets around the globe did well, especially emerging markets. A big rally in the Dollar could certainly upset the apple cart and lead to an unexpected correction in global equity markets. Sentiment is quite negative the Dollar especially after Mnuchin’s comments. Technically, the Dollar still needs more time and will probably make a lower low in coming weeks as the Euro is making its high. Prior to the Dollar’s rally in September and October 2017, the Dollar made an initial low in August, bounced, and then recorded a lower low in early September. At the August low, the Dollar’s RSI was 21.3. However, when the Dollar posted a lower low in early September, the RSI was 29.2. This positive divergence suggested that the Dollar was setting up for a rally. I expect something similar will unfold in coming weeks which would provide technical evidence that the down trend was nearing an end. As discussed in January, the repatriation of overseas profits could provide the Dollar a lift starting in the second quarter and beyond.

Oil

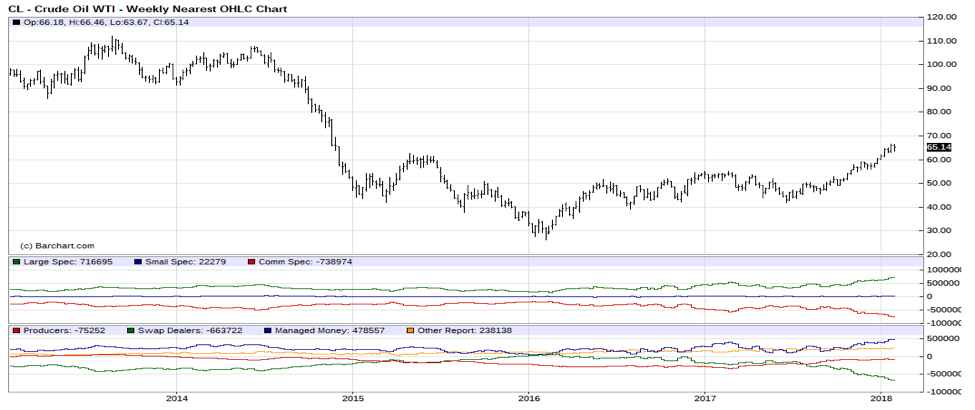

One of the markets that might be adversely affected by a stronger Dollar is oil. Obviously, global GDP growth and the increase of oil production from U.S. shale producers are more important. However, oil sports a similar technical and sentiment set up as the Euro, which is the primary reason oil could be vulnerable to a meaningful correction. From its low of $26.05 a barrel in February 2016, oil rallied $25.62 to an initial high in June 2016 of $51.67. Oil then spent the following 12 months chopping sideways before recording a trading low of $42.05 in June 2017. An equal rally of $25.62 suggests oil could rally to $67.67. On January 25 oil traded as high as $66.66 so it is possible that the rally from last June has topped. The main message from technical analysis is that the rally in oil is close to at least an intermediate high that could lead to correction down to $55.00 or lower by mid-year.

Based on the positioning in the futures, market sentiment is wildly bullish. Large Speculators (trend followers, hedge funds) have their largest long position in history (+716,695 contracts) as noted by the green line in the middle panel. When oil was trading at $108.00 a barrel in June 2014, Large Specs were long 458,969 contracts. When oil fell to $26.05 in February 2016, Large Specs had sold 271,092 contracts and were long only 187,877 contracts. Large Specs selling certainly contributed to the decline in oil prices, which is why positioning can provide important clues near tops and bottoms.

In June 2014 the Commercials were short -492,580 contracts in anticipation of lower oil prices. They were right. At the low in February 2016 Commercials had trimmed their short position by 291,694 contracts. As of January 22, Commercials were holding their largest short position of -738,974 contracts in history. The smart money is clearly positioned for a decline in oil prices.

Interest Rates

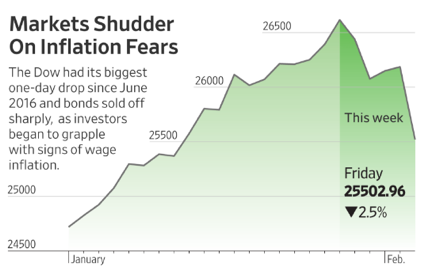

For several months I have discussed my expectation that bond yields were going to rise and that the 10-year Treasury yield would breakout above the high from March 2017 at 2.63%. On January 24, I posted the following note on LinkedIn. “After years of slow growth many have forgotten that the fiscal stimulus being added will make the economy more cyclical in terms of the business cycle than at any time during this recovery. If correct, the bond market is poised for a 'recognition' point when investors realize that inflation is actually moving higher. If this develops it could lead to an overreaction. The movie will be called 'Taper Tantrum II. Since September I have expected the yield on the 10-year Treasury bond to breakout above 2.63%. That is unfolding and could lead to run up to 3.0% in coming months. I suspect that the stock market might not appreciate the competition higher yields pose.” Since January 24 the yield on the 10-year Treasury bond has soared from 2.65% to 2.85% on February 2, and the stock market took notice. On Friday, February 2 the DJIA shed a devilish 666 points and the S&P 500 lost -2.1%.

The 10-year Treasury yield finished 2013 at 3.03%, while the 30-year Treasury yield topped at 3.20% in March 2017. The question is whether bond yields will run right through these significant technical levels or will the race higher in yields take a pause. For a number reasons my guess is that yields are near a short term high and are likely to come down in coming weeks. The bond market is quite oversold and pension funds, insurance companies, and retail bond investors will do some buying as yields on the 10-year and 30-year Treasury approach those yield thresholds. There is also a good chance that a Federal Reserve president will give a speech that mollifies bond investors by emphasizing that the Fed will be willing to allow inflation to run above 2.0% for a period. The Fed’s expectation is that fiscal stimulus will give the economy and inflation a boost before fading by the end of 2019. After years of inflation holding below its 2.0% target, the Fed will tolerate a brief period above 2.0% and continue to be patient as it normalizes interest rates in coming months. If this speech is given, the bond market will be comforted and reassured that the Fed will not overreact. Trade negotiations could bring bond yields down as discussed below.

Longer term the technical chart patterns for the 10-year and 30-year Treasury yields suggest they may eventually rise to 3.30% and 3.75% as discussed in the December Macro Tides. “From the bottom in July 2016, the 10-year Treasury yield rose from 1.336% to 2.62% or an increase of 1.28% for wave A. The decline from 2.62% in March 2017 to 2.034% in September 2017 represents wave B. If wave C is equal to wave A and rises 1.28% from the September low of 2.034%, the 10-year Treasury yield could reach 3.30%. The yield pattern in the 30-Treasury bond suggests the following: From the bottom in July 2016, the 30-year Treasury yield rose from 2.10% to 3.20% in March 2017 or an increase of 1.210% for wave A. The decline from the high at 3.20% to 2.034% in September 2017 represents wave B. If wave C is equal to wave A and rises 1.10% from the September low of 2.65%, the 30-year Treasury yield could reach 3.75%.”

Trade Negotiations

Trade negotiations on NAFTA and with China are going to intensify in coming months. If talks on NAFTA breakdown or become more bellicose with China, Treasury yields would fall as would the stock market. It seems likely there will be some bumps along the way even if negotiations produce an agreement. Candidate and President Trump has repeatedly called NAFTA "the worst trade deal ever made". On January 25 Commerce Secretary Wilbur Ross said, “Trade war has been in place for quite a little while, the difference is the U.S. troops are now coming to the ramparts.” Some of this rhetoric is posturing and an attempt to game negotiations. In a January 8 speech to the American Farm Bureau Federation’s annual convention in Nashville, Trump told the audience, “On NAFTA, I’m working very hard to get a better deal for our country and for our farmers and for our manufacturers. It’s not the easiest negotiation, but we’re going to make it fair for you people again. We want to see even more victories for the American farmer and the American rancher.” According to government figures, in 2016 the U.S. sent $16.4 billion in agricultural and food products to Mexico and $23.4 billion to Canada. Farmers worry that without NAFTA Canada and Mexico would have the right to put tariffs on products from the U.S. and could turn to other countries for supplies of soybeans, corn and other farm products.

In Trump’s speech at Davos Switzerland on January 26, Trump also said his “America first” policy did not mean “America alone” and that there had never been a better time to do business with the US. In the same speech Trump took a not so indirect swipe at China. “The United States will no longer turn a blind eye to unfair economic practices, including massive intellectual property theft, industrial subsidies and pervasive state-led economic planning.” Few would disagree with the goal of fair trade. As always during negotiations, the devil is in the details.

Gold and Gold Stocks

In the January Macro Tides I explained why I thought Gold and Gold stocks could rally in early January, which was discussed in the December 18 Weekly Technical Review when Gold was $1261. “The positioning in the futures suggests Gold is likely rally to at least $1305 and could make a run at the September high of $1357 in the first quarter of 2018. Based on the improved positioning in the futures market, I increased the position in GDX to 50% on December 18 at $22.17. On December 19, GDX opened at $22.16 and traded down to $22.035, so subscribers had the opportunity to enter GDX below $22.17. Based on the bullish outlook, I also established at 25% position in the Junior Gold stock ETF GDXJ at $32.035.” In the January 22, Weekly Technical Review (WTR) I noted why I was far less bullish on Gold and the Gold stocks. “If Gold does manage to rally above $1344, selling most of the position may be warranted since sentiment has turned overly bullish and the positioning in the futures market has become far less supportive.” After Mnuchin’s comments about the Dollar, Gold spiked above $1344 and traded as high as $1365 on January 25. On Friday February 2, Gold closed at $1331. I also discussed in the January 22 WTR why I had sold my positions in Gold stocks. “When Gold pulled back from $1344 to $1326, the Gold stocks acted poorly as measured by their relative strength to Gold. The high on January 2 was $23.84 which I felt should not be touched again if GDX was going to rally above $25.00. On January 18 my stop at $23.85 was triggered on the remaining portion (50%) of my position. The average sell price was $23.91. The cost basis on the GDX position is $21.73. When Gold pulled back from $1344 to $1326 on January 17, GDXJ traded down to $34.90, which indicated that its relative strength to Gold was weakening. On January 18 my stop at $34.82 was triggered on the remaining portion (50%) of my position. The average sell price was $34.93 and the cost basis on the GDXJ position was $32.035.” On February 2, GDX closed at $22.91 and GDXJ finished at $32.29.

Stocks

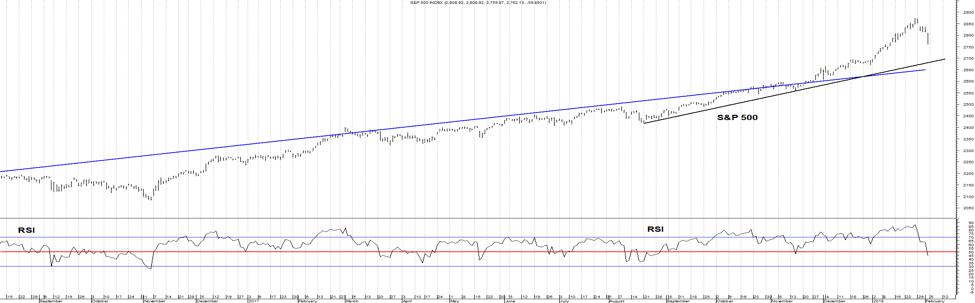

Measures of bullish invest sentiment have recently reached multi-decade highs which is always a warning that the market could be vulnerable to a correction, if provided a good reason. I have thought that higher Treasury yields could provide a reason since lower interest rates have been cited as why the stock market’s valuation was still reasonable. If Treasury yields hold below the cited levels of 3.03% and 3.20% for the 10-year and 30-year Treasury bonds, the bull market in stocks is likely intact. In coming weeks, the S&P 500 has the potential to fall to the black trend line connecting the August and November lows which is near 2700. The blue trend line, which is near 2650, connects the prior highs in the S&P 500 after it bottomed in February 2016. The quality of the next rally will reveal whether the stock market could be vulnerable to a larger correction during the second quarter which is my expectation.

January Employment Report

Once the U.S. Unemployment rate fell below 6.0% in September 2014 economists and the Federal Reserve expected wage growth to accelerate from the paltry level of 2.2% it had been growing since 2010. Expectations for better wage growth increased when the U3 rate fell to 4.9% in January 2016. Needless to say, the forecasts for faster wage growth in 2015, 2016, and 2017 did not materialized as the majority of economists and the Fed expected. I disagreed with their forecasts since the spread between the U6 unemployment rate minus the U3 unemployment rate has been a better predictor of wage growth than either the U3 rate, or the Non-Accelerating Inflation Rate of Unemployment or the natural unemployment rate (NAIRU). In the November 2017 issue of Macro Tides I said, “Wage growth is finally likely to accelerate in coming months.” I based that conclusion on the fact that the U6 minus the U3 unemployment had narrowed to the lowest level in nine years in October and was at the level that has led to higher wage growth since 1994. Here are the headlines from the WSJ on February 3 after the Labor Department reported that in January average hourly earnings were up 2.9% from a year ago. “Wage Growth Feeds Market Unease” “Dow drops 4.1% in week, bonds slide as investors start taking threat of inflation more seriously.” “Long run in jobs growth is finally lifting wages.”

Once the U.S. Unemployment rate fell below 6.0% in September 2014 economists and the Federal Reserve expected wage growth to accelerate from the paltry level of 2.2% it had been growing since 2010. Expectations for better wage growth increased when the U3 rate fell to 4.9% in January 2016. Needless to say, the forecasts for faster wage growth in 2015, 2016, and 2017 did not materialized as the majority of economists and the Fed expected. I disagreed with their forecasts since the spread between the U6 unemployment rate minus the U3 unemployment rate has been a better predictor of wage growth than either the U3 rate, or the Non-Accelerating Inflation Rate of Unemployment or the natural unemployment rate (NAIRU). In the November 2017 issue of Macro Tides I said, “Wage growth is finally likely to accelerate in coming months.” I based that conclusion on the fact that the U6 minus the U3 unemployment had narrowed to the lowest level in nine years in October and was at the level that has led to higher wage growth since 1994. Here are the headlines from the WSJ on February 3 after the Labor Department reported that in January average hourly earnings were up 2.9% from a year ago. “Wage Growth Feeds Market Unease” “Dow drops 4.1% in week, bonds slide as investors start taking threat of inflation more seriously.” “Long run in jobs growth is finally lifting wages.”

Jim Welsh

@JimWelshMacro

© Marcro Tides

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All