The underlying investment story since the stock market’s trough in March 2009 has been investors no longer believe in the business cycle. Each cycle has unique characteristics and catalysts, but history shows well that business cycles still exist and tend to follow a very common pattern.

The current business cycle, contrary to popular belief, has both existed and followed the typical course. The current cycle, however, has been elongated. The economy developed more slowly than investors expected, but the cycle nonetheless had early- and mid- cycle periods. Whereas economists have largely been disappointed by this cycle’s anemic growth, investors have benefitted greatly from its muted, but abnormally long path.

We commented many months ago that the US economy was entering the late-cycle phase. Investors again ignored the business cycle and the signs indicative of a late-cycle period. In particular, investors disregarded the inflation pressures that were building.

Inflation expectations have been rising since mid-2016 (see Chart 1), yet flows into bond funds and ETFs went unchecked.

The recent market volatility seems to be a result of investors finally realizing that the business cycle isn’t dead. Later-cycle inflation is becoming more obvious, and the market has needed to recalibrate valuations, earnings expectations, and asset allocations to the suddenly “new” inflationary environment.

CHART 1:

Inflation Expectations : 5 Yr 5Yr Forward Breakeven

(Weekly, Feb. 13, 2013 – Feb. 7, 2018)

The elongated cycle

In 2010, RBA suggested that the bull market might be one of the longest in modern history, and positioned our portfolios accordingly. We thought the cycle would rejuvenate, but it would be elongated because of the constraining effects of the deflating global credit bubble. Early-cycle sectors tend to be very credit-sensitive (housing, autos, and retailing), but credit conditions remained tighter than normal even as the economy recovered. The combination of unusually tight credit standards, fiscal policies that were contractionary, and increasing financial regulation and oversight limited early-cycle growth. The positive though was that the economic boom often sought by politicians was replaced by slow consistent growth that proved to be investors’ nirvana.

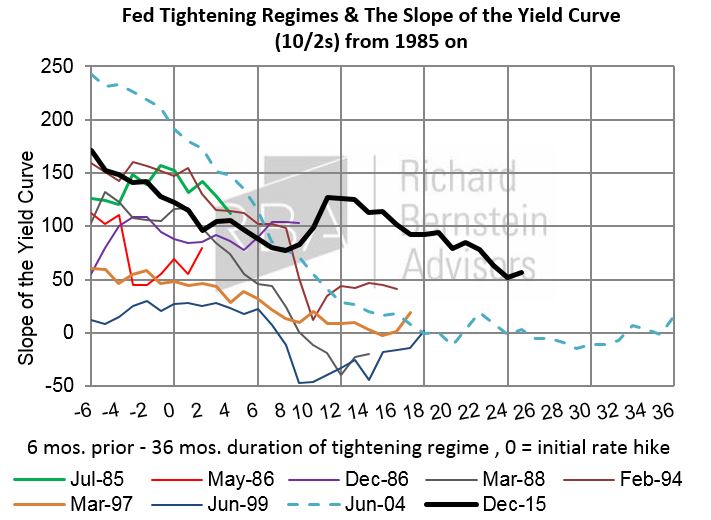

Normal cyclical events have occurred, but they have occurred more slowly and gradually than in a typical cycle. The yield curve is a good example. Chart 2 compares the slope of the yield curve during this cycle to those of past cycles. Note how long it has taken during this cycle for the yield curve to invert (it still hasn’t!). History will remember this cycle as an elongated one.

CHART 2:

Fed Tightening Regimes & The Slope of the Yield Curve

(10/2s) from 1985 on

Late-cycle bottlenecks

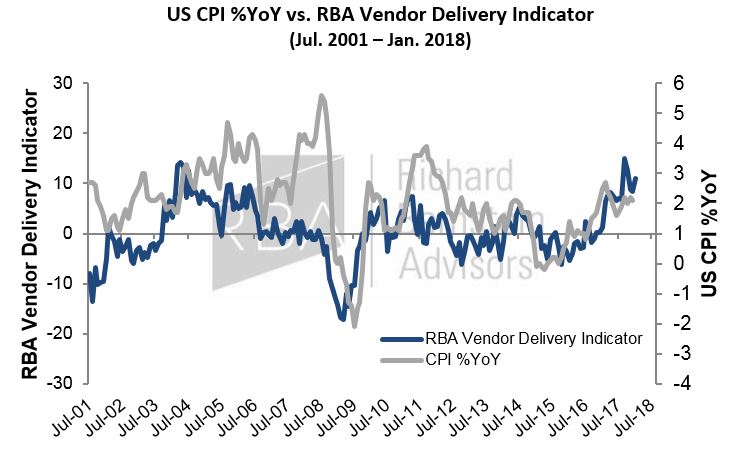

The late-cycle is often characterized by economic growth that outstrips the growth in capital spending and causes production bottlenecks, and that certainly describes the current environment. Vendor delivery time is a simple indicator of potentially increasing inflation, and measures how long it takes for suppliers to fulfill orders. Longer fulfillment times indicate that demand is greater than available supply, and that prices could increase.

Chart 3 is RBA’s indicator of vendor delivery time, which incorporates common delivery statistics. Vendor delivery times have been increasing and normal cyclical bottlenecks are forming. That implies further upward pressure on the CPI.

It’s important to reiterate that bottlenecks are normal in a later-cycle environment. Unfortunately, investors played ostrich with respect to inflation and ignored the standard indicators’ warnings that portfolios positioned for deflation/disinflation might underperform. The increase in market volatility suggests that investors finally caught on.

CHART 3:

US CPI %YoY vs. RBA Vendor Delivery Indicator

(Jul. 2001 – Jan. 2018)

Our portfolios remain flexible

RBA’s “go anywhere” macro strategy affords us great flexibility to adapt our portfolios to many different environments. When inflation expectations began to trough in 2016, we significantly repositioned our portfolios to take advantage of nominal economic growth and profits growth that might be stronger than investors expected. To date, we continue to have inflation as a major theme within our portfolios.

Cyclical sectors make up the bulk of our equity positioning: Technology, Financials, Materials, and Emerging Markets. We remain very short duration within our fixed-income portfolios to help protect against rising long-term interest rates. Currently, our bond holdings have a duration of only about 20-25% of benchmark duration. In addition, we still hold gold and/or gold miners.

Volatility is always unsettling. However, we think our disciplined approach that relies on fundamentals and not events (like volatility spikes) will continue to benefit our investors.

© Copyright 2018 Richard Bernstein Advisors LLC. All rights reserved.

PAST PERFORMANCE IS NO GUARANTEE OF FUTURE RESULTS

Nothing contained herein constitutes tax, legal, insurance or investment advice, or the recommendation of or an offer to sell, or the solicitation of an offer to buy or invest in any investment product, vehicle, service or instrument. Such an offer or solicitation may only be made by delivery to a prospective investor of formal offering materials, including subscription or account documents or forms, which include detailed discussions of the terms of the respective product, vehicle, service or instrument, including the principal

risk factors that might impact such a purchase or investment, and which should be reviewed carefully by any such investor before making the decision to invest. Links to appearances and articles by Richard Bernstein, whether in the press, on television or otherwise, are provided for informational purposes only and in no

way should be considered a recommendation of any particular investment product, vehicle, service or instrument or the rendering of investment advice, which must always be evaluated by a prospective investor in consultation with his or her own financial adviser and in light of his or her own circumstances, including the investor’s investment horizon, appetite for risk, and ability to withstand a potential loss of some or all of an investment’s value. Investing is subject to market risks. Investors acknowledge and accept the potential loss of some or all of an investment’s value. Past performance is, of course, no guarantee of future results. Views represented are subject to change at the sole discretion of Richard Bernstein Advisors LLC. Richard Bernstein Advisors LLC does not undertake to advise you of any changes in the views expressed herein.

© Richard Bernstein Advisors

Read more commentaries by Richard Bernstein Advisors