There is a headline-grabbing kerfuffle regarding new US tariffs on imported steel and aluminum, which come on top of tariffs previously placed on solar panels and washing machines.

At RBA, our policy of remaining “annoyingly dispassionate” during a fire-charged political environment leads us to focus on an investment issue that virtually no one is discussing.

Investors have flocked for years to income-oriented strategies in both the bond and equity markets, yet those strategies are the ones most at risk from US tariffs. Tariffs, by definition, are always inflationary, and inflation is the enemy of income.

Tariffs are, by definition, ALWAYS inflationary

Investors need to remember that tariffs, by definition, are always inflationary. When a country is accused of dumping its goods that means the country is gaining market share by selling goods at unreasonably and unprofitably low prices. The tariff is meant to equate the dumping country’s prices with those of domestic producers in order to stem or reverse the ill begotten gain in market share. Tariffs are by definition inflationary because prices increase from an alleged artificially low price to a more normal and less competitive price. The price increase might be warranted or not, but the reality is that prices always increase as a result of a tariff.

Another way to understand why prices always increase when tariffs are imposed is based on simple economics of supply and demand. Tariffs restrict the supply of goods. If one assumes that demand does not fall, then “Economics 101” highlights that coupling reduced supply and consistent demand results in higher prices. Reducing competition rarely results in lower prices.

Of course, there is a chance that higher prices actually reduce demand, and defeat the tariff’s ultimate goal of increasing demand for domestic producers. Domestic companies might gain market share, but the overall market could shrink in response to higher prices as other products substitute for the tariffed products. This is not theoretical. A major auto company has already stated that they may simply accelerate their use of carbon fiber if tariffs significantly distort steel and aluminum prices.

Inflation hurts income strategies

Inflation expectations troughed in June 2016 (!), and have been gradually rising since then. It seems immaterial from an investment point of view whether this increase in inflation expectations is secular or merely cyclical because investors are largely ill-positioned for any increase in inflation. Chart 1 shows that the 10-year T-note yield troughed roughly 3 weeks after inflation expectations troughed. The sizeable flows into fixed-income investments ran unabated until only recently despite the increase in yields.

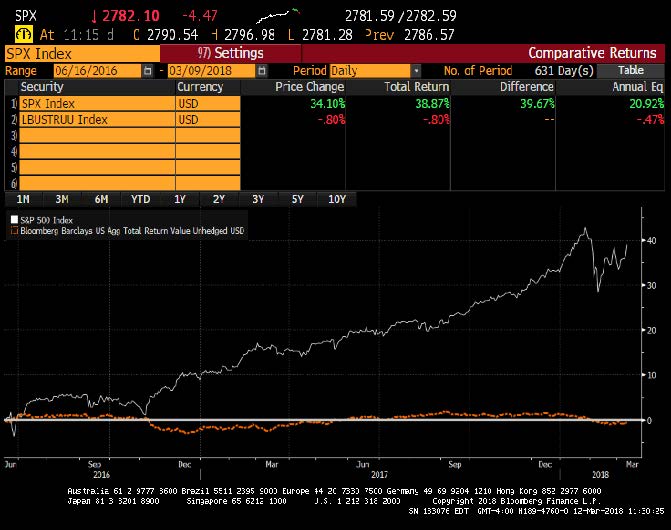

Disinflation and deflation seem to be so ingrained into investors’ psyche that investors refuse to believe that inflation expectations are rising, and they do not seem aware how poorly their income-oriented portfolios are performing. Chart 2 shows the performance of stocks and bonds since inflation expectations troughed on June 16, 2016. Since that date, stocks have outperformed bonds on an annualized basis by more than 20% PER YEAR!

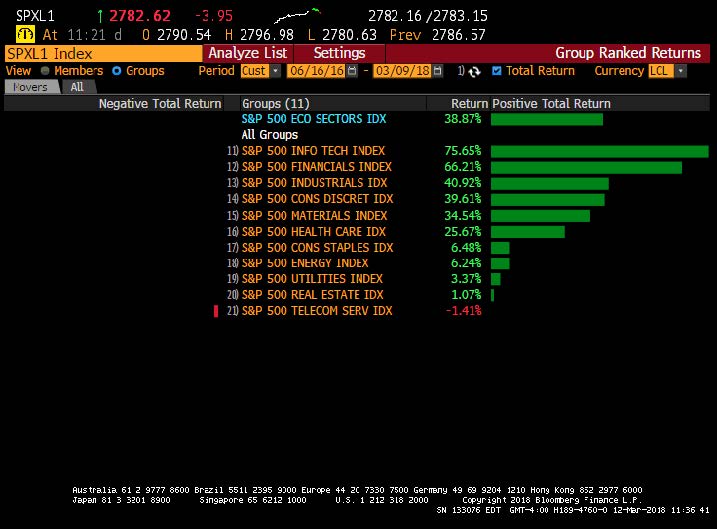

Chart 3 shows the performance of US economic sectors since June 2016. Income-oriented sectors (Real Estate, Telecom, and Utilities) have been the three worst performing sectors since inflation expectations troughed. More important, sectors that generally benefit from rising prices have significantly outperformed. The opportunity cost of investing in fixed-income or in income-oriented stocks instead of pro-inflation investments has been massive.

The backup in interest rates has been fundamentally-based. As is typical in a late-cycle environment, inflation pressures begin to grow and interest rates increase. Instituting tariffs on top of these normal late-cycle developments suggests that income-oriented investors should be much more concerned about inflation than they are currently.

CHART 1:

10-Year T-Note Yield

(Daily Mar. 9, 2008 – Mar. 9, 2018)

Source: Bloomberg Finance L.P.

Source: Bloomberg Finance L.P.

CHART 2:

Stocks vs. Bonds since June 16, 2016

Source: Bloomberg Finance L.P. For Index descriptors, see "Index Descriptions" at end of document.

CHART 3:

S&P 500® Sector Performance since June 16, 2016

Source: Bloomberg Finance L.P. For Index descriptors, see "Index Descriptions" at end of document.

Putting fuel on normal late-cycle pricing power

The global economy has significantly changed during the past nine years. As there would be during any economic cycle, there have been early-, mid-, and late-cycle periods. It is RBA’s contention that the US is currently entering a very traditional late-cycle period, and late-cycle periods are often characterized by production bottlenecks and rising inflation. That fundamental backdrop is well underway.

Tariffs could be the fuel on the pricing power fire. There are already production bottlenecks forming within the economy, and pricing power is returning to corporate America. Tariffs are likely to cause prices to increase more than they might normally.

Most investors’ portfolios are not allocated for even a small increase in inflation. The performance of popular fixed-income and equity income strategies has been miserable since inflation expectations troughed in June 2016. Most important, though, is that the underperformance of these popular strategies has come before tariffs were introduced. It would be extraordinarily unique to see these strategies outperform when confronted with even more inflation prone regulation and policies.

The risks in the financial markets are not from inflation. Rather, the risk is that most investors are very poorly positioned for the changing inflation environment, which now includes tariffs.

INDEX DESCRIPTIONS:

The following descriptions, while believed to be accurate, are in some cases abbreviated versions of more detailed or comprehensive definitions available from the sponsors or originators of the respective indices. Anyone interested in such further details is free to consult each such sponsor’s or originator’s website.

The past performance of an index is not a guarantee of future results.

Each index reflects an unmanaged universe of securities without any deduction for advisory fees or other expenses that would reduce actual returns, as well as the reinvestment of all income and dividends. An actual investment in the securities included in the index would require an investor to incur transaction costs, which would lower the performance results. Indices are not actively managed and investors cannot invest directly in the indices.

S&P 500®: Standard & Poor’s (S&P) 500® Index. The S&P 500® Index

is an unmanaged, capitalization-weighted index designed to measure the performance of the broad US economy through changes in the aggregate market value of 500 stocks representing all major industries.

Stocks: Standard & Poor’s (S&P) 500® Index. The S&P 500® Index is an unmanaged, capitalization-weighted index designed to measure the performance of the broad US economy through changes in the

aggregate market value of 500 stocks representing all major industries.

Bonds: The Bloomberg Barclays US Aggregate Bond Index: The Bloomberg Barclays US Aggregate Bond Index is a broad-based benchmark that measures the investment grade, US dollar- denominated, fixed-rate taxable bond market. The index includes Treasuries, government-related and corporate securities, MBS (agency fixed-rate and hybrid ARM pass-throughs), ABS and CMBS (agency and non-agency).

Sector/Industries: Sector/industry references in this report are in accordance with the Global Industry Classification Standard (GICS®) developed by MSCI Barra and Standard & Poor’s. The GICS structure consists of 11 sectors, 24 industry groups, 68 industries and 157 sub- industries.

© Copyright 2018 Richard Bernstein Advisors LLC. All rights reserved. PAST PERFORMANCE IS NO GUARANTEE OF FUTURE RESULTS

Nothing contained herein constitutes tax, legal, insurance or investment advice, or the recommendation of or an offer to sell, or the solicitation of an offer to buy or invest in any investment product, vehicle, service or instrument. Such an offer or solicitation may only be made by delivery to a prospective investor of formal offering materials, including subscription or account documents or forms, which include detailed discussions of the terms of the respective product, vehicle, service or instrument, including the principal risk factors that might impact such a purchase or investment, and which should be reviewed carefully by any such investor before making the decision to invest. Links to appearances and articles by Richard Bernstein, whether in the press, on television or otherwise, are provided for informational purposes only and in no way should be considered a recommendation of any particular investment product, vehicle, service or instrument or the rendering of investment advice, which must always be evaluated by a prospective investor in consultation with his or her own financial adviser and in light of his or her own circumstances, including the investor’s investment horizon, appetite for risk, and ability to withstand a potential loss of some or all of an investment’s value. Investing is subject to market risks. Investors acknowledge and accept the potential loss of some or all of an investment’s value. Past performance is, of course, no guarantee of future results. Views represented are subject to change at the sole discretion of Richard Bernstein Advisors LLC. Richard Bernstein Advisors LLC does not undertake to advise you of any changes in the views expressed herein.

© Richard Bernstein Advisors LLC

© Richard Bernstein Advisors

Read more commentaries by Richard Bernstein Advisors

Source: Bloomberg Finance L.P.

Source: Bloomberg Finance L.P.