Summary

- Further Thoughts On Trade Policy

- The Costs of Cybersecurity

- France Tries To Reform Labor Markets

I was first exposed to trade as an 8-year-old. I was a collector of baseball cards, each of which had a picture of a player on one side and an enumeration of his achievements on the other. Each year, my ultimate goal was to acquire a complete set.

My initial strategy was to purchase packages of cards until I had every player, but that proved costly and left me with many duplicates. A friend then taught me that exchanging excesses for missing items was a superior strategy. That experience began my lifelong appreciation of free trade.

International commerce in goods and services is certainly more complicated than grade school exchanges of collectibles. But the broad concept—that trading maximizes outcomes for participants—is the same. As the United States and its economic correspondents contemplate trade restrictions, they would do well to remember this basic principle. We’ve written about the American steel tariffs in each of the last two weeks. But there remain some important points to make on the topic of trade.

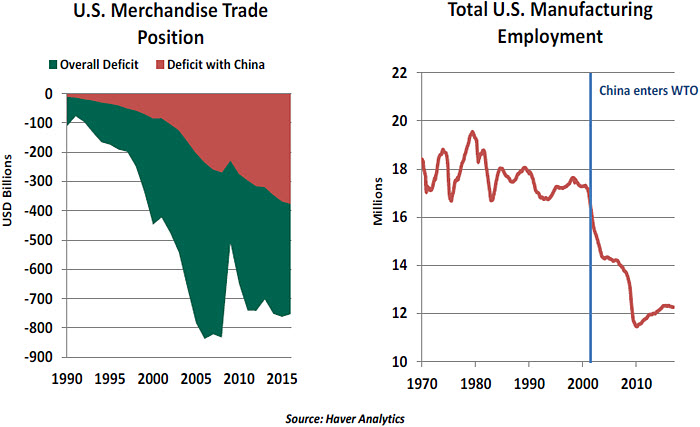

1. The presence of a trade deficit does not mean that one side is playing unfairly. Different countries specialize in making different things. People in different countries may consume different baskets of goods. This means there will be situations in which flows of merchandise are not entirely even between nations. It should also be noted that countries trade services as well as goods, which can even out accounts. The United States, for example, exports more than $200 billion more services than it imports each year.

2. China’s trade practices warrant attention. The annual deficit with China accounts for half of the overall U.S. trade imbalance. Since China was granted entry to the World Trade Organization (WTO) in 2001, heavy industry and its accompanying employment have rapidly migrated east across the globe.

To be fair, this arrangement has brought broad benefits, including lower prices and wider selection, to U.S. consumers. But it has made things difficult for some American industries and the communities that house them.

China has periodically expressed a wish to open its economy more completely over time. U.S. exports to China have, in fact, grown substantially over the past 20 years. But a variety of restrictions continue to make it difficult for foreign firms to gain access to Chinese markets, and the potential theft of intellectual property remains a risk.

There is consensus that some rebalancing is needed, but analysts differ in their recommended angles of approach. Back-channel negotiations seem to be giving way to more outward confrontation, raising the risk of overreaction.

3. Re-shoring manufacturing is not easy. Once production moves away, it is difficult to bring back. Old facilities may have been demolished; those that remain may be technologically obsolete. Steel-making has changed significantly in the past generation, with a movement toward smaller mills and smaller, highly-skilled workforces. Tariffs may therefore not produce the gains in industry employment that protectionists are hoping for.

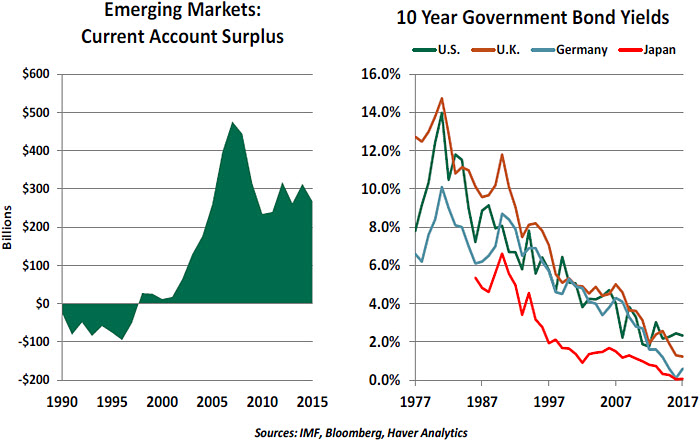

4. Trade flows and capital flows are mirror images. Dollars earned trading with the United States are often reinvested in this country, creating a kind of vendor financing system. Monies flowing in from emerging nations have helped limit the cost of U.S. debt and the consequences of growing fiscal deficits. Long-term interest rates in a range of developed countries have been falling persistently over the past 20 years, thanks in large part to an influx of foreign capital.

Trade restrictions would tend to diminish the surpluses earned by emerging markets, and by consequence, their appetite for U.S. government bonds. Production and profits would shift back to America, where saving rates are much lower than they are in Asia. This transition could make it more difficult for the Treasury department to issue debt at reasonable prices.

5. There are rules governing international trade, but enforcing them is a challenge. The WTO has served as a coordinating body for global commerce since 1995. Its charter is to establish guidelines, monitor compliance and adjudicate disputes. Even before the current tariff tiff, the number of disputes raised to the WTO for resolution had been increasing with the rise of protectionist impulses in many countries. And Brexit may add considerably to the WTO’s case load in the years ahead.

There are a handful of ways to justify protection, but countries have stretched them to their limits. (The U.S. steel tariffs were rationalized as enhancing national security, even though the country’s steel supply is not at great risk.) Mediating between nations in an environment of growing nationalism has been difficult, and may only get more so.

Countries may choose to seek forgiveness rather than permission, and resolution could take a very long time. While it is not our base case, a scenario where the global trade order breaks down is not difficult to describe.

Like other collectibles, baseball cards enjoyed a huge surge in value in the 1980s. (The “Economist” called it a classic financial mania.) Seeking to capitalize, I went back to my family home to locate the shoeboxes full of cards I had accumulated over the years. Sadly, my mother had discarded them as part of a decluttering program. Thousands of dollars had been chucked down the trash chute.

As we collectively contemplate free trade, we must be careful not to discard the substantial value created by international exchanges. While periodic calibration is needed, trashing the present system would be a tragedy.

Electronic Threats Have Real-World Costs

Cybersecurity once sounded like a fantastical field, with “white hats” fighting hackers. Recent headlines portray it as a very real challenge, affecting 57 million Uber passengers, 70 million Target customers, 148 million consumers with an Equifax credit file, 3.5 billion Yahoo accounts and millions more victims of other breaches. Almost everyone with an electronic identity has probably been the victim of some sort of data breach. Cybersecurity can be a personal issue, but it also has broad consequences for the global economy.

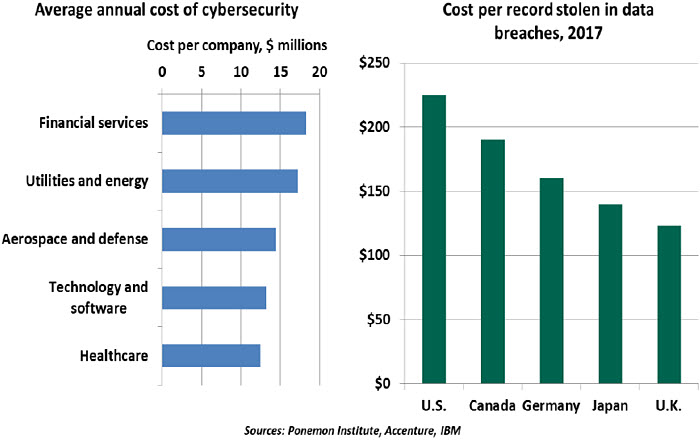

Readers of this publication are not expected to be experts in technical security concepts; we trust our security experts to defend us. They perform well, but at a cost. The 2017 Cost of Cyber Crime Study by Accenture and the Ponemon Institute estimated that the average cost of cybersecurity was $11.7 million per year to large companies, with many sectors showing higher costs.

Security is a collective problem: Attacks against one entity are easy to repeat elsewhere. Industry professionals have responded by creating information sharing and analysis centers (ISACs) for various industries, including financial services, healthcare, national defense, electricity and other critical sectors. ISACs allow security professionals to share information in real time and coordinate responses to immediate and long-term threats. This collaboration is crucial as attacks and perpetrators continue to evolve. Cybercrime has grown from an individual pursuit to a more organized form of crime, with some attacks believed to be state-sponsored.

The expenses of preventing cybercrime sound intimidating, but they pale against the cost of a data breach. The estimated cost of breaches can exceed $200 per record; when millions of records are stolen, the business risks are material. If intellectual property is taken that reveals strategic information or allows copying of patented goods, the damage can be incalculable.

Detecting and stopping the breach is not easy, but in many cases, it’s only the beginning of the effort and expense. Companies must investigate the root cause of the incident and communicate the breach to any affected parties. In the event of a consumer data breach, the company can expect to pay for credit monitoring. Breached companies may be subjects of drawn-out litigation and reputational damage lasting years beyond the incident.

In terms of their potential impact to a business, data breaches are idiosyncratic risks, like a fire or an earthquake. This has led to a growing global market for cyber insurance, which helps companies mitigate the costs of recovery from a breach. Global reinsurer Aon estimated that more than $2.3 billion in premiums were paid for cyber insurance in 2016, a figure poised to grow as more small to medium-sized firms adopt these policies. As we can see, even the most secure companies will still incur millions of dollars of expenses protecting their assets and insuring against losses.

Our modern lives are digital. This transformation has been generally good, improving our productivity and making a wealth of new information available at unprecedented speed. Thanks to the digital migration, entire industries have emerged and millions of jobs have been created.

However, this transformation has created new risks. As payments, ledgers and communications have moved away from paper, we have put the very infrastructure of our economy at risk. A significant attack could do lasting damage to our confidence in our financial systems. Maintaining security is crucial not just to prevent financial losses, but for the functioning of the economy broadly. By staying vigilant and protecting our data in all aspects of our lives, we can make our economy safer.

France Attempts to Emulate the German Model

French President Emmanuel Macron has taken aim at his country’s labor market, considered the most rigid in the region. The progress of reform is being closely watched.

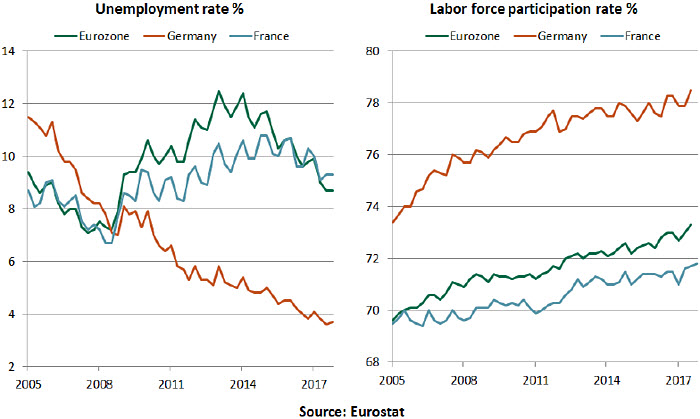

France’s labor market conditions have improved modestly over the past two years, with the unemployment rate down to a 5-year low of 9.3%. But that is more than twice the rate in Germany. The labor force participation rate is also low by European standards, and well below that of Germany.

Structural impediments are thought to account for an important portion of these differentials. Unlike in Germany, a company in France that is making profits is not entitled to lay off employees in any plant or department, even in a money-losing subsidiary. Furthermore, wage negotiations have become more decentralized in Germany but remain stringent in France. Despite low union membership, France is also known for widespread collective bargaining in the private sector.

The French labor market is also grappling with skills shortages, though this is likely to diminish with the current revamp of system of professional training.

Macron’s reforms appear to be an attempt to emulate the German model, which is aimed at improving flexibility and redirecting savings towards investments that boost productivity. A component of the reform is to make hiring and firing easier for employers. An early focus for Macron has been France’s state-owned rail operator, and he is now headed for a clash with the powerful rail union. The decline in Macron’s approval ratings to below 50% further highlights the opposition to reforms.

The evolution of France’s labor markets will take time. But the process is off to a promising start, as only a few strikes and protests have been witnessed. Reform is likely to face several speed bumps ahead, but a successful completion will serve as a model for others in the region.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2018 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/disclosures.

© Northern Trust

Read more commentaries by Northern Trust