Diamond Jewelers, Gold Coins and the Paradox of Indian Banking

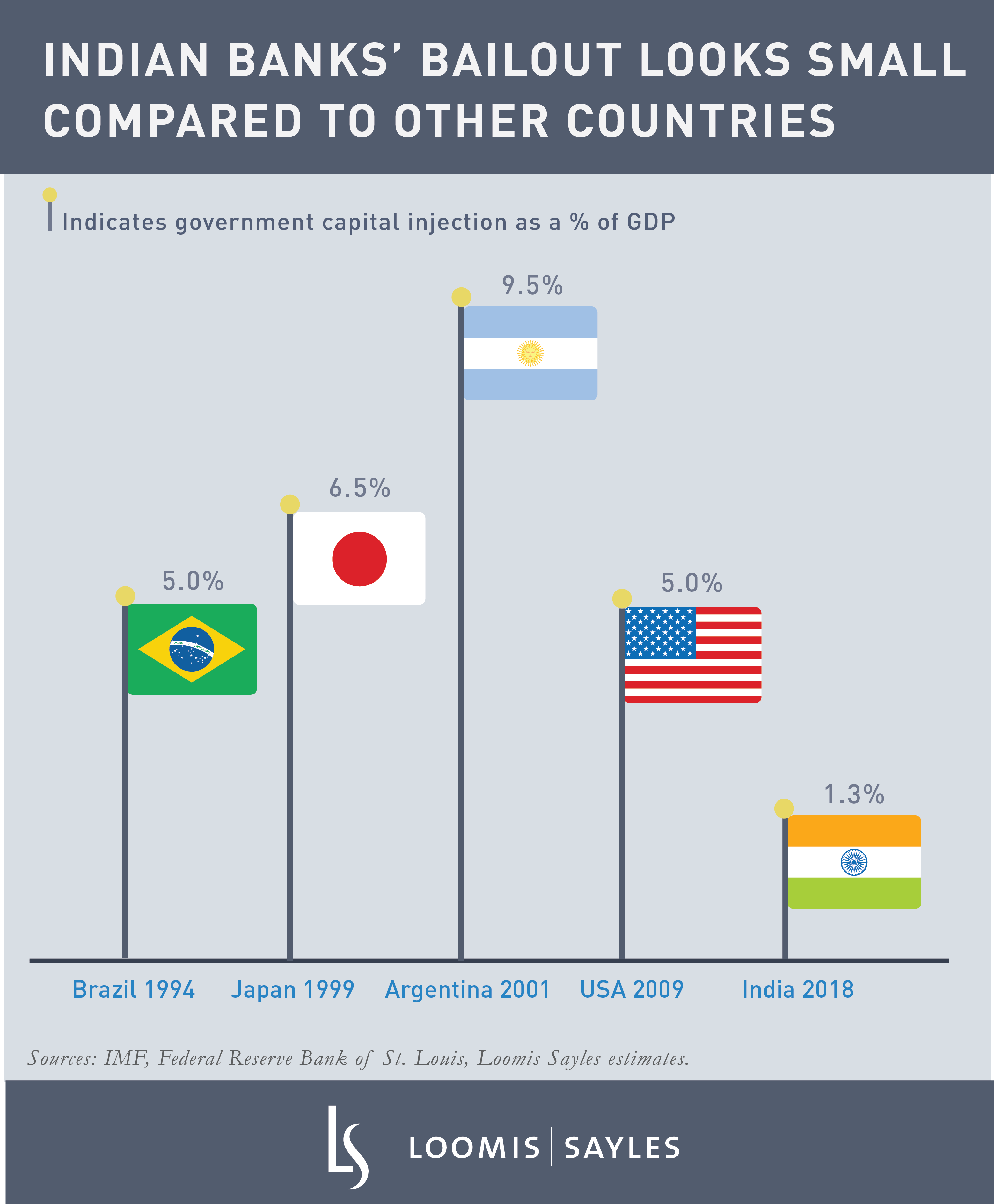

Many of India’s state-owned banks are in trouble. This month the government is injecting $13 billion to help these banks offload non-performing loans. By 2020, the total cost of injections is projected to rise to $21 billion, about 1.3% of GDP. It seems like an odd time for a non-performing loan crisis since the Indian economy hasn’t had a recession since 2010. So what’s going on? Why are the state-owned banks struggling even while the economy is growing at 7%?

Over-Optimistic Forecasts, Corruption and Red Tape

More than 13% of state-owned banks’ loans are classified as non-performing. Many of the unpaid loans were for construction on power plants, ports and roads. These projects were based on over-optimistic economic forecasts, and some were delayed for years by corruption and red tape. Other unpaid loans were made to tycoons with political connections, like the founder of now-defunct Kingfisher Airlines. The state-owned banks have been slow to admit the scale of the problem. For example, bankers rated the borrowings of struggling Bhushan Steel as “performing,” even after the vice-chairman of Bhushan Steel was arrested for bribing the chairman of Syndicate Bank to keep extending the loans.

New problems continue to emerge. Earlier this year, Punjab National Bank admitted that it lost up to $2 billion in a diamond jeweler’s fraud scheme. The jeweler bribed bank employees with gold coins for issuing fake credit guarantees.