The increasing costs of health insurance borne by employees and employers alike has spawned a variety of plans and strategies to help manage the expenses. Among these are health savings accounts (HSAs), which first came onto the scene in 2003. HSAs allow individuals who are covered by high-deductible health plans to receive tax-preferred treatment of money they have saved for medical expenses. Kevin Murphy, our national retirement plan strategist, explains the benefits of HSAs, and how they can even help build your retirement savings.

Every year Franklin Templeton conducts its Retirement Income Strategies and Expectations (RISE) survey,1 asking individuals how prepared they are for retirement, the strategies they have used to save for it and what concerns them most about their post-work life. Concerns about health care expenses often top the list of worries among survey respondents. In fact, in the 2018 RISE survey, paying for medical and pharmaceutical expenses was the number one expense individuals were concerned about in retirement. And that’s no surprise, as health care planning—or lack thereof—can directly impact one’s retirement for the better or worse.

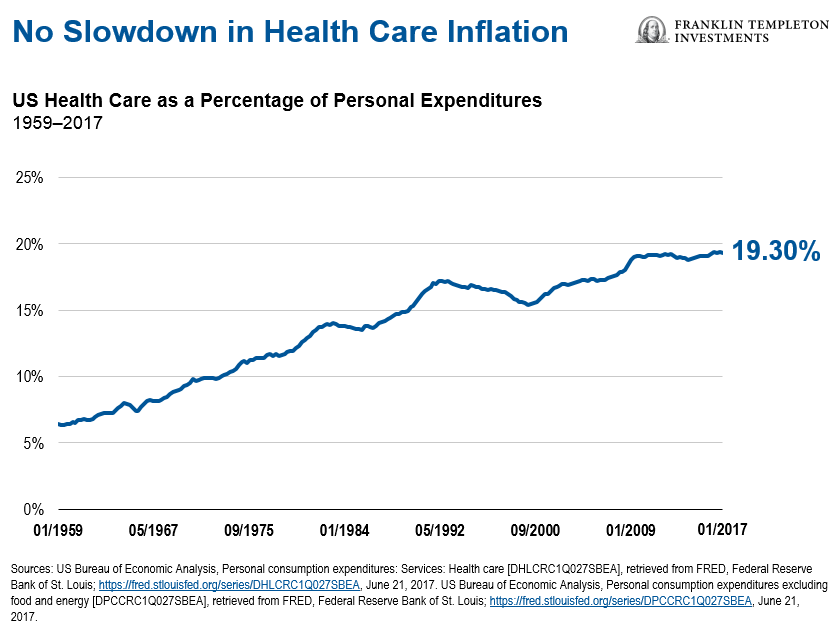

Health Care Costs on the Rise

The amount US employers spend on employee benefits rose 24% between 2001 and 2015.2 That is almost exclusively due to the rising cost of health care, which has more than doubled during that time frame. And, retiree health care expenses are expected to continue to outpace the overall US inflation rate, as well as annual projected Social Security cost-of-living adjustments (COLAs).3

To put the cost of health care into perspective, in a 2017 report, HealthView Services projected the basic total lifetime premium costs for a healthy 55-year-old couple retiring in 10 years would amount to an estimated $410,002.4

Health care costs have continued to take a larger share of our overall expenses (see chart below) and the trend doesn’t appear to be slowing.

The ABCs of HDHPs and HSAs

High-deductible health plans (HDHPs) have been one solution to help employers and employees cope with rising health care costs. Along with traditional health care plans, increasing numbers of employers have been offering these plans, which can provide greater upfront savings to the employer than traditional plans, and significantly lower premiums for individuals. As the name implies, an HDHP has a higher deductible than a traditional health insurance plan. The individual is responsible for paying medical expenses up to a specified level. After meeting the deductible threshold coverage kicks in. Certain aspects of care may be covered in full outside the deductible, such as yearly exams and preventative care.

A Health Savings Account (HSA), which is used in conjunction with an HDHP, allows users to save money tax-free to pay for qualified health care expenses paid out of pocket And, HSAs can be used for health care expenses not only in one’s working years, but also in retirement. In this sense, the HSA represents the intersection of retirement and consumer-driven health care. In fact, 75% of companies which offer HSAs to their employees regard the HSA as part of their retirement benefits.5

The Main Advantages of an HSA

There are three main advantages of an HSA.

- Contributions are not subject to income tax.

- Earnings and interest grow tax-free.

- Withdrawals are tax-free if used to pay for qualified medical expenses.

As HSA participants direct where to invest the funds (which can include vehicles such as mutual funds), HSAs are often thought of like an Individual Retirement Account or 401(k) plan for medical expenses, and a great complement to these long-term retirement savings strategies. Both offer tax-deductible contributions, but the main difference is that while most individuals won’t touch their 401(k) assets until they retire, it’s more likely individuals will need to access their HSA savings periodically before then. This is worth highlighting, as an HSA also offers the benefits of tax-free withdrawals, no Social Security/Medicare tax on contributions and no required minimum distributions.6

A Growing Pool

Individuals are eligible for an HSA if they are covered by an HDHP, are not a dependent on another’s tax return and not covered by any other health insurance plan. There are also yearly contribution limits. For 2018, the limit is $3,450 for an individual and $6,900 for a family. If one is over the age of 55, then he or she can contribute an additional $1,000. If you have one of these plans—particularly if you are healthy—you may not feel you need to set aside this much.

However, setting aside more money for health care today may mean greater peace of mind tomorrow. The assets will continue to grow tax-free until you need them, even into retirement, when you can use the money for the health expenses Medicare doesn’t cover.

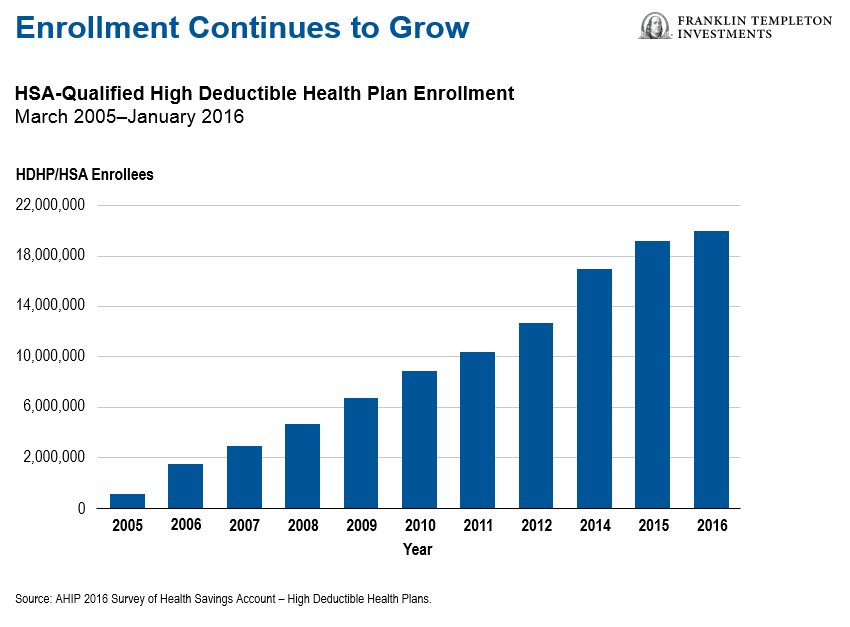

These plans have been growing increasingly more popular, with the number of enrollees growing 10-fold since 2005 (see chart below). Assets in HSAs are projected to reach $44.4 billion at the end of 2018, up from nearly $38 billion at the end of 2017 and just $1.6 billion at the end of 2006, according to Morningstar’s 2017 Health Savings Account Landscape report.7

No One-Size-Fits-All Approach

When it comes to health care coverage, what’s appropriate for one individual or family might not be appropriate for another. If you choose an HSA plan, you’ll want to give careful consideration to how your assets are invested based on your personal situation, including your risk-tolerance, needs and goals.

Of course, there are always trade-offs with any type of health plan, and I certainly would not want to imply an HSA is right for everyone. It’s important to weigh the pros and cons. But, if you are healthy and can afford a higher deductible, an HSA can also help build your retirement savings.

For financial advisors who are interested in resources and business development ideas to support their HSA practice, please contact us at (800) 342-5236.

This information is intended for US residents only.

What are the Risks?

All financial decisions and investments involve risks, including possible loss of principal.

This communication is general in nature and provided for educational and informational purposes only. It should not be considered or relied upon as legal, tax or investment advice or an investment recommendation, or as a substitute for legal or tax counsel.Any investment products or services named herein are for illustrative purposes only, and should not be considered an offer to buy or sell, or an investment recommendation for, any specific security, strategy or investment product or service. Always consult a qualified professional or your own independent financial advisor for personalized advice or investment recommendations tailored to your specific goals, individual situation, and risk tolerance.

Franklin Templeton does not provide legal or tax advice. Federal and state laws and regulations are complex and subject to change, which can materially impact your results. Franklin Templeton Distributors, Inc. cannot guarantee that such information is accurate, complete or timely; and disclaims any liability arising out of your use of, or any tax position taken in reliance on, such information.

Data from third party sources may have been used in the preparation of this material and FTI has not independently verified, validated or audited such data. FTI accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments opinions and analyses in the material is at the sole discretion of the user.

______________________________________________

1. The 2018 Franklin Templeton Retirement Income Strategies and Expectations (RISE) survey was conducted online among a sample of 2,002 adults comprising 1,002 men and 1,000 women 18 years of age or older. The survey was administered between January 17 and 25, 2018, by ORC International’s Online CARAVAN®, which is not affiliated with Franklin Templeton Investments. Data is weighted to gender, age, geographic region, education and race. The custom-designed weighting program assigns a weighting factor to the data based on current population statistics from the US Census Bureau.

2. Source: Willis Towers Watson press release, “Employers cost to provide employee benefits has risen 24% since 2001,” July 18, 2017.

3. Sources: Willis Towers Watson press release, “Employers cost to provide employee benefits has risen 24% since 2001,” July 18, 2017; Bureau of Labor Statistics. There is no assurance that any estimate, forecast or projection will be realized.

4. HealthView Services, “2017 Retirement Health Care Costs Data Report©.” National averages are used for supplemental insurance premiums, which vary by state. Total lifetime projections comprise all out-of-pocket (OOP) expenses related to hospitalization, doctors and tests, prescription drugs, vision, dental hearing services and hearing aids. All calculations assume that a healthy male and female will have life expectancies of 87 and 89 respectively, and will have a combined future modified adjusted gross income (MAGI) of under $170,000. For illustrative purposes only. There is no assurance that any estimate, forecast or projection will be realized.

5. Source: Plan Sponsor Council of America, Health Savings Accounts and Retirement Plans, 2017.

6. If HSA is used for qualified medical expenses.

7. Source: Morningstar 2017 Health Savings Account Landscape. For additional data provider terms and conditions, see www.franklintempletondatasources.com.

© Franklin Templeton Investments

© Franklin Templeton Investments

Read more commentaries by Franklin Templeton Investments