In their second-quarter (Q2) 2018 outlook, K2 Advisors’ Research and Portfolio Construction teams share their views on why investors should not fear the return of market volatility—and why it may unlock opportunities for active managers. We believe offering these insights will help investors better understand the rationale for owning retail mutual funds that invest in hedge strategies.

Don’t Fear the Fear Index

We suggested at the end of last year that when the massive tide of global liquidity injected into markets post-2008 begins to recede, a wave of volatility could follow. It appears as though the wave has arrived.

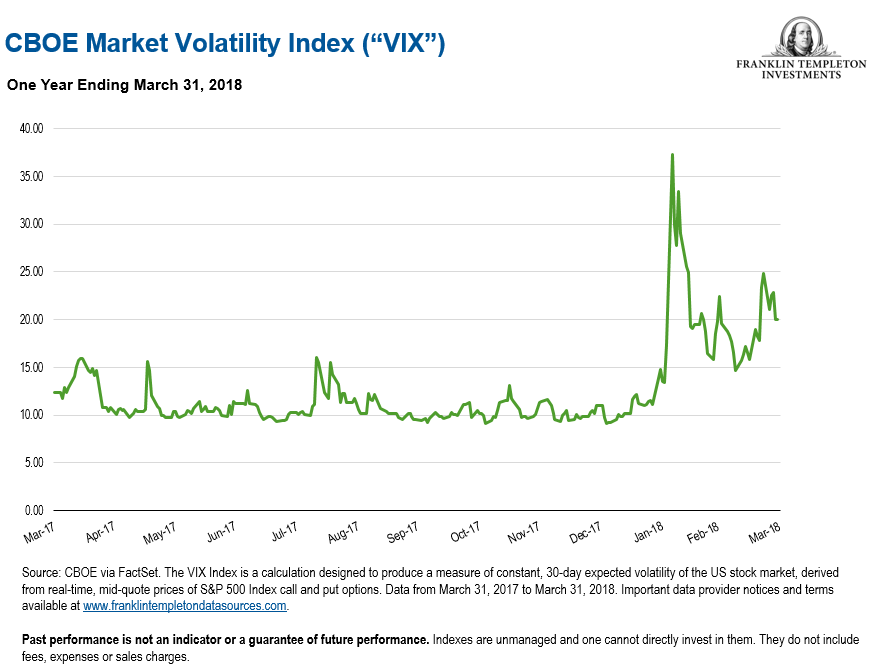

Market volatility—as measured by the VIX (the so-called “fear index”)—surged 80% in the first quarter of the year. The S&P 500 Index and Dow Jones Industrial Average both declined for the quarter respectively, while the Nasdaq Composite Index managed a modest gain based largely on its sharp rise in January. Nine out of 11 S&P 500 sectors traded lower.

The steepest declines were in telecommunication services, consumer staples, and energy. Information technology and consumer discretionary were positive outliers despite selling off broadly in March. The negative quarter for the S&P 500 Index broke a string of nine positive quarters, the longest streak in 20 years. In addition, all of this happened following the nine-year anniversary of the bull market, which began on March 9, 2009, and 10 years after the bailout of Bear Stearns.

So now what? From our perspective, a reversion from the unprecedented low levels of volatility was to be expected—perhaps even welcomed. In some ways it reflects the resumption of more normalized market behavior. This is a good thing, in our view.

As we have said in past commentaries, the historic levels of quantitative easing following the global financial crisis—that is the expansion of the Fed’s balance sheet from around $900 billion to nearly $4.5 trillion today—was one of the most dominant market-shaping forces over the last decade. In our view, it caused a distortion in prices, a suppression of volatility, and a reduced emphasis on corporate fundamentals.

In addition to yields being driven toward record lows and stock markets to record highs, many investors were pushed toward riskier assets while the cost of capital was kept artificially low. While passive investing thrived in such an environment, it could be argued that active management and hedge funds suffered. As this era of quantitative monetary stimulus slowly winds down, we believe an improved environment for active management will emerge.

Reduced central bank support should make stocks more responsive to idiosyncratic factors. The consensus thought seems to be that less-supportive monetary policy will lead to greater price sensitivity from individual company fundamentals, which in turn could lower pair-wise correlations. If this were to occur, we feel this should lead to greater sector dispersion as well, creating a more conducive environment for managers to identify potential winners and losers. As a result, we believe the environment for alpha capture1 for the remainder of 2018 may remain fertile.

Discretionary Macro

Our outlook for the discretionary macro strategy continues to improve. Increased central bank activism and policy divergence, combined with political uncertainty across major economies, have contributed to an increase in volatility across major asset classes. The increase, while modest, is nevertheless indicative of higher uncertainty and potentially better trading opportunities for managers with flexibility to trade across asset classes (most notably in fixed income and currencies, which have traditionally been a core area of focus for discretionary managers).

Long/Short Equity – Europe

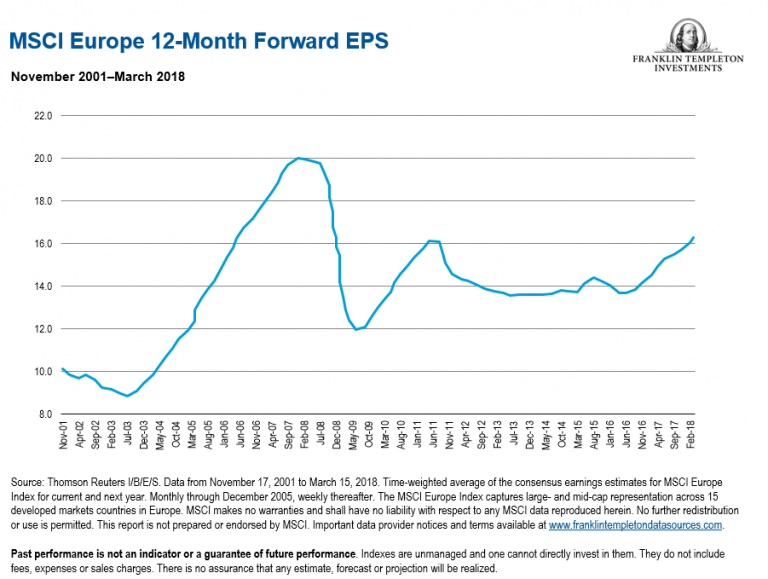

The opportunity set in Europe remains favorable for long/short equity managers. European equities continue to trade below their historical average valuation versus the United States, which we believe to be fully valued. Eurozone forward earnings estimates are trading well below their prior peak, providing ample room for further recovery. US forward earnings, by contrast, are well above their 2008 peak.

European economic growth should continue to improve with low rates, resumption in bank lending, and strong external expansion. We believe the fears of a catastrophe following the Brexit decision are beginning to subside, as the issue appears to be reaching an amicable end for both Europe and the United Kingdom. In addition, Europe looks to be positioning itself close to the Trump administration at the trade table, likely putting it in a better position related to China or Japan in terms of any tariff actions by the administration.

Furthermore, the alpha environment appears strong with increased dispersion and decreased correlations2 impacted by varied regional macro developments, ECB meetings and elections.

Relative Value – Fixed Income

With interest rates finally starting to rise, duration3 risk is coming into focus for fixed income investors. Relative value fixed income managers such as long/short credit managers appear well positioned, given their shorter duration portfolios, and, in our view, should be able to generate alpha from rising sector dispersion.

The diverging paths of central banks in the major global economies are expected to present improved directional opportunities. Participation from directional buyers and sellers of bonds should result in greater market inefficiencies between cash bonds and futures, benefiting less directional relative value trading. The strategy is still subject to greater leverage and funding risks, justifying a cautious approach.

Comments, opinions and analyses expressed herein are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. Because market and economic conditions are subject to rapid change, comments, opinions and analyses are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy.

Data from third party sources may have been used in the preparation of this material and Franklin Templeton has not independently verified, validated or audited such data. Franklin Templeton and its third party sources accept no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user. Important data provider notices and terms available at www.franklintempletondatasources.com.

This information is intended for US residents only.

What Are the Risks?

All investments involve risks, including possible loss of principal. Investment in these types of hedge-fund strategies is subject to those market risks common to entities investing in all types of securities, including market volatility. There can be no assurance that the investment strategies employed by hedge fund and liquid alternative managers will be successful. It is always possible that any trade could generate a loss if the manager’s expectations do not come to pass. Hedge strategy outlooks are determined relative to other hedge strategies and do not represent an opinion regarding absolute expected future performance or risk of any strategy or sub-strategy. Conviction sentiment is determined by the K2 Advisors’ Research group based on a variety of factors deemed relevant to the analyst(s) covering the strategy or sub-strategy and may change from time to time in the analyst’s sole discretion.

For more information on any of our funds, contact your financial advisor or download a free prospectus. Investors should carefully consider a fund’s investment goals, risks, sales charges and expenses before investing. The prospectus contains this and other information. Please read the prospectus carefully before investing or sending money.

________________________________________

1. Alpha measures the difference between a fund’s actual returns and its expected returns given its risk level as measured by its beta. A positive alpha figure indicates the fund has performed better than its beta would predict. In contrast, a negative alpha indicates a fund has underperformed, given the expectations established by the fund’s beta. Some investors see alpha as a measurement of the value added or subtracted by a fund’s manager.

2. Correlation represents the linear relationship between two return series. Correlation shows the strength of the relationship between two return series. The higher the relationship, the more similar the returns.

3. Duration represents a measure of the sensitivity of the price (the value of principal) of a fixed-income investment to a change in interest rates. Duration is expressed as a number of years.

© Franklin Templeton Investments

© Franklin Templeton Investments

Read more commentaries by Franklin Templeton Investments