The cost of a college education continues to rise, and along with it, student debt. Roger Michaud, senior vice president and director of college savings for the Franklin Templeton 529 College Savings Plan, and Mike O’Brien, director, Program Marketing, Global Client Marketing, look at how mounting student debt could have a long-term impact on one’s future. They explore one solution to help finance education—a 529 Savings Plan—along with some myths and misconceptions about these plans. You may be surprised to learn they aren’t just for college, nor are they only for children.

A Look at the Numbers

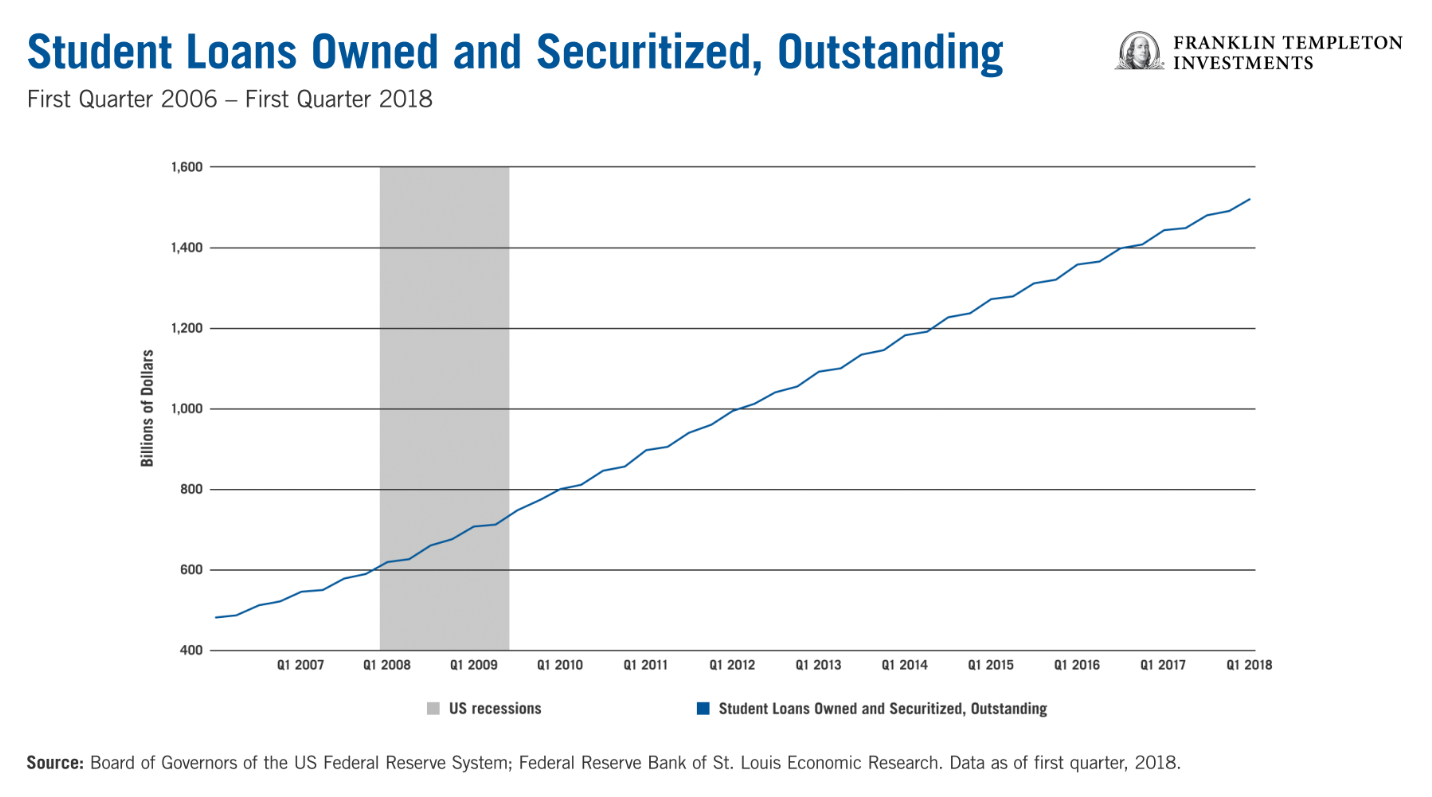

Student loan debt in the United States has continued to mount. As of the first quarter of 2018, more than $1.5 trillion in student loan debt was outstanding, triple that of 2001.1 Various estimates show the average student loan is now more than $30,000 at graduation—a sizable sum to be saddled with.

The amount of student-loan debt actually exceeds that of US auto- or credit-card debt. We are even starting to see a new generation of parents who are still paying off their own student debt while raising children of their own. These parents are stuck in a student loan debt sandwich. Not only do they have their own student debt, but they have to finance their children’s education, sometimes with more debt.

As a result of a high debt burden, many recent graduates are living at home with their parents instead of moving out, and/or staying at home longer than they anticipated. Researchers at the Federal Reserve recently studied whether student-loan debt might be acting as a restraint on US economic growth. While increases in debt payments since 2001 appear to have had only a small direct effect on consumption overall so far, increased student-loan debt may have other impacts, including the loss of access to other types of loans, for a car or house, for example.2 So, many young adults may be delaying purchases or even putting off getting married or buying a house of their own due to financial constraints.

If one is paying off a loan for 10 or 15 years, that money is not available for other types of purchases—or for saving for a long-term goal, including retirement. Some individuals even wind up tapping their 401(k) plans to pay off student-loan debt. In fact, a 2015 Franklin Templeton survey revealed nearly a quarter of individuals (23%) would withdraw money from their retirement account to finance college education.3

Of course, once you already have the debt you can’t go back and erase it. Our focus should be on how to help prevent the next generation from being overly burdened with it.

Debt as a Tool

One might be getting the impression that we think all debt is bad. That is certainly not the case—debt can be a powerful tool. According to the National Center for Education Statistics, the median earnings of adults aged 25-34 with a bachelor’s degree were 64% higher than those with only a high school diploma.4 And, those with a master’s degree earned 20% more than those with a bachelor’s degree.5 The pattern of higher earnings associated with higher levels of educational attainment held true for both male and females, as well as across ethnic groups.

The thing we would like to emphasize is that if you are going to take on student debt, borrow wisely, and be smart about your choices—pick the right school, don’t borrow more than you need to, and make sure you graduate! The worst case is to have the debt, but not the degree.

An Educational Savings Plan

Getting back to our new generation of parents, we stress that it’s important to get started as early as you can to develop a plan to pay for your child’s education. It doesn’t matter if your child is a newborn, 12 years old or even a teenager, it’s never too late to put a plan in place.

In our view, it’s important not only to make an initial contribution toward college savings, but to do it systematically so it has a chance to grow. Don’t be afraid to ask friends and family to contribute along the way. If asked, most family members are more than happy to contribute toward college costs for their nephew, niece or grandchild. In lieu of a holiday or birthday gift, we think a contribution to a college savings plan could be much more valuable down the road.

Many families use 529 plans to help manage and invest their college savings. States, state agencies or educational institutions can sponsor 529 plans, which are considered qualified tuition plans. Parents, grandparents and other family members and even friends can help a designated beneficiary save for college costs.

Money invested in these plans grows free of federal income tax when withdrawn for qualified higher education expenses such as tuition, books, and room and board (when attending at least half time). Depending on where you live, you may be able to take advantage of state tax benefits, too.6

Tax benefits of 529 plans are conditioned on meeting certain requirements. Federal income tax, a 10% federal tax penalty, and state income tax and penalties may apply to nonqualified withdrawals of earnings. Generation-skipping tax may apply to substantial transfers to a beneficiary at least two generations below the contributor. Gift examples are general; individual financial circumstances and state laws vary—consult a tax advisor before investing. If the contributor dies within the five-year period, a prorated portion of contributions may be included in his/her taxable estate. See our 529 plan Investor Handbook for complete information.

Setting the Record Straight

As we speak with individuals who are considering a 529 educational savings plan, there are some myths that often bubble up. We’ll outline a few we’ve heard.

Myth: 529 plans can only be used for schools in the plan’s state.

Fact: You can use a 529 plan for most schools in the United States no matter where your 529 savings plan is based.

Myth: There’s no point in opening a 529 plan if I don’t even know if my child will even go to college. What if he/she goes to a trade school?

Fact: A 529 plan is most often used for college, but can also be used for vocational schools, trade schools and now with the recent US tax law changes, it can be used for kindergarten through 12thgrade education, too. A 529 plan is no longer a college savings vehicle, it’s an educational savings vehicle.7

Myth: Only parents can open a 529 plan.

Fact: You can open an account for nearly anyone—a child, a grandchild, a friend or even for yourself! Many adults wish to change careers sometime during their lifetime, or even take classes to enrich their lives in retirement. In many cases, you can tap your assets in your 529 plan for these purposes.

Myth: Once the 529 plan is established for an individual, you can’t change the beneficiary if he or she doesn’t need it.

Fact: You can change the beneficiary of the plan to another member of your family. As noted, you can even make the beneficiary yourself for educational purposes—even if it’s for education related to a hobby, for example.

Want More Information and Strategies?

We’ve only scratched the surface of this important topic. We encourage you to learn more.

Learn about 529 College Savings Plans at Franklin Templeton and talk to an advisor for savings ideas and strategies that are best for you and your family. And, check out Franklin Templeton’s Spryng™ Crowdfunding tool.

The comments, opinions and analyses expressed herein are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. Because market and economic conditions are subject to rapid change, comments, opinions and analyses are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy.

This information is intended for US residents only.

What Are the Risks?

All investments involve risks, including possible loss of principal. 529 plan underlying funds have risks that will cause your investment return and principal value to fluctuate. Stocks tend to fluctuate dramatically over the short term. Bond prices generally move opposite to interest rates; as bond prices adjust to a rise in interest rates, a fund’s share price may decline. High-yield, lower-rated bonds generally have greater price swings and higher default risks. Foreign investing, especially in developing markets, has additional risks such as currency and market volatility and political or social instability. These and other risks are discussed in each fund’s prospectus.

Tax benefits are conditioned on meeting certain requirements. Federal income tax, a 10% federal tax penalty, and state income tax and penalties may apply to nonqualified withdrawals of earnings. Generation-skipping tax may apply to substantial transfers to a beneficiary at least two generations below the contributor. Gift examples are general; individual financial circumstances and state laws vary—consult a tax advisor before investing. If the contributor dies within the five-year period, a prorated portion of contributions may be included in his/her taxable estate. See the Investor Handbook for more complete information.

An investment in Franklin Templeton 529 College Savings Plan does not guarantee any specific rate of return or that your college investing goals will actually be met. The value of an investment in the plan may fluctuate, and investors may have a gain or a loss from investment in the plan.

This is not a recommendation of any particular security, is not based on any particular financial situation or needs, and is not intended to replace the advice of a qualified financial advisor. Before making any financial commitment regarding a Section 529 college savings plan, consult with an appropriate financial advisor.

Investors should carefully consider Section 529 college savings plan investment goals, risks, charges and expenses before investing. To obtain a 529 plan disclosure document, which contains this and other information, talk to your financial advisor or call Franklin Templeton Distributors, Inc., the manager and underwriter for a 529 plan at (800) DIAL BEN / (800) 342-5236 or visit franklintempleton.com. You should read the 529 plan disclosure document carefully before investing or sending money and consider whether your or the account beneficiary’s home state offers any state tax or other benefits that are only available for investments in its qualified tuition program.

____________________________________________________________________________

1. Source: Federal Reserve Bank of St. Louis, “Student Loans Owned and Securitized, Outstanding.” Data as of first-quarter 2018.

2. Source: US Federal Reserve FEDs Notes, “Student Loan Debt and Aggregate Consumption Growth,” February 2018.

3. Source: The Franklin Templeton College Savings Trends Survey was conducted online among a sample of 1,009 adults comprising 506 men and 503 women 18 years of age and older. The survey was administered between April 30–May 3, 2015, by ORC International’s Online CARAVAN, which is not affiliated with Franklin Templeton Investments. Data is weighted to gender, age, geographic region, education and race. The custom-designed weighting program assigns a weighting factor to the data based on current population statistics from the U.S. Census Bureau. Children are defined as those age 18 or younger in the household

4. Source: National Center for Education Statistics, FastFacts, Income of young adults. Data as of 2015.

5. Ibid.

6. It’s important to remember that, as with any investment, principal value may be lost, and investing in the plan does not guarantee admission to college or sufficient funds for college. There is no federal or state guarantee of investments in the plan.

7. 529 savings can be used at most accredited two- and four-year colleges and universities and vocational schools, including many outside the United States In addition, up to $10,000 per year per beneficiary can be used for tuition for eligible public, private and religious primary and secondary educational institutions (K-12.) It is not currently clear what public K-12 school costs, if any, will be regarded as tuition for this purpose. State tax benefits and treatment of withdrawals for K-12 tuition may vary by state, may not have been updated for changes in federal tax law and may be uncertain; consult a tax professional concerning your state.

© Franklin Templeton Investments

© Franklin Templeton Investments

Read more commentaries by Franklin Templeton Investments