The Federal Reserve’s Axis of Symmetry

Membership required

Membership is now required to use this feature. To learn more:

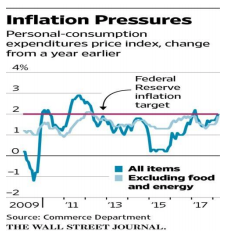

View Membership BenefitsThe Federal Reserve has two primary mandates: maximizing employment and stable prices. Congress also included moderating long-term interest rates as part of the Fed’s overall objective, but that should be the offshoot of stable prices. In May the unemployment rate fell to 3.8% which is the lowest since April 2000. If it drops to 3.7% in coming months as seems likely, it would be the lowest since October 1960. By any assessment the Fed has achieved its goal of maximizing employment. Prior to 2012 the Federal Reserve did not have an explicit inflation target. That changed on January 25, 2012 when Federal Reserve Chairman Ben Bernanke established a formal 2% target for inflation, as measured by the core Personal Consumption Expenditures price index (PCE) that excludes food and energy. The core PCE was 2.0% in January 2012, but then proceeded to decline and remained under 2.0% for most of the next six years. The failure wasn’t due to the lack of trying by the Fed as it kept interest rates near zero percent from 2008 until December 2015, and continued its QE programs until the end of 2014. The biggest drag came from the precipitous fall in oil prices from June 2014 until early 2016, which caused the All Items PCE to plunge and pulled the core PCE down as well.

In recent months the core PCE has been working its way back toward 2.0% and I expected the Fed to communicate that 2.0% was not a ceiling and would not overreact if the PCE went above 2.0% for a period of time. After the FOMC meeting on May 2 the Fed inserted the word symmetric into its post FOMC statement for the first time. “Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability. The Committee expects that, with further gradual adjustments in the stance of monetary policy, economic activity will expand at a moderate pace in the medium term and labor market conditions will remain strong. Inflation on a 12-month basis is expected to run near the Committee's symmetric 2 percent objective over the medium term.” The Fed has indicated that its 2.0% target will be an axis, rather than a ceiling and will allow the core PCE to drift above 2.0% without a change in monetary policy. Should the core PCE exceed 2.0% in coming months, the Fed will continue with its pace of gradual rate increases, but will not accelerate the pace. The Fed is almost certain to increase the federal funds rate again when it meets on June 13. Although the symmetric message was expressed in the FOMC statement on May 2, the bond market didn’t clearly get the message until the minutes of the May 2 meeting were released on May 23. From the close on May 22, the yield on the 10-year Treasury bond fell from 3.065% to 2.931% on May 25, with the yield on the 30-year Treasury falling to 3.090% from 3.209%

In the May 14 Weekly Technical Review (WTR) I discussed the price pattern in Treasury yields and why there was a decent chance that Treasury yields might top soon. “If Treasury yields rise above the April 25 high, the Treasury bond ETF TLT is likely to drop below the low of wave 3 ($116.51) and complete a 5 wave decline from the price high in September 2017. It took 3 months from the time TLT made its wave 3 low in December 2016 and the wave 5 low in March 2017. An equal amount of time from the wave 3 low on February 21 would target May 14 - May 21 as a guess of when Treasury yields will exceed their recent high and TLT records a low for wave 5. Establish a 50% position in TLT if it trades under $116.51 in the next few weeks.” On May 17, the 30-year Treasury yield rose to 3.247% and the 10-year yield topped out at 3.115%, as TLT dropped to $116.09 triggering the buy signal. In the May 21 WTR I made the following projections for TLT and Treasury yields. “Based on the price pattern, TLT has the potential to rally to near $121.00 in the next 1 to 3 months, while the yield pattern in the 10-year Treasury bond suggests its yield could fall below 2.75% and the yield for the 30-year Treasury bond could dip under 3.0%.”

In the May issue of Macro Tides, I discussed why Treasury yields were nearing a peak and why I expected yields to fall in the second quarter. “Although Treasury yields may spike above the April 25 highs, Treasury yields are nearing a peak. Technically, the recent increase appears to have completed a 5 wave advance in yields since the low in September, and positioning in Treasury bond futures show that Large Speculators have a record short position. Treasury yields are poised to decline during the second quarter.” While the release of the May 2 FOMC minutes provided an initial push for Treasury yields to fall, the hammer came on May 29 after Italy’s bond market swooned raising concerns about another European sovereign debt crisis and potentially the future of the European Union. The Italian 10-year yield soared from 1.76% on May 7 to 3.17% on May 29 before falling to 2.54% on June 4. The spike on May 29 caused global equity markets to shudder inspiring a flight to quality into Treasury bonds. On May 29, the five–year Treasury yield fell 18.5 basis points, while the 10-year yield dropped by 16.3 basis points, and the 30-year plunged by 12.2 basis points. The extraordinary plunge in yields was fueled by the positioning in Treasury bond futures as I discussed in the May 29 WTR. “The news coming out of Italy and the rise in Italian bond yields certainly provided the impetus for yields to decline. But the real octane came from the large short position in Treasury bond futures. One contract has a value of $100,000 and requires a margin of $4,300. Each one point move in Treasury bond prices represents $1,000. Since May 17, 30-year Treasury bond prices have soared from 140.16 to 146.21, or more than $6,000 for each futures contract. For any firm short Treasury bonds, this is a devastating loss in a short period of time. In order to maintain a short position which is losing so badly, a firm would likely receive a margin call and be required to bring in more money within one or two hours. If the firm fails to bring in more capital to maintain the position, the trading firm would simply liquidate the position. In the case of a short position, the liquidation would actually be a purchase of bond futures to close out the short position. The intensity of buying in Treasury futures today suggests a measure of panic buying was responsible for the huge one-day decline in interest rates.” On May 29, the 10-year Treasury yield fell to 2.759% and the 30-year reached 2.954%, very near the yield targets discussed in the May 21 WTR. The yield pattern suggests that yields could dip modestly below the lows on May 29. After that things could get interesting.

The bond market was relieved to learn the Fed would not over react if the core PCE exceeds 2.0%. However, should the core PCE start to approach 2.20% the bond market may become far less sanguine and begin to worry that some FOMC members may consider that inflation could become asymmetric and that the Fed may be falling behind the inflation curve. The core Consumer Price Index (CPI) tends to lead the core PCE and could help provide guidance as to when the bond market and the Fed might begin to worry that monetary policy is behind the curve. The core CPI reached 2.3% in January 2012 and a number of times in 2016 – March, July, September – and finally in February 2017. In May the core CPI was 2.1%. Basic chart analysis indicates that a rise above 2.3% would represent a break out and suggest that the core PCE could subsequently climb above 2.2% and trigger alarm bells first for the bond market and then within the Fed. The increase in inflation has been glacial so it is unlikely this development will occur in the next few months, but that could change before October.

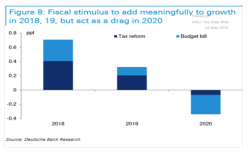

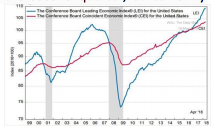

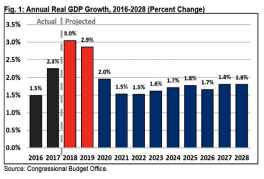

The tax cut and the increase in spending in the budget bill is projected to add 0.7% in 2018 with most of the stimulus taking hold in the next three quarters. The increase in gas prices is siphoning off some the kick from the tax cut especially for lower income earners as discussed in the May Macro Tides. “The after tax increase for a worker in the lowest percentile will only rise by 0.4%, but spending on gas consumes about 8% of their income. The 18.1% increase in the cost of filling their gas tank will cost them 1.4% more of their income (18.1% X 8.0%) compared to a 0.4% net income rise. For taxpayers in the second lowest quintile, the tax cut only marginally exceeds the increase in gas prices. For almost 40% of working Americans, the increase in the cost of driving their car exceeds the increase in their net pay or neutralizes most of the benefit from the tax cut.” The average cost for a gallon of gas was $2.97 on May 25, the highest since 2014. If it climbs and holds above $3.00 a gallon, the psychological impact on consumers could become more pronounced. This is one reason I doubt GDP will grow by 4.8% in the second quarter, as currently forecast by the Atlanta Fed’s GDPNow on June 1. Despite the drag from higher gas prices, GDP will pick up in the second quarter from 2.2% in the first quarter and could modestly exceed 3.0%. The Conference Board’s Leading Economic Indicator (LEI) is rising at a brisk pace which indicates that economic growth should continue at a solid pace in coming months. The LEI began to decline well in advance of the recessions in 2001 and 2008, so the risk of a recession developing before the end of 2018 is remote.

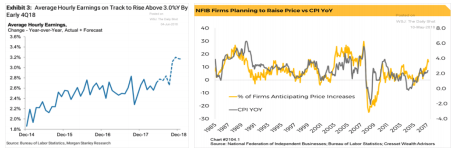

Economic growth in coming months will lower whatever remaining slack is left in the labor market and manufacturing. Upward pressure on wages will continue to build gradually and result in increases in Average Hourly Earnings and ECI wage growth to approach 3.0% before year end. According to Morgan Stanley, AHE and could be up 3.3% before year end.

According to a recent survey by the National Federation of Independent Businesses (NFIB), the percentage of small businesses that are planning to raise wages is the highest since 2006. Labor is the largest expense for the majority of companies irrespective of their size. If wage growth accelerates before the end of 2018, companies will be faced with a tough decision: either absorb higher wage costs and accept lower profit margins, or raise prices to cover the increase in labor costs.

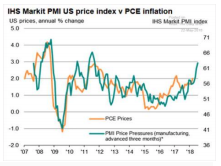

When there is an excess amount of slack in the production supply chain, delivery times are short and pricing power from material suppliers is weak. Conversely, when utilization rates are high, delivery times become more stretched and pricing power increases. According to the Institute of Supply Management (ISM), factories are now waiting 67 days for materials, which matches the longest period since 1987. The level of pricing power can be inferred by the percentage of firms that report paying higher prices in the monthly ISM manufacturing survey. In May ISM reported that 79.5% of the firms surveyed said they were paying higher prices, which is the highest level since 2011. The April monthly survey of manufacturers by IHS Markit found the same result and offered the following summary. “Warning lights are being flashed in relation to inflation, however, with factories reporting the strongest rise in prices for nearly seven years. Suppliers are hiking prices in response to surging demand, while tariffs and higher oil prices are also exerting upward pressure on costs. With the average price of goods leaving factories rising at the fastest rate since 2011, consumer price inflation looks set to accelerate.” This assessment is significant since there is a fairly high correlation between prices paid in the HIS Markit manufacturing survey and PCE inflation (Chart above). This suggests that the Fed’s preferred inflation gauge will likely rise above 2.0% in coming months. The last time inflation pressures were this strong in the ISM and HIS surveys was in 2011 and the PCE exceeded 2.2%.

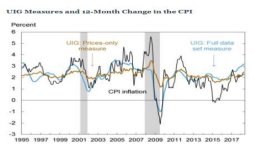

The Federal Reserve of New York’s Underlying Inflation Gauge (UIG) rose from 3.15% in March to 3.20% in April. The UIG combines 105 separate indicators so it is broad based. Although the increase of .05% in April doesn’t sound like much, the UIG is now higher than it was in 2011. The UIG confirms that the creep higher in inflation is widespread and a reflection that inflation pressures are building throughout the economy.

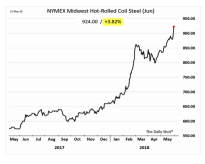

This analysis suggests that the odds are high that PCE inflation will breach 2.0% and move higher during the next 3 to 6 months based on ongoing economic growth and inflation pressures. Obviously, if a trade war develops economic growth could slow, and probably force the Fed to postpone additional rate hikes so the FOMC can assess the full impact. However, a trade war could exacerbate inflationary pressures as tariffs result in higher prices which are already evident in the price of steel. The political situation in Italy could also cause the Fed to pause if Italian bank’s solvency is questioned, since Italian banks still hold $300 billion in nonperforming loans. Deutsche Bank is the fourth largest bank in Europe and its stock has lost 45% of its value since the end of January. Clearly, the unwinding of such a large bank has the potential to become a contagion in the European banking system. However, if all of these issues are resolved without any economic disruption to the U.S’s and Europe’s economy, the path of least resistance for rates is up. Let’s see if technical analysis can offer any insight or guidance.

Treasury Bonds Yields

Most economists, strategists, and financial advisors rely almost exclusively on fundamental analysis, which focuses on the economy, interest rates, and estimates for corporate earnings. Technical analysis utilizes measures of price momentum, moving averages, and chart pattern analysis of major markets. I believe the combination of both disciplines is better, since each provides a different perspective, which is why my approach combines both fundamental analysis and technical analysis. As discussed the reduction of slack in the labor market and production capacity has laid the foundation for inflationary pressures to continue to build as economic growth improves in response to fiscal stimulus. Despite the numerous signs of mounting inflation, the level of complacency is quite high as most economists and strategists expect technology and demographics to keep inflation in check. Longer term, artificial intelligence and baby boomers being replaced by lower paid younger workers will exert downward pressure on wage growth and inflation. However, the cyclical forces currently at work can outweigh longer term factors in the next twelve months, and have the potential to push inflation higher than expected and thus force the Federal Reserve to stick to its projection of rate increases in 2018 and 2019.

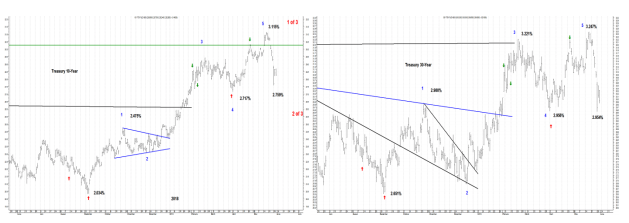

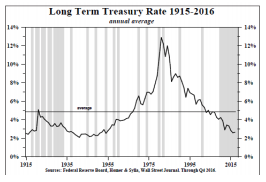

The 10-year Treasury yield peaked in September 1981 at 15.70% and continued to set lower highs and lower lows for the next 35 years. Before posting a low of 1.33% in July 2016, the 10-year yield recorded a high of 3.03% in December 2013. On May 17, 2018 the 10-year yield reached 3.115% after posting a higher low of 2.03% last September. For the first time since September 1981, the 10-year yield has made a higher low of 2.03% in September 2017 and a higher high of 3.115% in May 2018. The odds have now increased that the secular bull market in Treasury bonds ended in July 2016 and a new secular bear commenced. The prior secular bear market began in April 1946 with the yield on the 10-year bottoming at 2.08%. Who could have imagined that 35 years later it would top at 15.70% and then be followed by a 35 year secular bull market that would bring the 10-year yield down to 1.33%!

If a new secular bear market in Treasury bonds began in July 2016, interest rates will work higher in coming years and probably the next two decades. The pattern of higher highs and higher lows is supportive of the bear market thesis, as is the price pattern in the 10-year yield. Generally, the major trend in any market is accompanied by strong directional movement in prices, or yields in the case of Treasury yields. The strong directional movement is notated with wave 1 up, wave 2 down, wave 3 strongly up, wave 4 down, and wave 5 up. Corrections against the major trend begin after 5 waves have been completed and are usually choppy.

Since the low in July 2016, the directional movement in yields has been clearly up, while the correction (decline in yields) from the high in March 2017 to September was quite choppy. The initial move up from 1.336% to the March 2017 high was dynamic and directional, and would be labeled as wave 1 of the new bear market (Chart above - red 1). The decline to 2.034% in September 2017 was quite choppy and typical of a correction and would be labeled wave 2 (red 2). The longest and most directional wave is usually wave 3 within the 5 wave pattern. This was clearly the case between the low in September 2016 and December 2016 (wave 3 in blue), as well as the move higher from the low in November 2017 (wave 2 in blue) and the high near the end of February 2018 (wave 3 in blue). The wave 4 correction in blue brought the 10-year yield down to 2.717%, which was followed by wave 5 which pushed the yield up to 3.115% on May 17. Within the bear market thesis, the increase in the 10-year yield from 2.034% to 3.115% is wave 1 of wave 3 (red 1 of 3), and the current decline would be wave 2 within wave 3 (red 2 of 3). After wave of 2 of 3 is complete, wave 3 of 3 should lift the 10-year Treasury yield by more than the 1.081% of wave 1 of 3 and comfortably above 4.0%. Although it won’t be very comforting to the bond market or stock market if this occurs.

The correction for wave 2 (in red) lasted from March 10, 2017 until September 7, 2017 or almost 6 months. This suggests that wave 2 of 3 (in red) will likely last at least 2 to 3 months and implies that the 10-year Treasury yield could chop around between 2.65% and 2.96% for weeks. This view is supported by the high level of bearish sentiment toward Treasury bonds and the positioning in Treasury futures, which show hedge funds and trend followers have amassed a very large short position.

The move up from the low on July 6, 2016 until the high on March 10, 2017 took just over nine months, as did the tick up in yields from the low of 2.034% on September 7, 2017 to the high on May 17, 2018. The similarity in time is interesting as is the length of each move higher. Wave 1 brought the 10-year yield up by 1.285% (2.621% - 1.336%), but the recent rally in yield only rose by 1.081% (3.115% - 2.034%) which is far shorter. As noted, the longest and most directional wave is usually wave 3 within the 5 wave pattern, which is why it is either wave 1 of 3 since it is shorter, or something else.

Since the major trend in any market is accompanied by strong directional movement in prices in 5 waves, or yields in the case of Treasury yields, the move higher from the July 2016 low is only 3 big waves so far. This opens the door to a different interpretation as long as the high yield of 3.115% is not exceeded materially. The 3 wave increase in yield from the July 2016 low to the May 2018 high could be labeled an A-B-C (red A, B, C chart above), which suggests that the secular bull market in bonds may not be over. If this is the case, the yield could be expected to fall significantly in coming months in a down up down pattern. The rally from 1.33% to 3.11% was 1.78% so a 38.2% retracement would target a low near 2.43% while a 50% retracement would target 2.22%.

Although the fundamentals – economic growth, inflation outlook – support higher yields, the sentiment, positioning, equality of time within the move up in the yield, and the fact that the second move up was shorter than the first increase in yield are all supportive of the A-B-C pattern and a larger decline in yields in coming months. Realistically, though it will take a meaningful slowdown in the economy or an event to enable the 10-year yield to fall to 2.43% or 2.22%.

While the economic fundamental picture is healthy in the U.S., Italy could become a broader risk for the European economy and Deutsche Bank could unsettle the global banking system. Tensions in the Middle East are persistently rising under the radar, but could conflict erupt between Iran, Israel, or Saudi Arabia. The last two major bear markets in equities were initiated in the U.S. with the dot.com bubble and financial crisis. The next bear market in equities is likely to be triggered by events outside the U.S.

Debt Here, Debt There, Debt Everywhere

The current recovery, which began in June 2009, is the second longest on record, passing the 9 year mark (108 months) at the end of May. It would become the longest ever (121 months) if it stretched through July 2019. In its annual 10-year projection of GDP growth, government spending, budget deficits, and total federal debt, the nonpartisan Congressional Budget Office (CBO) assumes there will not be a recession until after 2028. Anyone willing to assume that outcome has never heard the alternative definition for assume – Ass – U – Me, which is definitely appropriate in this case. If a recession does materialize, the projections for GDP growth will be too high, budget deficits too low, as well as the estimates for total federal debt. Even if a recession is avoided, GDP growth is expected to be less than 2.0% annually in the nine years between 2020 and 2028.

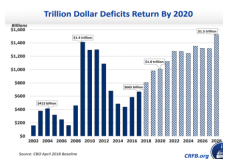

The CBO’s estimates the annual budget deficit will exceed $1 trillion in 2020 and never look back. The net result is that total federal debt will rise significantly during a period of consistent economic growth. Imagine how large the annual budget deficit could be during even a modest recession ($2 trillion?) and how much federal debt would pile up debt during the next decade.

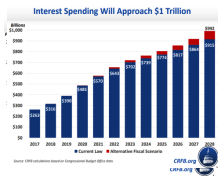

The alternative fiscal scenario was calculated by the Committee for a Responsible Federal Budget and projects that federal debt could be 192% of GDP in 2048 compared to 148% estimated by the CBO. If the CBO estimates are in the ballpark, the supply of Treasury bonds (in excess of $1 trillion annually) could require higher interest rates to generate the level of demand needed to absorb so much paper. The avalanche of coming supply during the next decade is supportive of the secular bear market in Treasury bonds and higher interest rates. Interest expense will consume an ever larger portion of the federal budget, even if the CBO’s expectation that the U.S. will remain recession free until after 2028 proves accurate. Spending on interest could easily crowd out spending for many other programs or require much higher taxes to sustain them.

If the 10-year Treasury yield climbs to near 4%, it won’t be a question of if there will be a recession, but when. I expect the Federal Reserve to launch a new round of Quantitative Easing to prevent yields from climbing too much and to keep the increase in interest expense in check. The Federal Reserve annually remits to the Treasury the interest it collects on the Treasury bonds it holds. In 2017, the Federal Reserve collected $113.6 billion in interest, paid banks $25.8 billion for holding reserves at the Fed, and paid the Treasury $80.7 billion. The Fed’s remittance lowered the cost of net interest expense in the 2017 budget from $263 billion to $182.3 billion. The amount of this annual remittance will fall as the Fed shrinks its balance sheet. However, during the next recession, the Fed’s balance sheet could easily balloon to $10 trillion or more, as it attempts to prevent an outright deflationary debt collapse. The debt issued to support the economy and purchased by the Fed amounts to free money for the government, as the Fed remits the interest it collects back to the Treasury. With a slight alteration to the Dire Straits song Money for Nothing, the lyrics wiould be: “That’s the way you do it. Money for nothing, get your programs funded for free.” Bernie Sanders and Elizabeth Warren would be happy to sing that tune!

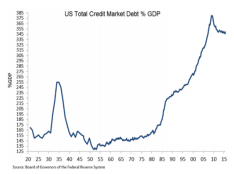

Total Credit Market Debt (TCMD) includes government debt, household debt, and corporate debt, so it provides an overview of the level of indebtedness for the U.S. economy as a whole, especially when it is compared to Gross Domestic Product. When interest rates peaked in September 1981, TCMD was roughly 163% of GDP. During the past 37 years it has ballooned as consumers took on more debt (mortgage debt, auto loans, and credit card debt), while the U.S. government made deficit spending a national pastime, and corporations piled on debt in their pursuit of maximizing shareholder value. At the end of 2017 TCMD was hovering just under 350%, which means for each $1 of GDP the U.S. is servicing $3.47 of debt. The huge increase in debt funded demand for goods and services lifting GDP in the process. However, average annual growth in the 1980’s and 1990’s was no better than in the 1970’s, and was far weaker in the ten years after 2000 as the toll of the financial crisis impaired growth. Although the increase in debt as a percent of GDP since 1981 supported GDP growth, it really didn’t boost growth to new heights. And now we have to pay for it. This is going to be very difficult especially if annual growth is less than 2% as forecast by the CBO after 2020. The excessive burden of carrying $3.47 of debt for $1 of GDP will become progressively heavier as interest rate rise. This suggests it won’t take as large of a rise in interest rates to curb growth as the cost of servicing the mountain of debt increases. This suggests that even if a secular bear market in bonds began in July 2016, interest rates won’t rise anywhere near as much as in the 1946 – 1981 secular bear market.

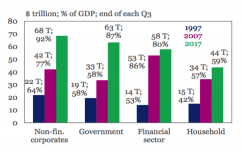

The U.S. is not alone in having a high debt to GDP ratio. According to the Institute of International Finance (IIF), global debt rose to a record of $233 trillion in the third quarter of 2017. Since 1997 global debt as percent of GDP has climbed from 217% to 318% in 2017, and up from 278% in 2007. Debt levels are up since 2007 but global GDP growth is noticeably slower. According to the International Monetary Fund (IMF), global growth clocked in at 5.6% in 2007 and is projected to grow 3.9% in 2018. Growth was 43% faster in 2007 than in 2018, but global debt levels are 40% higher. This is not a good combination and indicates that the global economy is on a weaker foundation than in 2007. Any meaningful slowdown in global GDP growth could result in a spike in debt defaults and another financial crisis that could prove more difficult for central banks to manage. Interest rates are far lower than in 2007 so the stimulus from lowering them won’t be as effective as it was after the financial crisis. Government debt has climbed from 58% in 2007 to 87% of global GDP in 2017, so governments will be hampered in running large budget deficits to cushion the social dislocations from a recession. I have no doubt that politicians around the world will try to spend and central banks will launch more Quantitative Easing programs to combat the next global recession. The $64 question is whether financial markets will have the same confidence in the ability of central banks to adequately manage a bigger problem with less ammunition and no bazooka. Initially markets will due to the relative success after the financial crisis. But a healthy degree of skepticism will be warranted.

The Italian Dilemma

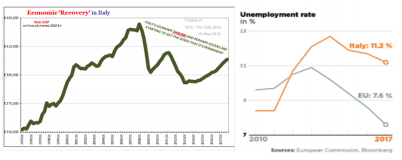

In the 72 years since World War II, Italy has had 66 governments or one every 1.1 years. The new government is composed of the left wing populist 5 Star Movement and the far right wing League. The U.S. domestic equivalent would be Bernie Sanders followers joining arms with members of the Tea Party. There is a good chance the new government in Italy won’t even make it a full year, but in the short run the goals of each group could prove unsettling for Europe. The 5 Star Movement wants Italy to adopt a guaranteed income of around $900, while the League wants to cut taxes. The net result could increase Italy’s annual budget deficit by $150 billion and well above 3% of GDP, which is against EU rules. Both groups avocally criticize Brussels for its ‘imperialism’, and would like to see Italy receive almost $300 billion in debt forgiveness. Both groups tapped into a reservoir of economic discontent since Italy’s economy has shrunk by 7% since 2007 despite the ‘recovery’. The unemployment rate is 11.2% compared to 7.6% for the European Union. The unemployment rate for Italian young workers is 31.7%, more than double the 15.6% average for the EU. Only Greece (42.3%) and Spain (35%) have a higher rate. Most revolutions begin with the disenfranchisement of the young, who have the time to participate in marches and the energy to persist.

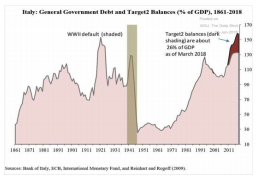

The goals of the two groups are colliding with the Italy’s hard fiscal reality. Italy’s debt as a percent of GDP is 131.8% compared to an EU average of 83.1%. Since Italy’s central bank’s debts (Target2 balances) must be added to those of the general government, the real debt to GDP ratio is 158%. There is virtually no chance that Italy will be able to grow sufficiently to repay its debt, leaving restructuring as the only viable option since default is out of the question. The restructuring of Italy’s debt is likely to go as smoothly as the negotiations went with Greece’s restructuring, which raises the potential of a sovereign debt crisis redux. Italy is the third largest economy in the European Union and the fourth biggest bond market in the world. Italy is truly too big to fail. Italy presents a dilemma with no easy solution. The only question is whether the new government has the capacity to truly challenge the authority of the EU and trigger the threat of another crisis.

Dollar

In the March Macro Tides I expected the Dollar to rally and provided an upside target. “The Dollar chart suggests a rally to near 95.00 is possible in coming months. This would represent an increase of almost 8.0% from its low at 88.25. A Dollar rally of this magnitude could prove a headwind for U.S. stocks, some commodities, and Emerging Markets, especially if Treasury rates breakout before Labor Day.” On May 29 the Dollar reached 95.02. The Dollar is likely to push to a modest new high after a modest correction of 1.5% or so. The rally in the Dollar has benefited small cap stocks since they are far less affected by Dollar strength compared to large cap stocks. Although the Russell 2000 has made a new all time high, the S&P 500 is 4.3% below its prior peak and the DJIA is 6.8% below its January high. By their nature small cap stocks are more volatile than large cap stocks, so the embracement of them is a sign of complacency and speculation, suggesting a correction is not far off. Emerging Markets have been pressured by the rally in the Dollar and higher interest rates.

Emerging Markets

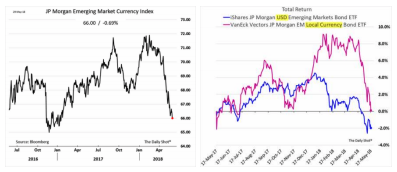

After bottoming in the first quarter I expected the Dollar to rally and Treasury yields to exceed their 2017 highs. This combination was expected to be a negative for Emerging Markets as noted in the March Macro Tides. “The 12 combination of higher interest rates in the U.S. and a stronger Dollar could prove a heavy burden on the $10 trillion of EM debt denominated in Dollars between now and Labor Day.” As would be expected during a period of Dollar strength, EM currencies have slumped by more than -8% since February. This weakness also caused EM Dollar denominated bonds to fall -7.5% and EM bonds in local currencies to lose more than -11.5%.

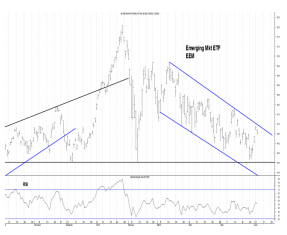

Emerging Market equities as measured by the Emerging Market ETF (EEM) is down -7.2% since its mid march high, and did test its February low of $45.00 as forecast in the March Macro Tides (black horizontal line). “Money flows into EM soared in January before the markets got clipped. The inflow suggests a bit too much enthusiasm and leaves EM funds vulnerable. A retest of the February low near $45.00 on the Emerging Market ETF (EEM) is possible.” Since its high in March EEM has made a series of lower highs and lower lows, which is the definition of a downtrend. If the U.S. equity market corrects in the third quarter as expected, EEM could trade under $45.00.

Gold

With the Dollar rallying, Gold fell below $1306 as anticipated in the May Macro Tides. “If the Dollar moves toward 94.50 in coming weeks/months, Gold has the potential to close below $1306 and decline to $1275 and potentially $1250.” After closing below $1306 Gold fell to $1282.20 on May 21. Bullish sentiment remains low but Large Speculators did increase their long position when Gold traded above $1300 in the last week of May. This increase suggests Gold may need even more time before a sustainable rally is capable of taking hold and lifting Gold above the heavy duty resistance at $1368. I continue to expect Gold to rally to $1318 - $1325 in the short term. If Gold is able to overcome this resistance, the next target would be $1360 - $1370.

Gold didn’t establish a solid trading low in December 2017, until Gold broke below the higher dashed trend line (chart below). This was an important trend line since it connected the significant low in December 2016 with the next important low in July 2017 that preceded the rally from $1205 to $1357 in September 2017. Gold may break below the solid trend line connecting the December 2016 low and December 2017 low in order to shake out the last remaining bulls. If Gold breaks below the solid trend line, a quick drop to $1250 may follow and set up a great buying opportunity.

I still expect Gold to rally above $1400 before year end. Inflation could be the spark if wage growth exceeds 3.0%, or tariffs lift prices more broadly, as steel prices have risen by 45% since January.

Gold Stocks

If Gold trades up to $1320, the Gold stock ETF GDX may rally up to $23.30 - $23.60 in the next few weeks. If GDX’s relative strength to Gold doesn’t improve significantly during the next rally and GDX’s RSI nears 70, selling into that strength could prove a good idea. If Gold drops to $1262 or lower, GDX could easily drop below $21.75 and possibly down to $21.30. A good buying opportunity could develop if GDX’s RSI falls below 32. The Weekly Technical Review will try to monitor which course seems more likely.

Stocks

In a finely tuned car all the pistons work together, especially when the car is accelerating. If one or more of the pistons begin to misfire, engine trouble soon develops and the car will need to be repaired by a mechanic. When all the major averages are not in sync, the trend in the stock market is often nearing a change. The Russell 2000 has posted a new high and probably will be joined by the Nasdaq 100 shortly. The FAANG stocks represent 38.3% of the Nasdaq 100 and 12.5% of the S&P 500. Incredibly, the bottom 250 stocks in the S&P 500 only comprise 13.1% of the index. The 5 stocks in FAANG effectively neutralize the contribution of the 250 smallest stocks to the performance of the S&P 500. Despite the strong performance of the FAANG stocks, which have outperformed the S&P 500 by 30% over the past year, the S&P 500 is 4.3% below its January peak. It is certainly possible that the S&P 500 and the DJIA will play catch up and also make a new high. The odds though don’t favor that outcome.

The strongest major average has been the Russell 2000 but it appears to finishing a 5 wave advance from the low on May 1. Although it has been making a new high, its RSI has been making lower highs (red line). This is an indication that upside momentum is waning and is often a precursor to at least a modest pullback. I expect the Nasdaq 100 (QQQ) to make a new high soon and potentially complete a 5 wave advance from the low on May 3 as it does so.

The S&P 500 has so far failed to exceed the blue trend line which extends back to the April 2016 high, despite all the support it has received from the FAANG stocks. The 21 Day Net of Advances - Declines has reached a level that has coincided with recent price highs in the S&P 500 (red arrows). Based on mathematical relationships discussed in the June 4 WTR, the S&P 500 has the potential to register a high between 2750 – 2758 soon. The market will likely hold up for a bit more as the Russell 2000 and the Nasdaq 100 finish wave 5, but the upside seems limited for the broad market.

Jim Welsh

@JimWelshMacro

[email protected]

© Macro Tides

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All