With the economy in the later stages of its post-crisis recovery, we believe investors should be cautious and selective on corporate credit. Within the high yield sector, this caution may warrant a move up in quality toward the higher end of the spectrum: BB rated bonds. Historically, many high yield investors have been underweight BB rated bonds, presumably to seek greater value and higher returns in the more idiosyncratic universe of single B rated issuers. Indeed, BBs have underperformed other parts of the high yield market year-to-date (as of 31 May) on both total return and spread, and a selective, bottom-up approach remains crucial. But with BB spreads at relatively attractive levels today amid a more supportive technical and fundamental picture, we believe it’s time to reconsider this overlooked area of high yield credit.

Attractive valuations in BB

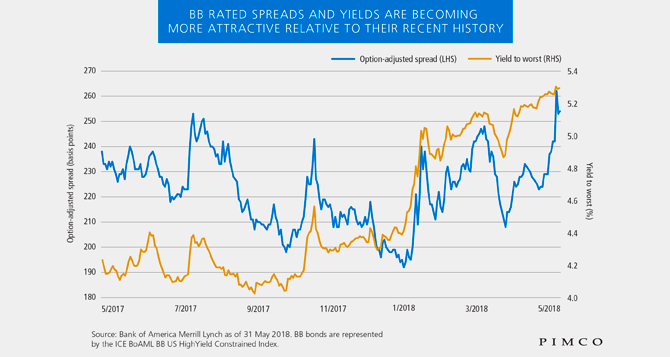

High yield bonds have been resilient in 2018 despite significant mutual fund outflows and an increase in U.S. Treasury yields. However, at the end of May U.S. BB spreads (and yields) were at their widest in 12 months (see chart). BBs have also underperformed Bs and CCCs over the same period, according to ICE Bank of America Merrill Lynch index data, partly as a result of their higher duration and partly due to investors moving down the quality spectrum in search of higher yields against a backdrop of rising rates.

We think BBs may reverse this underperformance if investors believe, as PIMCO does, that Treasuries will remain somewhat range-bound after the recent sell-off.

Improving fundamentals

Credit fundamentals in the U.S. are generally improving, driven by faster economic growth and higher corporate earnings. Net leverage for BB rated issuers has been declining and now lies below its long-term average, according to Barclays Research, with further improvements likely as issuers deleverage in response to recent U.S. legislative changes limiting the tax deductibility of debt. (Net leverage is calculated as net debt divided by EBITDA – earnings before interest, taxes, depreciation and amortization.)

Furthermore, since 2016 BB bonds have realized a 0% default rate, according to J.P. Morgan (bonds as rated 12 months prior to default). In light of the improving fundamentals we believe defaults are likely to stay at or near this level for a while, meaning BBs offer an attractive yield opportunity on a loss-adjusted basis.

Supportive technical factors

The improvements in fundamentals, buoyed by a stronger macroeconomic backdrop and a recovery in commodity prices from their lows in late 2015 / early 2016, have led to an increase in “rising stars” (issuers upgraded into investment grade) and a decrease in “fallen angels” (issuers downgraded to high yield) across the U.S. credit market.

In the first four months of this year, the volume of outstanding bonds from rising stars exiting high yield indexes exceeded that from fallen angels by over $20 billion and estimates suggest that the year-end total could reach approximately $70 billion, according to Bank of America Merrill Lynch. Historically, upgrades have resulted in a positive technical (i.e., spread compression) as bonds enter much larger, and more widely followed, investment grade indexes. Further technical upside is possible due to mergers and acquisitions in sectors such as telecoms and homebuilders; with many BB bonds now trading below par, the triggering of change-of-control clauses can lead to a takeout at par or above, creating capital appreciation opportunities.

The case for BBs

In summary, we believe the recent underperformance of BB bonds has largely been the result of their higher duration and the overall rise in bond yields since the beginning of the year, in addition to investors’ more aggressive search for yield down the quality spectrum. Yet corporate credit markets have historically been prone to overshooting in response to shocks both small and large. Given a positive fundamental and technical backdrop and in light of our New Neutral framework anchoring yields, we see a tactical opportunity to move up in quality into BBs. Via careful credit selection through bottom-up ideas, and an emphasis on “bend but don’t break” positions with a low likelihood of default, investors may earn attractive, relatively resilient yield with proportionately reduced default risk.

Read “Understanding High Yield Bonds” for a quick refresher on this credit sector.

Hozef Arif is a portfolio manager in Newport Beach, focusing on global high yield and crossover corporate credit portfolios. Matthew Livas is a credit product strategist in London.

DISCLOSURES

Past performance is not a guarantee or a reliable indicator of future results. Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and the current low interest rate environment increases this risk. Current reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed. High yield, lower-rated securities involve greater risk than higher-rated securities; portfolios that invest in them may be subject to greater levels of credit and liquidity risk than portfolios that do not.

The credit quality of a particular security or group of securities does not ensure the stability or safety of the overall portfolio. Statements concerning financial market trends are based on current market conditions, which will fluctuate. There is no guarantee that these investment strategies will work under all market conditions or are suitable for all investors and each investor should evaluate their ability to invest long-term, especially during periods of downturn in the market. Investors should consult their investment professional prior to making an investment decision.

© PIMCO

© PIMCO

Read more commentaries by PIMCO