Templeton Global Macro makes a compelling case that finding attractive opportunities in emerging markets lies in distinguishing the more resilient countries from the rest. Here, CIO Michael Hasenstab provides an update of the team’s proprietary “Local Markets Resiliency Index” and highlights the scores of seven different countries—Argentina, Brazil, India, Indonesia, Mexico, Malaysia and South Africa.

In June 2016, we released Global Macro Shifts1 (issue 5)—Emerging Markets: Mapping the Opportunities [GMS-5]. This paper discussed many of the risks and opportunities across emerging markets while highlighting the importance of assessing economic resiliencies in individual countries.

Since then, we have seen notable rallies in emerging economies as capital has returned to a number of undervalued markets, particularly during 2017. Those trends can continue, in our view, particularly in specific countries that have made strides in fortifying their economies against potential trade shocks, commodity price shocks and exchange rate shocks.

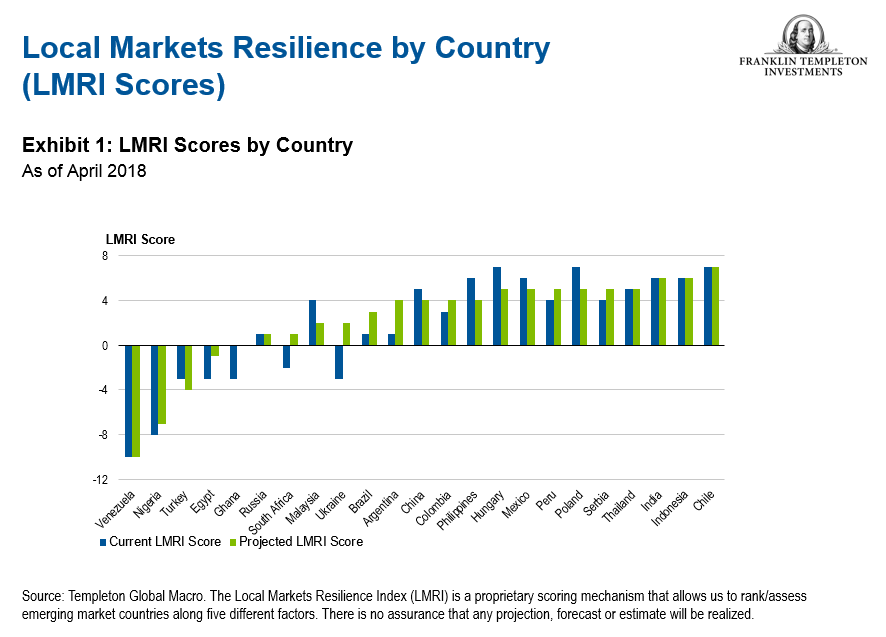

In GMS-5, we introduced our proprietary Local Markets Resilience Index (LMRI), which scores countries along five resilience factors. Given that macro conditions are in constant flux, we are continuously reviewing and updating our LMRI scores. In this research briefing, we provide an external update on our current and projected LMRI scores for 23 countries. We also provide a breakdown of the five factor scores along with brief analyst notes for five countries with high projected scores and two that have low projected scores.

Overall, we continue to have a positive outlook for a select set of emerging markets, but it’s important to recognize that there are significant variations across the asset class. Thus, it’s critical to sort the stronger, more resilient economies from the weaker, more vulnerable ones, in our view. The LMRI scores illustrate aspects of our research process that aim to identify those more resilient economies and the concomitant longer-term investment opportunities that they may provide.

The Five Critical Factors of the LMRI

1 | Policy mix

Focuses on the quality of macroeconomic policymaking, from an institutional and capacity-to-implement perspective, taking into account the broader enabling political environment. A well-functioning government and parliament, fiscal rules and a highly independent central bank improve the policy mix, as does the political ability to push through needed changes.

2 | Lessons learned

From their experience of past crises, evaluates the extent to which the country has learned lessons from previous crises or episodes of mismanagement of the economy, reevaluating the sustainability of its growth model and assessing financial fragilities.

3 | Structural reforms

The legal and institutional changes that improve productivity and economic growth, determining the ability of a country to enhance its institutions and productive capacity to drive sustainable economic growth. An extended period when high commodity prices and indiscriminate capital flows could compensate for economic mismanagement is unlikely to return soon. Over the long term, there is no substitute for the hard steps necessary to diversify economic structures, upgrade infrastructure, improve the business environment, facilitate innovation and invest in high-quality education. Specific structural reforms could relate to areas such as the governance of state-owned enterprises, labor laws, the energy sector and corruption.

4 | Domestic demand

Captures the ability of a country to grow on its own, abstracting from external factors. A small, open economy is highly dependent on the rest of the world. By contrast, a large economy has the efficiency of scale, the gravity to attract investment and the ability to generate growth independently from the rest of the world. Other factors that determine domestic demand include demographic factors such as population growth and the age of the population; inflation; and wages and employment growth. Overstimulation of domestic demand runs the risk of overheating and hence reduces the score. Given the heightened degree of uncertainty in the global environment, we expect economies that are comparatively insulated from global forces and with healthy domestic demand to outdo their peers.

5 | External vulnerabilities

Captures the traditional exposure to external shocks and the risk of a balance of payments crisis or capital flight. Such indicators include the current account, external debt and commodity dependence. In some countries, a substantial part of external debt is owed by companies to their foreign parent companies, and this is not regarded as a source of risk. “External vulnerabilities” are, in a sense, a different side of the same coin as “domestic demand.” They capture the same idea that in a very volatile global environment, some degree of insulation from external shock is likely to prove especially valuable.

The Scoring Process for the LMRI

For each factor, we separately assess both current and projected conditions, so as to gauge the degree of risk along the investment horizon. We aggregate the five individual category scores to obtain an overall country score—the LMRI score. The scoring along each category is necessarily based to an important extent on our subjective judgment; nonetheless, we believe it provides a strong rigor in assessing and comparing different markets in a way that allows us to assess the true underlying risk and to identify attractive opportunities where our score deviates significantly from the risk assessment implicit in market prices.

The rating of countries is based on the five criteria, described above. Each criterion is assigned a value between -2 and +2 for the current situation, and similarly a value for the projected outlook, in the views of the team. Exhibit 1 shows the results of our ranking system for the selected subset of EMs across the different regions.

Five Countries with High Projected LMRI Scores

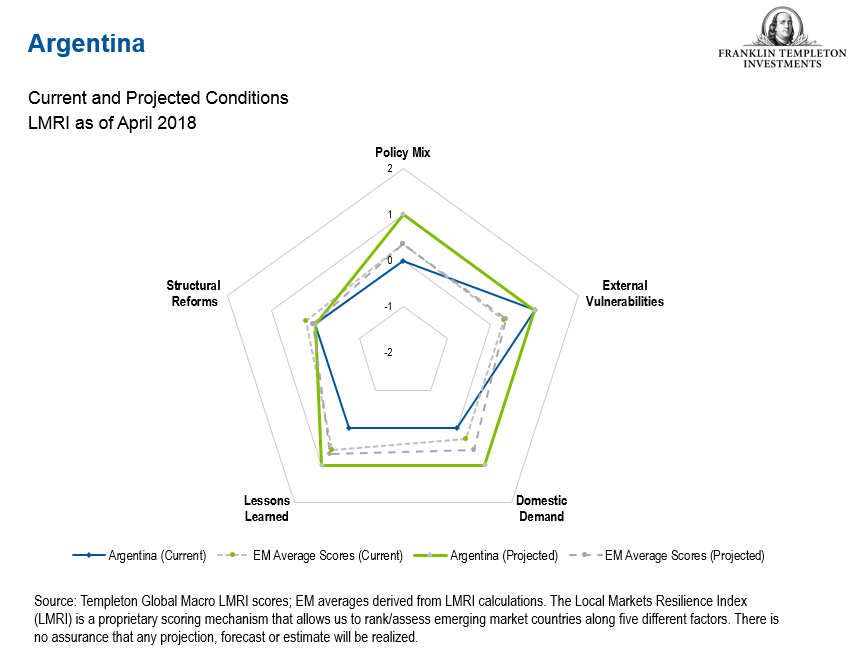

Argentina

(Overall LMRI Score, Current: +1; Projected: +4)

Short notes

- Inflation-targeting regime slowly taking hold. Inflation is declining but remains above target due to tariff adjustment.

- Reserves have rebounded strongly. Primary deficit declining. Exports are improving.

- Economic activity is rebounding, investment is increasing. High interest rates may temper business investment.

- Labor markets remain over-regulated.

- Structural reforms continue to see gradual impact, improving fiscal efficiency. Slow progress expected before the 2019 presidential election.

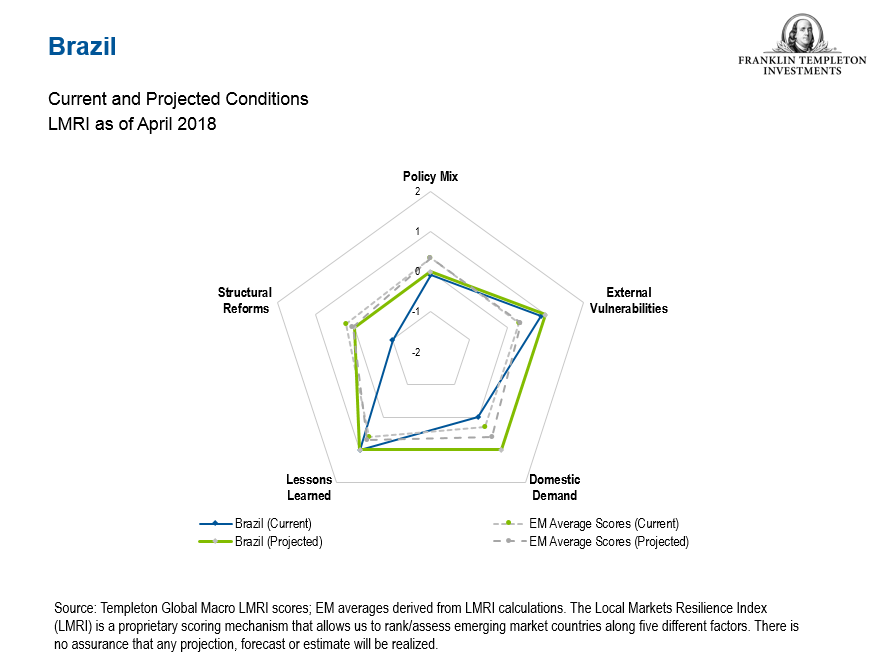

Brazil

(Overall LMRI Score, Current: +1; Projected: +3)

Short notes

- Fiscal deficit remains high, but relatively stable.

- October 2018 elections may increase policy risks.

- High foreign reserves appear more than sufficient to cover short-term external debt.

- Consumer and business confidence has gradually improved.

- Pension reform has been delayed by political disruptions.

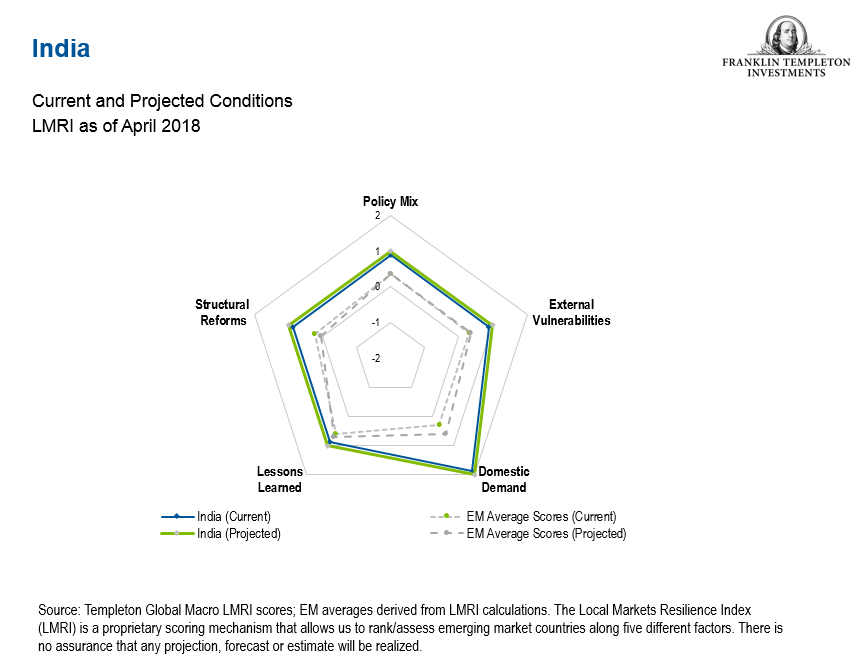

India

(Overall LMRI Score, Current: +6; Projected: +6)

Short notes

- Fiscal consolidation is in progress, but more needs to be done. Government debt is high but appears sustainable.

- Central bank independence appears secure, foreign exchange policy remains appropriate.

- Ample foreign reserves, low external debt.

- Domestically driven economy, low exports and young demographics.

- Several reforms in recent years but more reform needed for banking, labor and land issues.

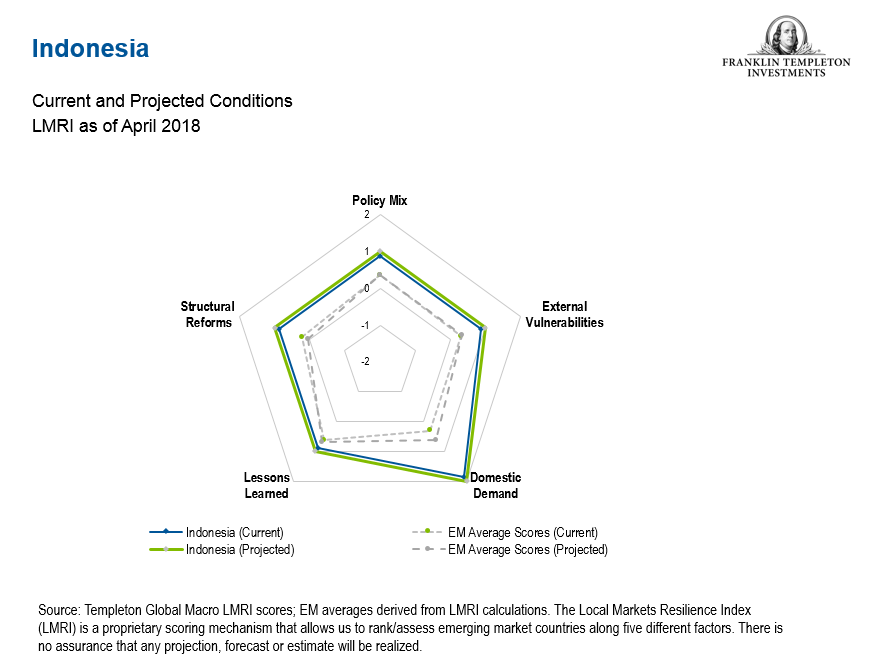

Indonesia

(Overall LMRI Score, Current: +6; Projected: +6)

Short notes

- The fiscal deficit cap is in place and government debt remains low.

- High level of foreign reserves with a narrow current account deficit and strong financial inflows.

- Domestically driven economy that is relatively shielded from regional trade tensions.

- Flexible exchange rates and strong central bank independence.

- Government appears committed to improving business environment and fiscal management.

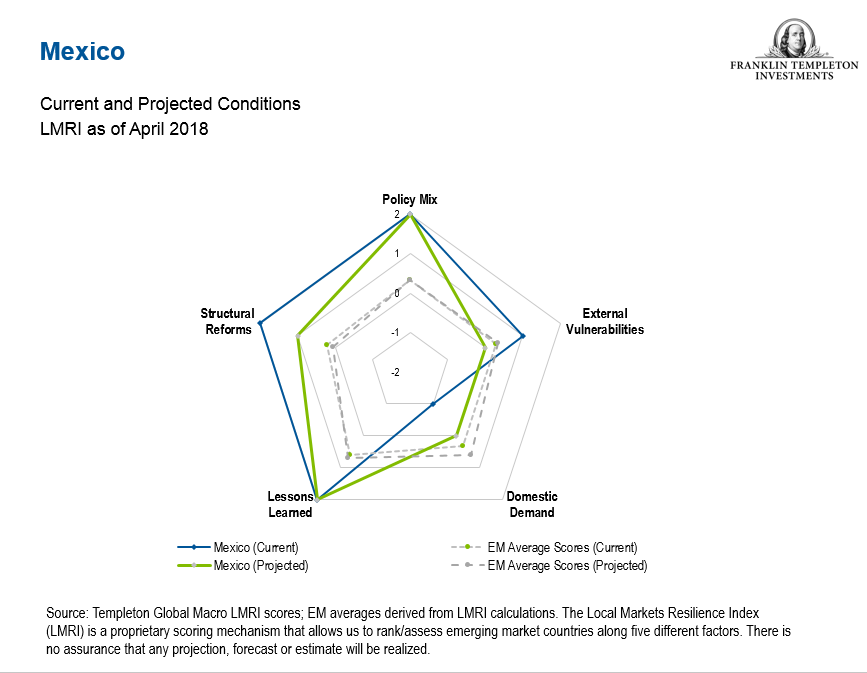

Mexico

(Overall LMRI Score, Current: +6; Projected: +5)

Short notes

- Recent fiscal consolidation with primary balance in surplus in 2017. Central bank is orthodox and independent.

- Several sector reforms since 2012, but July 2018 elections may increase policy risks.

- Export sector is manufacturing-based and predominantly linked to the US; free-trade negotiations remain a risk.

- High foreign reserves with manageable current account deficit.

- Low unemployment, falling inflation, but moderating domestic demand.

Two Countries with Projected Low LMRI Scores

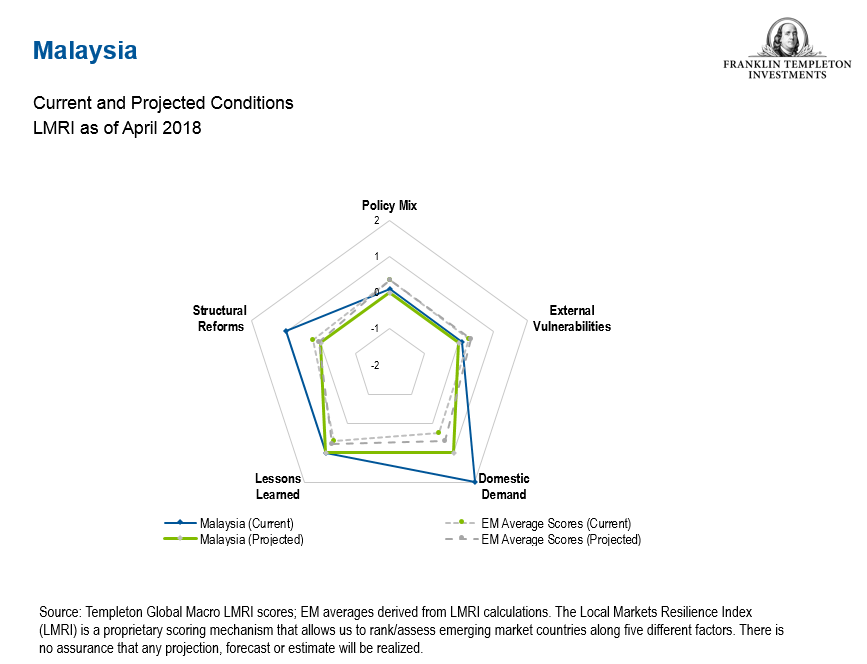

Malaysia

(Overall LMRI Score, Current: +4; Projected: +2)

Short notes

- Fiscal consolidation remains on track, but government’s growing unpopularity could slow structural reforms.

- Central bank confidence has weakened.

- Export sector is well-diversified between electronics and commodities, but is vulnerable to a slowdown in China.

- High household debt limits growth, though domestic demand is supported by demographics.

- Foreign reserves are high, the central bank has leaned toward exchange-rate intervention.

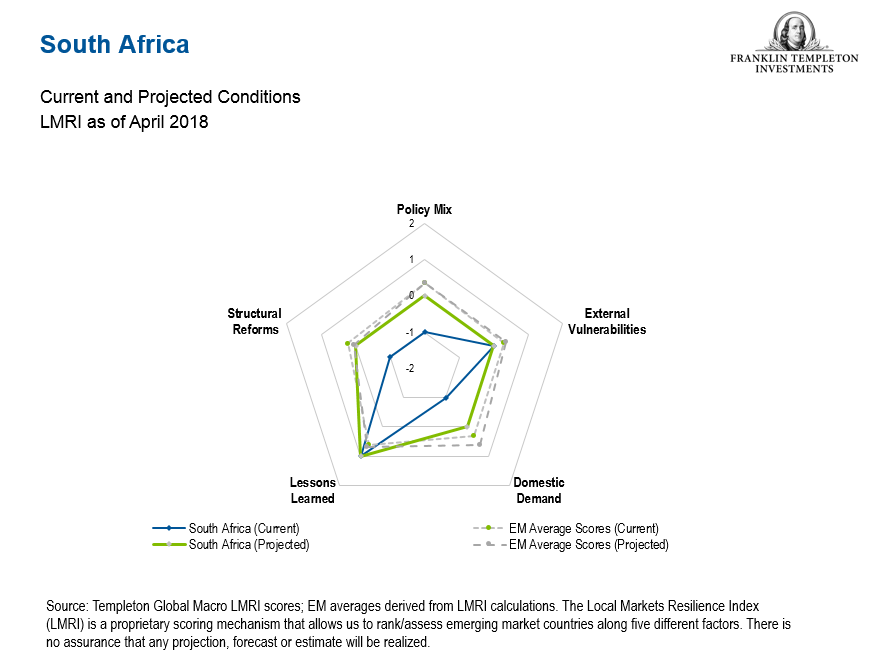

South Africa

(Overall LMRI Score, Current: -2; Projected: +1)

Short notes

- Fiscal deficit remains high, government raising taxes to fiscally consolidate.

- Ambitious transformation agenda may compromise fiscal efforts.

- Low foreign reserves and economy remains vulnerable to commodity prices.

- Domestic demand improving but remains weak. Tax hikes may suppress consumption.

- Independent central bank responding appropriately to inflation, while maintaining flexible exchange rate.

For more detail on the team’s LMRI scoring, read “Emerging Markets: Mapping the Opportunities” a research-based briefing on global economies featuring the analysis and views of Dr. Michael Hasenstab and senior members of Templeton Global Macro. Dr. Hasenstab and his team manage Templeton’s global bond strategies, including unconstrained fixed income, currency and global macro. This economic team, trained in some of the leading universities in the world, integrates global macroeconomic analysis with in-depth country research to help identify long-term imbalances that translate to investment opportunities.

The comments, opinions and analyses expressed herein are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. Because market and economic conditions are subject to rapid change, comments, opinions and analyses are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy.

This information is intended for US residents only.

What Are the Risks?

All investments involve risks, including possible loss of principal. Special risks are associated with foreign investing, including currency fluctuations, economic instability and political developments. Investments in emerging markets, of which frontier markets area subset, involve heightened risks related to the same factors, in addition to those associated with these markets’ smaller size, lesser liquidity and lack of established legal, political, business and social frameworks to support securities markets. Because these frameworks are typically even less developed in frontier markets, as well as various factors including the increased potential for extreme price volatility, illiquidity, trade barriers and exchange controls, the risks associated with emerging markets are magnified in frontier markets. Bond prices generally move in the opposite direction of interest rates. Thus, as prices of bonds in an investment portfolio adjust to a rise in interest rates, the value of the portfolio may decline.

_____________________________________

1. Global Macro Shifts is a research-based briefing on global economies featuring the analysis and views of Dr. Michael Hasenstab and senior members of Templeton Global Macro.

© Franklin Templeton Investments

© Franklin Templeton Investments

Read more commentaries by Franklin Templeton Investments