Rising interest rates and volatile markets can create headwinds for all types of investors. Franklin Equity Group’s Alan Muschott makes a case for convertible securities, a hybrid asset class that he thinks can adapt to various market conditions.

Amid expectations that US interest rate increases could accelerate, many fixed income investors in particular have asked for our view on the prospects for convertible securities. It’s an understandable concern as bonds tend to lose value when interest rates rise, and the Federal Reserve’s June projection called for a total of four increases in its benchmark interest rate this year.

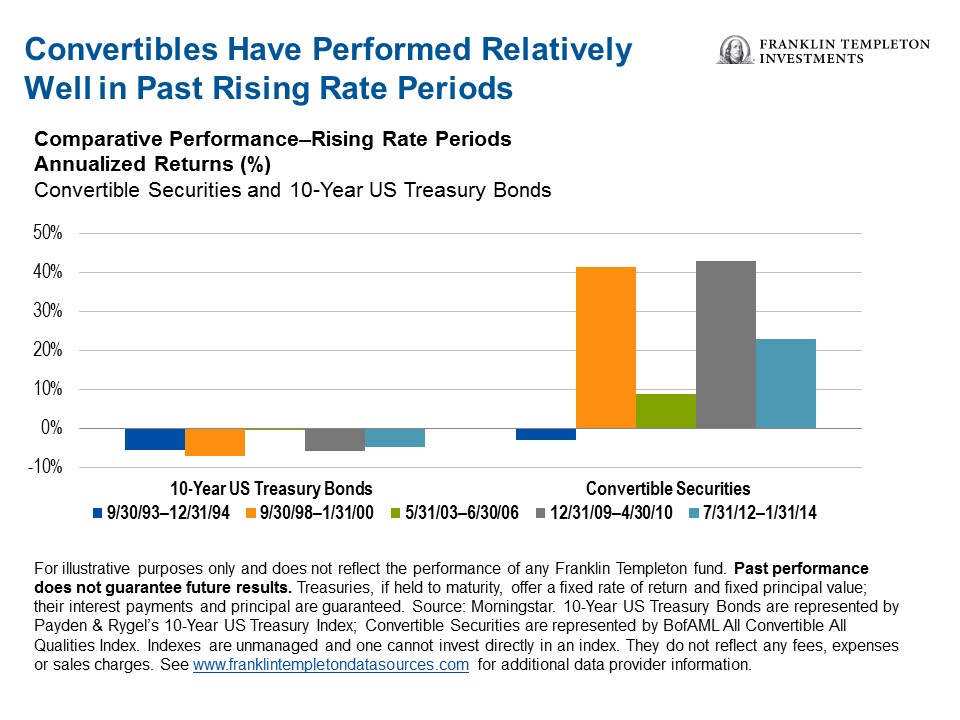

As the chart below shows, during prior periods of rising interest rates, convertibles have performed better than 10-year US Treasuries.1 Therefore, in a rising-rate environment, we think convertibles can be a favorable place for fixed income investors to be.

That said, it’s a bit incomplete to compare the performance of convertibles to other fixed income investments given their characteristics. Convertibles are a unique asset class, offering investors features associated with bonds and the growth potential of common stocks.

A Bit of Background

Convertibles are generally structured as a form of debt (bonds, debentures) or preferred shares with an embedded option that allows conversion into common shares under predetermined

conditions. That embedded conversion option provides capital appreciation when the underlying common stock rises.

In a rising-rate environment where interest rates are rising for the “right” reasons—for example, strong economic and corporate earnings growth—equities tend to perform well. If the underlying common stock in a convertible security rises with the market, it should also increase in value because of the conversion option.

Conversely, if the common stock doesn’t perform well, the debt features of the convertible—interest payments and claim on principal—may provide some support. In this respect, convertibles act similarly to bonds, with characteristics that can potentially offer less value erosion in declining markets than the underlying common stock.

Investment Implications

Given the run we’ve seen in the US equity market over the past few years, many investors may be concerned about stock valuations and their equity exposures. In this environment, some investors may want to consider select exposure to convertible securities.

For those seeking income and risk-managed equity exposure, convertibles can offer numerous potential benefits, including:

- An asymmetric upside/downside profile, with higher participation in the underlying stock’s appreciation than depreciation.

- Current income that is usually higher than a common stock’s dividend, albeit typically lower than yields on non-convertible debt.

- Additional diversification potential and an improved risk/reward profile in a portfolio due to imperfect or low correlations.

- A claim on the issuer’s assets senior to holders of common shares.

- Robust asset class: the convertibles market can be considered a separate asset class due to its size, distinct composition of the issuer base and a unique risk/return profile.

Looking at opportunities across sectors, we see technology as increasingly becoming a non-discretionary expense for a wide range of companies and industries. In particular, we like certain convertibles in growth themes, like on-demand software.2

The bottom line is we think it’s a good time for investors to reconsider allocating to select convertibles. We believe convertible securities’ ability to adapt to myriad market conditions makes the investment class an attractive vehicle for increasing a portfolio’s diversification.3

Four Good Reasons to Consider Investing in Convertible Securities

1. Current Income. Investors seeking yield from equity securities may find convertibles an appealing option, as they generally provide a more attractive income component than stocks alone (although generally lower than traditional bonds), while still allowing participation in the stock’s price movement.

2.Potential for Additional Diversification. Historically, convertibles typically have exhibited a low correlation to fixed income and demonstrated imperfect correlation with stocks. This creates the potential for an investor to help enhance portfolio diversification, dampen volatility and improve a portfolio’s overall risk profile. Note, diversification does not guarantee profit nor protect against risk of loss.

3. Attractive Potential for Long-Term Risk-Adjusted Returns. Critics point out that convertibles do not increase as rapidly in value as stocks during rising markets; nor does their downside protection equal that of bonds during market declines. Nevertheless, historically they have delivered attractive long-term risk-adjusted returns compared with both stocks and bonds.

4. Robust and Diverse Opportunity Set. The flexible nature of convertibles makes them appealing to a broad range of investors. As a group, convertibles have historically presented an attractive risk/reward profile, but within the group there is considerable variation in the level of risk, sensitivity to movements in the underlying stock, and upside participation potential. Convertible securities are diversified across credit ratings, sectors, market capitalization and investment characteristics.

The comments, opinions and analyses expressed herein are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. Because market and economic conditions are subject to rapid change, comments, opinions and analyses are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy.

This information is intended for US residents only.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

What Are the Risks?

All investments involve risks, including possible loss of principal. Generally, those offering potential for higher returns are accompanied by a higher degree of risk. Stock prices fluctuate, sometimes rapidly and dramatically, due to factors affecting individual companies, particular industries or sectors, or general market conditions. Investments in fast-growing industries like the technology sector (which historically has been volatile) could result in increased price fluctuation, especially over the short term. Bond prices generally move in the opposite direction of interest rates. Thus, as the prices of bonds in an investment portfolio adjust to a rise in interest rates, the value of a portfolio may decline. High yields reflect the higher credit risk associated with these lower-rated securities and, in some cases, the lower market prices for these instruments. Convertible securities are subject to the risks of stocks when the underlying stock price is high relative to the conversion price (because more of the security’s value resides in the conversion feature) and debt securities when the underlying stock price is low relative to the conversion price (because the conversion feature is less valuable). A convertible security is not as sensitive to interest rate changes as a similar non-convertible debt security, and generally has less potential for gain or loss than the underlying stock.

_________________________________________________________________________________

1. Past performance is no guarantee of future performance.

2. The technology industry can be significantly affected by obsolescence of existing technology, short product cycles, falling prices and profits, competition from new market entrants as well as general economic conditions.

3. Diversification does not guarantee profit nor protect against risk or loss.

4. Source: Morningstar. Correlation measures the degree to which two investments move in tandem. Correlation will range between 1 (perfect positive correlation where two items have historically moved in the same direction) and -1 (perfect negative correlation, where two items have historically moved in opposite directions). See www.franklintempletondatasources.com for additional data provider information.

© Franklin Templeton Investments

© Franklin Templeton Investments

Read more commentaries by Franklin Templeton Investments