During the second quarter the equity market as measured by the S&P 500 Index had a total return of 3.4%, bringing the year-to-date total return to 2.6%. Second quarter performance reflects the continued low-inflationary expansion of the U.S. economy and the attendant growth in corporate profits. All else being equal, we would expect these trends to persist. The question, of course, is whether “all else is equal.”

The biggest potential change facing the economy is the evolving rhetoric surrounding trade, the imposition of tariffs and retaliatory tariffs, and the potential for a wider trade war. At this point, it is impossible to predict whether our trade disputes will devolve into a full-blown trade war or, alternatively, if they will be resolved amicably and with potentially lower tariffs. A lot is at stake. So let us lay out best-case and worst-case scenarios.

The best-case scenario is that the administration’s bellicose trade rhetoric is simply a negotiating tactic and that all sides will ultimately work toward a fair-trade outcome that could entail even lower tariffs than those currently in place. This would allow the long economic recovery to extend further as inflation would likely remain in check and corporations could rationally plan their capital spending. This favorable outcome would likely drive the stock market higher.

The worst-case scenario is that U.S. imposed tariffs are not withdrawn, but expanded, causing our trading partners to impose increasingly higher retaliatory tariffs. This would have widespread repercussions, ultimately increasing inflation and slowing global growth. It would disrupt supply chains, which have grown increasingly complex in the global economy, and would almost certainly cause corporations to defer investment spending, which is finally on the mend. As with the best-case scenario, we do not think that the worst-case scenario is fully discounted by the stock market.

Given the very real uncertainty surrounding the trade issues and given the unpredictability of the outcome, we are pursuing the overriding goal of owning companies whose fundamental outlooks are more company-specific or idiosyncratic and less dependent on any particular trade outcome. As an example, we believe that digitization is increasing throughout the economy and will continue to do so whether we enjoy excellent or terrible trade relations with our partners. In order for digitization to grow, companies need sophisticated data centers. We own a company, Digital Realty Trust, which owns and operates data centers. It is a REIT that pays close to a 4% yield that may grow at 7-9% over time. In a similar vein, we have positions in Google and Facebook, two companies clearly riding the digital wave.

We have also built positions in domestic companies not really exposed to imported raw materials or components. One example is Waste Connections, which is the third largest waste company in the U.S. Demand is relatively stable, and because of the company’s careful market selection in areas with limited or no competition, Waste Connections enjoys significant pricing power. Another example is NextEra, an extremely well-run, regulated utility (the former Florida Power & Light), which has an unregulated subsidiary that has become the nation’s leading developer and operator of alternative (wind and solar) energy facilities. Neither the regulated side of the business nor the unregulated is likely to be affected by trade disruptions. We could go on with other examples, but this should give you an idea of our approach. Importantly, we believe each company we own should see significant growth for the foreseeable future and have a clean balance sheet.

Our best guess – and we emphasize that it is only a guess – is that in the end the Trump administration’s trade rhetoric will ultimately prove to be more a negotiating tactic than a hard reality. That said, our trade partners are not idiots and will play tit-for-tat in ratcheting up tariffs until Trump steps back. It is in everyone’s interest to cooperate, but accidents can happen and playing chicken can at times cause serious injury. Stay tuned.

Finally, we would like to address the longevity of the current business cycle and ask whether it can continue much longer. This has been an unusual cycle in that it was preceded by a housing crisis that, in turn, ignited a full-blown banking crisis. Because housing had been so overbuilt in the run up to the crisis, and because the banking system was so impaired by the crisis, housing could not play its usual role as the engine of recovery. This, as we have written before, assured that the recovery would be more muted or less robust than normal. Such has been the case.

Moreover, this has been a recovery with very limited inflation. There are multiple explanations for this:

– Very slack labor markets:

- Globalization and technology have kept labor’s bargaining power in check.

– Technology:

- Technology is inherently deflationary and has grown significantly as a percent of the economy.

- The application of technology throughout the economy has enabled businesses to lower costs.

- Technology has given consumers unprecedented price discovery power, forcing businesses to compete harder on price.

– Unconventional oil and gas extraction technology:

- Fracking and horizontal drilling technology have enabled U.S. oil and gas producers to produce hydrocarbons at ever lower cost, resulting in a lack of energy cost inflation.

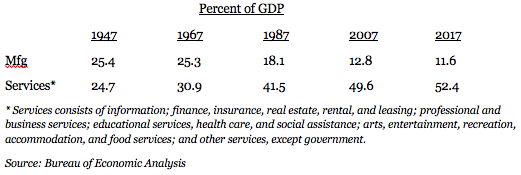

The fourth element to the long recovery may also tie back to technology, namely the changing nature of Gross Domestic Product (GDP) composition. Historically, the business cycle could be viewed as a giant inventory cycle. Simplistically, as the business cycle matured, shortages would develop and companies would be forced to double order to assure supplies of raw materials and components. As their suppliers eventually fulfilled these orders, companies would find they had too much inventory and would then stop ordering, causing suppliers to stop producing, sending the economy into recession. But in today’s economy with much of the “output” being digital and service-oriented, the concept of inventory becomes somewhat irrelevant. The Googles and Facebooks of this new world essentially have infinite capacity and do not need to order raw materials or components in the classic sense, with the exception of data storage and management. To the extent that GDP consists of software-based output and services rather than hardware or physical output, the inventory cycle becomes far less important and thus the business cycle should be able to endure for longer than historically with both lower inflation and fewer shortages.

The following table illustrates the dramatic shift in GDP composition over the past 70 years:

We have not seen much written on the relationship between GDP composition and the durability of the business cycle. We suspect that the significant decline in the importance of traditional manufacturing or physical output, coupled with the deflationary impact of technology, are combining to extend the longevity of the business cycle. Although the current expansion is now nine years old, none of the economists we most admire are calling for a recession anytime soon. Those that have talked about recession keep pushing out the onset. For now, trade issues are the key variables to consider. We expect the Fed will raise interest rates and tighten monetary policy at a measured pace so long as inflation rises only gradually. If inflation accelerates to a level the Fed regards as dangerous, then it may tighten monetary policy so aggressively as to cause a recession. Until that happens, the economy should continue to expand and the stock market is likely to grind higher.

If you have questions, please give us a call. We appreciate your continued confidence in our management.

Sincerely,

John Osterweis

Past performance is no guarantee of future results. Index performance is not indicative of fund performance. To obtain fund performance call (866) 236-0050 or visit osterweis.com.

This commentary contains the current opinions of the author as of the date above, which are subject to change at any time. This commentary has been distributed for informational purposes only and is not a recommendation or offer of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but is not guaranteed.

The S&P 500 Index is an unmanaged index that is widely regarded as the standard for measuring large-cap U.S. stock market performance. One cannot invest directly in an index.

As of 6/30/18, the Osterweis Fund held Digital Realty Trust (2.16%), Alphabet (parent company of Google) (6.46%), Facebook (2.54%), Waste Connections (2.64%) and NextEra (3.26%).

Holdings and sector allocations may change at any time due to ongoing portfolio management. References to specific investments should not be construed as a recommendation to buy or sell the securities by the Osterweis Fund or Osterweis Capital Management.

[33933]

© Osterweis Capital Management

© Osterweis Capital Management

Read more commentaries by Osterweis Capital Management