Synchronized Slowing Growth

Membership required

Membership is now required to use this feature. To learn more:

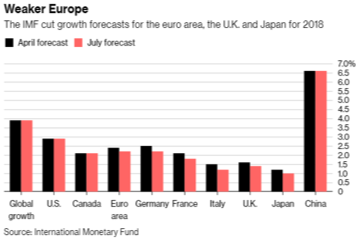

View Membership BenefitsSynchronized global growth was one of the main themes coming into 2018. In the second quarter GDP in the U.S. was the strongest since 2014, even as growth around the world downshifted. While global growth will be decent in the second half of this year, growth has already slowed in the U.K, Europe, China, and Japan. In July the International Monetary Fund trimmed its April 2018 growth estimates in July for a number of individual countries while maintaining their 3.9% global GDP projection for 2018. As the IMF noted in its Summary, “The expansion is becoming less even, and risks to the outlook are mounting. The rate of expansion appears to have peaked in some major economies and growth has become less synchronized. Growth projections have been revised down for the euro area, Japan, and the United Kingdom. Among emerging market and developing economies, growth prospects are also becoming more uneven, amid rising oil prices, higher yields in the United States, escalating trade tensions, and market pressures on the currencies of some economies with weaker fundamentals. The balance of risks has shifted further to the downside, including in the short term. Higher inflation readings in the United States, where unemployment is below 4 percent but markets are pricing in a much shallower path of interest rate increases than the one in the projections of the Federal Open Market Committee, could also lead to a sudden reassessment of fundamentals and risks by investors. Tighter financial conditions could potentially cause disruptive portfolio adjustments, sharp exchange rate movements, and further reductions in capital inflows to emerging markets, particularly those with weaker fundamentals or higher political risks.

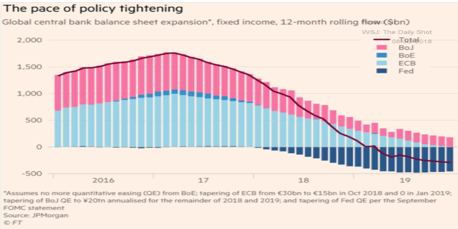

Central bank monetary policy has been a major tailwind for the global economy and global financial markets, as the European Central Bank (ECB), Bank of England (BOE), and Bank of Japan (BOJ) joined the Federal Reserve with large Quantitative Easing programs of their own. Even as the Fed began trimming its balance sheet in October 2017, the combined balance sheets of the Fed, ECB, and BOJ continued to expand so that the 12 month moving average was still positive. If the ECB lowers its purchases as it has indicated, the 12 month moving average of the combined balance sheet will drop below zero before the end of 2018. Short term interest rates in the U.S. have doubled from a year ago, while the 90 day Libor rate has doubled in the past 16 months. Trillions of dollars of loans are tied to these short term rates, which will progressively become a headwind in the U.S. and globally as loans are rolled over at higher rates.

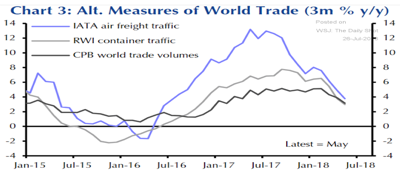

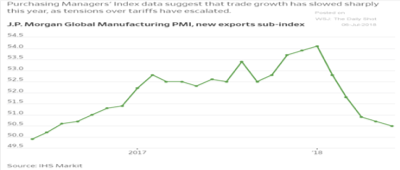

The volume of shipping by air or by container ship is a reflection of global growth. Since peaking at a high level in the second half of 2017, the 3 month rate of change in air freight traffic and container traffic slowed significantly through May. Although they are still well above the lows in late 2015 and early 2016, the rate of deceleration can’t be ignored. After bottoming in the first quarter of 2016, Global Industrial Production and the composite of Global Purchasing Manager Index’s (PMIs) rebounded strongly through the end of 2017, as measured by its 12 month rate of change. The strength in air freight traffic, container traffic, Global Industrial Production, and Global PMIs formed the back bone of the synchronized global growth story. Growth is still positive in all of these components but some of the air has come out of the story. The introduction of tariffs and angst about global trade in general has had a dampening effect on export activity, as measured by the new exports sub component of the JP Morgan Global Manufacturing PMI Index. As trade talks drag on or trade tensions increase, particularly with China, the global economy will be facing another headwind that was not present in 2017 when global growth was stronger and more synchronized.

U.S Economy

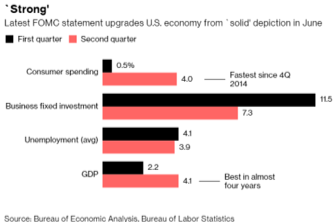

The Federal Open Market Committee upgraded its assessment of growth from solid to strong in the statement released after the August 1 FOMC meeting. In fact the FOMC used the words strong or strongly 5 times. “Economic activity has been rising at a strong rate. Job gains have been strong. Household spending and business investment has grown strongly.” The FOMC reaffirmed its commitment to gradual increases in the federal funds rate and noted that even after rate increases “The stance of monetary policy remains accommodative, thereby supporting strong labor market conditions and a sustained return to 2 percent inflation rate.” Whatever concerns FOMC members may have about potential risks to the economy from trade frictions, it isn’t reflected in the statement.

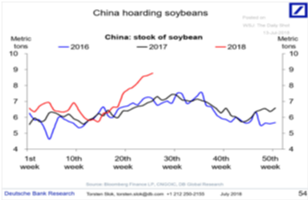

The FOMC’s statement shouldn’t have been a surprise since the first estimate of second quarter GDP clocked in at 4.1% after growing 2.2% in Q1. The main contributor was a surge in consumer spending from 0.5% in Q1 to 4.0% amounting to 2.7% of the 4.1% increase. Government spending added .37% and exports contributed 1.06% driven by preemptive buying from China of U.S. soybeans before they imposed tariffs on U.S. agricultural products. Inventory liquidation subtracted 1.0% from Q2 GDP in part from the export of soybeans which lowered the stock pile of soybeans. The decline in inventories was not entirely due to the surge in soybean export. The economy will receive a lift in the third and fourth quarter as companies increase production so firms can replenish inventories lowered in Q2.

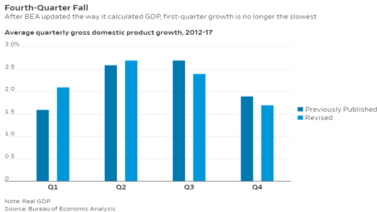

There are a number of factors that will cause growth to slow from the first estimate of Q2 at 4.1% in the second half of 2018, although GDP growth is likely to average above 3.0%. One reason is statistical. For years first quarter GDP has been consistently the weakest quarter of the year. This was one of the reasons I expected GDP to slow in Q1 of this year, along with a retrenchment in consumer spending after a strong holiday season. The Bureau of Economic Analysis (BEA) has recently concluded an extensive analysis to remove ‘residual seasonality’ from the data it receives from outside agencies like the U.S Census Bureau and the U.S. Labor Department. As part of their review, the BEA seasonally adjusted some underlying data that hadn’t previously been touched, and conducted numerous tests on historical data. The BEA now believes the updated series do not show signs of residual seasonality in real GDP or its major components over the full time span (1947-2017) or the most recent 15 years (2003-2017).

Correcting residual seasonality doesn’t impact annual GDP growth, but it did rebalance the amount of quarterly growth within each year. Prior to this analysis first quarter GDP averaged 1.6% from 2012 through 2017. After the revisions, the BEA now reports that first quarter GDP growth actually averaged 2.1% during that period. The average for growth in the second quarter was also lifted from 2.6% to 2.7% through 2017. Since the elimination of residual seasonality doesn’t change annual GDP, the increase in growth for the first and second quarter were essentially taken from the third and fourth quarter in the prior estimates for growth. The BEA now believes third quarter GDP averaged 2.4% instead of 2.7% from 2012 through 2017, and fourth quarter growth was revised down to 1.7% from 1.9%. The revisions now make the fourth quarter the weakest quarter each year rather than the first quarter. The new seasonal adjustments will lower third quarter GDP growth by 0.3% in 2018 and by 0.2% in the fourth quarter. No one would be surprised if President Trump doesn’t use a Tweet to criticize the BEA for making these changes that will make the second half of 2018 less strong.

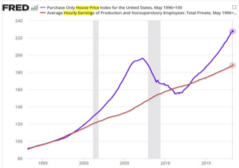

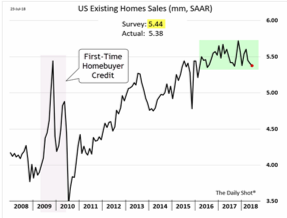

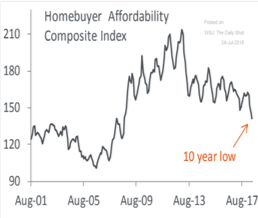

More strains are building on housing and auto sales that are likely to result in lower activity in the second half of 2018. Based on the Case-Shiller 20 City Home Price Index, home prices have been rising by more than 5% since 2012, while Average Hourly Earnings have grown by less than half that rate. The gap between home prices and Average Hourly Earnings is almost as wide as it was in 2006, which means fewer buyers can afford to purchase a home in many cities. Since last September the rate for a 30-year mortgage has jumped from 3.78% to 4.54%. The combination of higher home prices and mortgage rates has pushed the Homebuyer Affordability Index to the lowest level in 10 years. Existing Home Sales comprise 80% of housing activity so they are far more important than Housing Starts. The median sales price for an existing home in June was $276,000, up 5.2% from a year ago and a new all time high. In June Existing Home Sales slipped 0.6% to 5.38 million, according to the National Association of Realtors. Compared with a year ago, sales in June were down -2.2% and have declined on an annual basis in 5 of the first 6 months of 2018. Since early 2016 Existing Home Sales have hovered between 5.3 million and 5.7 million, and should they fall and remain below 5.3 million it would be a sign that housing will subtract to future economic growth. Housing Starts were down -12.3% May, which was the largest monthly decline in 18 months. Housing contributes 15% to 18% to GDP when construction, home improvements, lending, and home furnishings are combined.

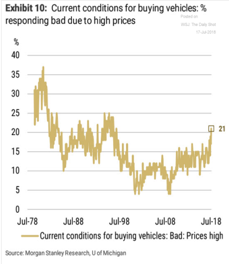

Since 2009 the average price for a car has risen by $6,000, from $26,000 to just over $32,000. Car lenders have responded by extending car loans to over 69 months. At the end of 2017, the average balance was a $31,099 and the average monthly payment was $515.00, both all time records according to Experian. The percentage of consumers who think it is a bad time to buy a car due to high prices reached a 20 year high of 21%, according to a recent survey by the University of Michigan. Steel accounts for 53% of the material in the average automobile and aluminum is 11% according to Ducker Worldwide. Although General Motors, Ford, and Fiat Chrysler buy almost all of their steel and aluminum from domestic producers, U.S. steel prices have increased in reaction to the 25% tariff the Trump administration announced in March and implemented on June 1 and the 10% duty on aluminum imports. Even though costs are rising for the automakers, they will have a tough time passing on all of their increased costs to consumers.

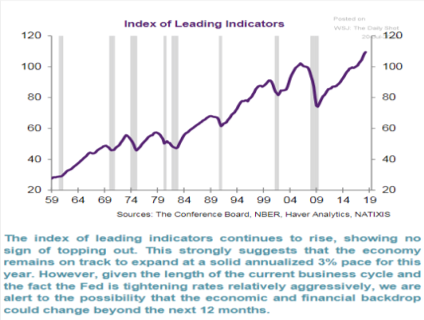

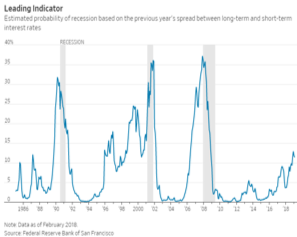

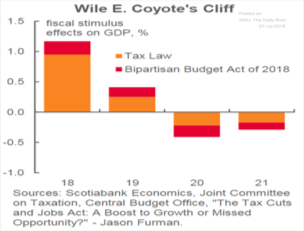

Although housing and auto sales may slow, economic growth is likely to hold above 3.0% in the second half due to the continued support from an increase in net pay for workers from the tax cut, additional government spending from the Bipartisan Budget Act, and more business investment. As noted, the main contributor to the pickup in growth in the second quarter was a surge in consumer spending from 0.5% in Q1 to 4.0%. Although Average Hourly Earnings are growing 2.7%, that reflects gross pay. After factoring in the increase to net pay from the tax cut, disposable after tax income is growing faster than 2.7%. My guess is that consumer spending will dip from the 4.0% annual pace in the second quarter in coming months. If spending drops to 3.0%, GDP would fall by .65% since consumer spending represents almost 70% of GDP. Government spending added .37% to second quarter GDP and is likely to add a similar amount in the third quarter since the federal government’s year ends on September 30. Business fixed investment growth fell to 7.3% in Q2 from 11.5% in the first quarter. While the ability to write off every dollar on any investment is very attractive, the uncertainty created by the trade issue likely contributed to the pullback in business investment in the second quarter. Since companies have the next 5 years to take advantage of this tax benefit, there is no pressing calendar issue that would trump waiting until the trade issues are resolved. No one knows whether the trade disputes with the E.U, Mexico, Canada, and China will be resolved quickly or successfully. What we do know is that the Leading Economic Indicator (LEI) is still rising at a brisk pace which suggests the economy will be just fine for the balance of 2018. Historically, the LEI has topped and begun falling 10 months in advance of the last 7 recessions. Given its rate of ascent it is not even close to flashing an early warning. The lift from fiscal stimulus will diminish in 2019 and turn negative in 2020, so the LEI may provide a warning of value if it begins to fall in the first half of 2019. Based on the spread between long term and short term interest rates from twelve months ago, the probability of a recession is 12%. Prior to the recessions in 1990, 2001, and the financial crisis in 2008, this forward looking indicator was above 25%. It would have to double from current levels before the risk of a recession would be meaningful.

Inflation Is Coming

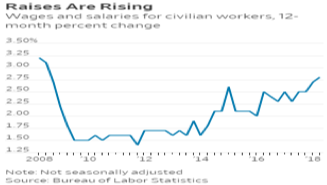

Inflation pressures are continuing to build. In recent weeks a number of companies have announced price increases of 4% or more including Coca-Cola and Proctor & Gamble. Input costs are rising in terms of energy costs, wages, shipping, and material prices in part due to tariffs on steel and aluminum. The Employment Cost Index (ECI), which includes wages and other employer paid benefits, rose at an annual rate of 2.9% in June, the highest in 9 years. Average Hourly Earnings were up 2.7% in the July employment report unchanged from June. However, the reference week for the survey for the July employment report did not include the 15th of the month, when many Americans are paid. When that happens, wage growth can be understated. The unemployment rate for those under 25 and without a high school diploma fell to 5.1% the lowest since records have been kept for this segment since 1992. These workers are being hired at the lowest pay scale which would also keep Average Hourly Earnings down.

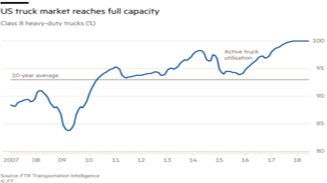

There is a shortage of truck drivers as older drivers retire and young people aren’t interested since the long term career prospects aren’t bright with A.I. drivers expected assume half of the jobs within the next decade. With fewer drivers available there are fewer trucks delivering goods, and the heavy duty truck segment, which accounts for 66% of the long haul segment, has been operating at 100% of capacity for more than a year. No surprise then that the cost of shipping has increased by almost 50% since early 2017. Trucks deliver nearly 70% of all manufactured and retail goods transported annually in the U.S., with a value $671 billion or almost 35% of annual GDP. The increase in shipping costs affects a broad spectrum of industries so the increase in shipping costs will filter through the economy and eventually lead to price increases.

According to the National Transportation Institute, median per-mile pay increased 8.2% to 39.8 cents for long haul truck drivers between December and June. The Bureau of Labor Statistics only shows that wages for long haul truckers rose 1.1% from June 2017. The potential for there to be an upside surprise in Average Hourly Earnings (AHE) in coming months is rising. The spread between the U-3 official unemployment rate of 3.9% and the U-6 underemployment rate of 7.5% fell to 3.6% in July. This is the smallest spread since December 2006. Since 1994 AHE have grown above an average annual rate of 3.3% when the spread was below 3.85%.

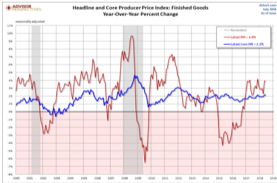

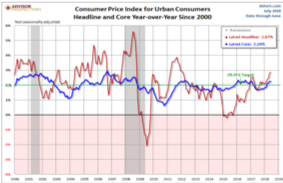

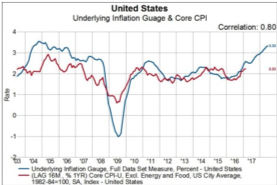

Inflation pressures are already evident in the headline numbers for the Producer Price Index (PPI) and the Consumer Price Index (CPI) which were up 3.9% and 2.87% in June. Both are above their core rates (PPI 2.2%, CPI 2.26%) and will continue to exert an upward pull as long as they remain above. The Personal Consumption Expenditure Index (PCE) is the Fed’s favorite inflation gauge and it has the same pattern, with headline inflation at 2.23% versus 1.9% for the core. The New York Fed’s Underlying Inflation Gauge (UIG) has an 80% correlation with the Core CPI and it continues to indicate that the Core CPI will be higher in coming months. If these inflation pressures lead to higher core inflation in coming months, the odds of a December increase in the federal funds rate will climb from the current level of 60%. The one caveat to this trajectory is a trade war that could cause global equity markets to experience a heart attack leading to a sudden drop in consumer confidence globally with an attendant fall in spending by consumers and business. This risk seems underappreciated especially by U.S. equity investors who assume a trade war will be avoided. I’m not so sure about that based on steps China has recently taken and statements.

China, No Trade Pushover

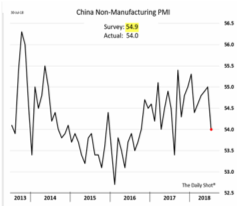

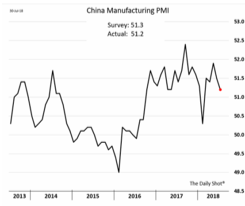

The consensus story line is that the U.S. has more leverage on China since they exported $505 billion of goods into the U.S. in 2017, while the U.S. only shipped $130 billion of stuff to China. The target is much bigger on China’s back than on the U.S., since the U.S. can slap tariffs on more goods than China can. Chalk one up for the U.S! China’s stock market as measured by the Shanghai Composite is down -17.1% through August 3, while the S&P 500 is up 6.0%. For the vast majority of investors who actually believe that markets discount the future, the only conclusion one can draw from this performance disparity is that China is losing and the U.S. will win. Chalk up another one for the U.S! In the second quarter GDP grew 4.1% in the U.S., while economic statistics in China are showing a slowdown as the recent figures for China’s manufacturing and nonmanufacturing illustrate. With the U.S. economy on the rise this is the perfect time for the U.S. to be pressing China, as opposed to a period when the U.S. isn’t as strong. The fact that China’s economy is weakening makes this advantage an even a bigger point of leverage. Chalk up another win for the U.S.! China has been ripping off the Intellectual Property of U.S. companies for too long, costing millions of middle class Americans their livelihood as factories closed, and stealing hundreds of billions of dollars from the U.S. each year through the trade deficit. Clearly the U.S. is justified in demanding free and fair trade. The U.S. is standing on the righteous moral ground in this dispute, which China will recognize and accept and thus seek to avoid a trade war. Another point for the U.S., which makes the trade negotiation tally 4 for the U.S. and 0 for China. We’re shutting China out!

While this analysis is neat and tidy it does manage to overlook what could be a number of salient points. The first is perspective. In the U.S. time is measured by quarters, but in China it is measured in decades. China’s leadership is not immune from short term considerations, but their focus is not centered on the next year or two but where things will be in 5 to 10 years and beyond. President Trump faces reelection in 2020 while changes to China’s Constitution will allow President Xi Jinping to remain in office until he dies. China is the country of Confucius, “If you think in terms of a year, plant a seed; if in terms of ten years, plant trees; if in terms of 100 years, teach the people.”

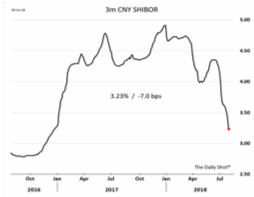

Actions speak louder than words or Tweets and China has been taking steps to insulate and bolster its economy from any short term negative impact from trade. In April, the Peoples Bank of China (PBOC), lowered its Reserve Requirement Ratio (RRR) by 1.0%, from the current 17% for large institutions and 15% for smaller banks. By reducing the amount of cash most commercial and foreign banks must hold as reserves, the cash can be used for funding new loans to stimulate growth. The PBOC has aggressively lowered short term interest rates especially since mid May. The 3 month Shibor rate has been lowered from 4.91% last December and slashed since May’s level of 4.33% to 3.17% in early July as trade tensions escalated. In late July the State Council encouraged local governments to issue bonds so the proceeds can be used to stimulate growth locally. The issuance of municipal bonds has soared from zero in January to $80 in June and will likely climb further after the State Council’s urging. In the last week of July the PBOC injected $74 billion into the banking system, the largest since 2014, so banks can increase lending. These steps indicate that China is easing fiscal and monetary policy in a myriad of ways as an insurance policy and to enable China to extend negotiations. China knows there is an important election in November in the U.S. The constituencies that supported President Trump that are now being hurt the most (farmers) can be counted on to apply more pressure directly on President Trump than China can through trade negotiations. According to Chinese philosopher Sun Tzu, “The supreme art of war is to subdue the enemy without fighting.” By stimulating its economy, China can weather the storm in the short term and achieve its long term goals. It’s possible that Sun Tzu may possess more wisdom and negotiating prowess than the guy who wrote the ‘Art of the Deal’.

In recent years China has expanded its military reach to a number of islands in the South China Seas despite Chinese President Xi Jinping’s 2015 pledge to President Obama that “China does not intend to pursue militarization” on the Spratly Islands. President Obama’s restrained response as China proceeded to expand only encouraged China to proceed. Satellite imagery now shows China has installed radars and communication jamming equipment in the Parcels and Spratlys Islands. In May China landed a long range heavy bomber on Woody Island which is claimed by Vietnam, Taiwan, Malaysia, Brunei, the Philippines, and China. The bomber has a range that covers almost the entire South China Sea. More than 30% of global trade passes through this area, which is also thought to contain large deposits of oil and natural gas. China says it has historical claims to almost the entire area and the right to defend those claims. One island in the Spratly Islands, which a UN court ruled belongs to the Philippines, now has a two-mile runway, a port and multi-story concrete barracks for Chinese military personnel. China claims the reefs are being developed to facilitate marine rescues, disaster relief, oceanic research, ecological protection and navigational safety. And if anyone believes that, China has an island it might sell you – for a price. Coincidently, the linkage of the bases in the Parcels and Spratly Island provides China an umbrella of coverage to control the South China Sea in all scenarios short of war with the U.S. In June it was reported that U.S. fighter pilots had been blinded in 20 instances since September 2017 by lasers coming from Chinese fishing boats, which are considered part of China’s militia. The US and China are signatories to an international treaty which bans the use of blinding lasers as a weapon of war, for what that’s worth. China’s military expansion reflects a mindset that is focused on the long term and an attitude that China will not be bullied nor dissuaded by any country.

On July 31 the Trump administration said it was considering increasing the tariff on $200 billion of Chinese imports from 10% to 25%. Comments by a spokesman for China’s Commerce Ministry didn’t sound as if China is cowed. “The U.S. unilaterally exerting pressure on China will get the opposite of what it wants.” Discussions haven’t even produced a plan for additional negotiations. The Commerce Ministry also issued a statement on August 2. “China has been fully prepared and will have to retaliate to defend national dignity and the people’s interests.” The word dignity caught my attention since it indicates that for China the trade negotiations represent something much bigger. China wants to be treated as an equal to the U.S. and respected, and that’s something China is not willing to trade away.

U.S. Stocks

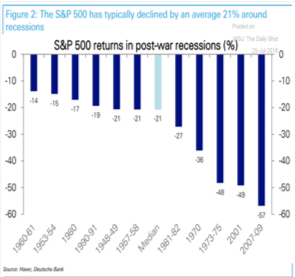

As noted, the risk of a recession developing in the next 6 to 9 months is low based on the Leading Economic Indicators which have turned down on average 10 months prior to the last 7 recessions. The spread between long term and short term interest rates from twelve months ago suggests the probability of a recession is just 12%. (Charts pg. 5) This is important since the some of the largest stock market declines since 1960 have occurred in response to a recession. While this is comforting it doesn’t obviate the risk from bull market event driven heart attack declines that have exceeded 15%, but were not associated with a recession. In 1962 the DJIA fell -21.7% between March and June after President Kennedy publically criticized U.S. Steel for increasing steel prices by 3.5%. In an April 11, 1962 press conference, Kennedy called the price hikes “a wholly unjustifiable and irresponsible defiance of the public interest.” In private Kennedy was less tactful. “My father always told me that all businessmen were sons of bitches, but I never believed it until now.” GDP grew 6.1% in 1962. In 1987 a combination of higher Treasury yields, a weaker Dollar, and portfolio insurance led to the October crash that shaved 30.7% off the S&P 500 between August 25 and October 19. In 1987 GDP grew 3.5% and by 4.2% in 1988. In August 1998, Russia defaulted on its bonds and Long Term Capital Management, navigated by 3 Nobel Laureates went bust. The S&P 500 fell by 16.5% even though GDP grew by 4.5% in 1998 and 4.9% in 1999. What were these declines discounting about the future and ‘telling’ investors? Absolutely nothing!

The stock market has been supported by a lack of selling pressure since the consensus outlook is for continued economic growth and good earnings. Second quarter corporate earnings have been good (up 23.5% according to Thomson Reuters), with the majority of companies meeting or beating estimates. But for those companies that have missed, their stock has been taken to the woodshed and greeted by a firing squad of sellers often resulting in double digit declines. The tranquility of the overall stock market is potentially masking an underlying vulnerability if a good reason to sell materializes.

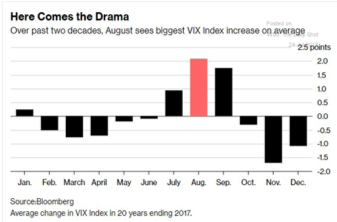

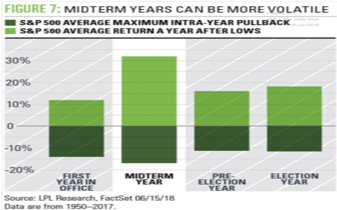

Equity investors are sanguine about the potential of a trade war which is likely misplaced if one listens to what China has been saying and doing. Over the past 20 years the biggest increase in Volatility (VIX) has occurred in August and September. The next 60 days is likely the window in which the trade dispute with China will come to a head. Midyear elections years have experienced an average drawdown in excess of 15% since 1950 with most of the declines occurring in August and September. The stock market has done particularly well in the year following mid year declines.

The technical support in the market is not as healthy as it may appear, if one is just looking at the major market averages. As noted in the Weekly Technical Review (WTR), a little more than half (53% on August 3) of NYSE stocks have been above their 200 day average compared to 68% in January, even as the S&P 500 hovers less than 2% below its January peak. This suggests that many stocks are further below their prior high than the cap weighted S&P 500. The lack of broad participation is also evident in the percent of stocks that have made a new 52 week high in the past 21 trading days. On August 3 just 1.43% of NYSE stocks made a new 52 week high compared to 2.61% in mid June and 6.92% in January. To be sure, no institutional money manager or portfolio manager will be running around their office screaming “Sell! Sell! Only 53% of stocks are above their 200 day average and the percent of stocks making a new high is dismal!” With the economy in good shape, there must be an exogenous event that results in a surge in selling pressure for a 15% correction to develop. The most obvious threat is a trade war since most are expecting a constructive outcome. The upcoming election could prove troublesome, if the polls in September show the democrats may do well enough to turn the House in their favor decisively. If the economy confirms that it is slowing, a normal correction that brings the S&P 500 down to 2700 is probable.

Treasury Yields

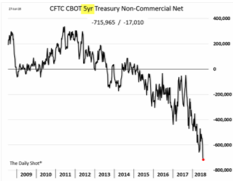

Sometimes the obvious turns out to be obviously wrong. By the time a trend has been in place long enough for investors to know the reasons why the trend has occurred and provided the opportunity for a majority of investors to get on the train, the trend simply runs out of gas and buyers or sellers. This is why contrary opinion has far more value in anticipating trend changes than the notion that markets are a discounting mechanism. The majority of investors expect Treasury yields to rise as the Federal Reserve continues to raise rates and inflation rises. To profit from that logical analysis investors have established a record number of short Treasury bond contracts in 5-year, 10-year, and Ultra Long bond futures. In total 1.438 million Treasury contracts have been sold short and at some point will be bought to close out the positions. If the economy loses some steam in the second half of 2018, investors who are short could be pressured to cover some of the short positions, which would help push Treasury yields lower, rather than higher. This suggests that the 10-year Treasury yield could test the March low of 2.715% and possibly the 2017 high of 2.63% in coming months. The 30-year Treasury may fall below the July 6 low of 2.925%.

Dollar

In February the percent of bulls expecting the Dollar to rally was 10%. The Dollar had declined from a January 2017 high of 103.84 to a low of 88.25 in February, despite 3 interest rate increases in 2017 and a fourth expected in March 2018. Since the February low, the Dollar has rallied by more than 8.0% and bullish sentiment in recent weeks has been hovering around 90%. Since the Fed is expected to increase rates in September and probably December, the expectation is that the Dollar will keep rising. My guess is the Dollar will exceed the July 19 high of 95.65, top below 96.00, and then undergo a 4% correction.

Gold

The positioning in Gold is almost as constructive as it was in December 2015 and early January 2016. Gold subsequently rallied from $1,060 in December 2015 to $1,365 in July 2016, a rally of 28% in less than 8 months. I doubt a move up of that magnitude is likely in the next 8 months. But the odds of an 8% - 10% rally that carries Gold above $1300 and possibly to $1350 by Thanksgiving is pretty high. A pullback in the Dollar will be supportive as would lower Treasury yields. If trade negotiations with China deteriorate and stocks undergo a correction, money may move into Gold.

Economic Enervation Reversed

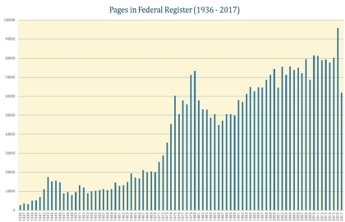

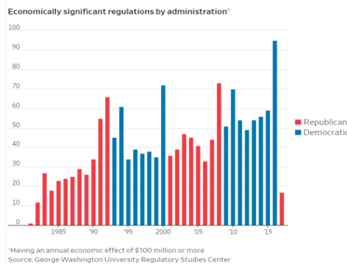

Enervate means to weaken or destroy the strength and vitality of something. I discussed how a mountain of regulation was stifling economic growth in June 2014 noting the multi-decade increase in the pages of the Federal Register, and a quote by Alexis de Tocqueville that proved prescient. Tocqueville was a French sociologist and political theorist who spent time touring the U.S. in 1831. In 1835 Alexis de Tocqueville warned that the real threat to American democracy wasn’t forceful tyranny, but a new kind of challenge. “Society will develop a new kind of servitude which covers the surface of society with a network of complicated rules, through which the most original minds and the most energetic characters cannot penetrate. It does not tyrannize but it compresses, enervates, extinguishes, and stupefies a people, till the nation is reduced to nothing better than a flock of timid and industrious animals, of which the government is the shepherd.” The Federal Register is a daily digest of proposed regulations from agencies, notices, corrections, and finalized rules. It was first published in 1936 and contained 2,620 pages. By 1966, the Federal Register was 16,850 pages long and mushroomed to 95,894 pages in 2016, the last year of President Obama’s legacy. In 2017 the number of pages in the Federal Register fell by almost 35% to 62,000 pages the lowest in 25 years. Rules that have a cost of at least $100 million are termed “economically significant”. During Obama’s 8 years as president, economically significant rules were 50% higher than during the Clinton or Bush administrations. Economically significant rules plunged from 95 in 2016 to less than 20 in President Trump’s first year.

Compiling reports of compliance costs from government agencies and outside sources, the Competitive Enterprise Institute (CEI) estimates $1.9 trillion was spent in 2017 by individuals and companies adhering to regulatory requirements. This amounts to more than 10% of GDP, and since businesses must pass along at least a portion of this regulatory compliance cost to consumers in the form of higher prices, it represents an unseen regulatory “tax”. However, there are definitive benefits to society from regulation, i.e. the air we breathe is cleaner, working environments and products are safer, as are the food and drugs we consume. These benefits offset a significant portion of the cost of regulation, so the regulatory cost to society may be less than half of the CEI’s estimate of $1.9 trillion.

In February 2017 the Economic Innovation Group (EIG) published the results of a study it conducted to quantify the number of firms that were opening their doors versus going out of business. The EIG study found more firm closures than startups in nearly two-thirds of all metro areas in 2014, the latest year with available data. There are many factors that can influence how willing people are in assuming the risk of starting a new business and regulation is just one factor. But existing small businesses have a front row seat on how regulation affects their business. Small businesses generate more than half of the net new jobs in the country and half of U.S GDP, according to the National Federation of Independent Businesses (NFIB). According to the NFIB 2016 Problems & Priorities report, the No. 2 problem facing small business owners is unreasonable government regulations due to the cost of compliance, difficulty in understanding rules, paperwork, and delays in getting answers to questions.

The reduction in overall regulation and economically significant rules in 2017 should in theory free up resources that could lift economically growth modestly in coming years, although it will prove difficult to quantify.

Jim Welsh

@JimWelshMacro

© Marcro Tides

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All