The United States is rapidly expanding its ability to export liquefied natural gas (LNG), as more countries look to embrace cleaner energy. Franklin Equity Group’s Matt Adams gives his outlook for US LNG and the possible investment implications.

Though carbon-based and not listed as a true “clean” energy source, natural gas has long been described as the “bridge fuel” to a cleaner energy future as the world weans itself off highly polluting coal and oil.

In our view, that bridge looks likely to extend well into the next decade, as more countries turn to natural gas in a bid to displace coal as the largest source of power generation. Moreover, long-term LNG supply additions appear to be slowing down after years of underinvestment and few recent project sanctions.

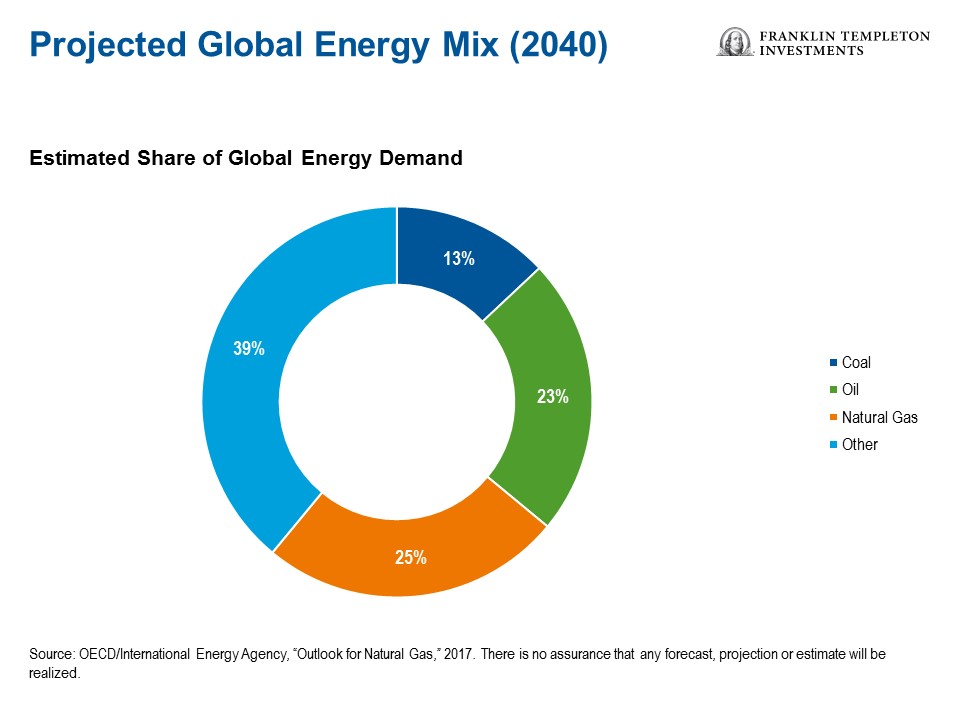

In 2016, natural gas supplied 22% of the world’s energy, and its use is growing.1 As the chart below shows, the International Energy Agency (IEA) projects natural gas to account for 25% of the global energy mix by 2040.

Why Demand for LNG Is Growing

In many parts of the world, constructing pipeline infrastructure to transport natural gas isn’t practical. In many countries outside North America, domestic production of natural gas is struggling or on the decline. That’s why we expect to see an increase in demand for LNG imports as countries pursue more natural gas-driven policies. The natural gas liquefaction process cools, condenses and transforms the gas into a commodity that can be ferried around the world in specialized compression tankers.

We’ve already seen the number of countries importing LNG rise from 35 in 2015 to 40 last year.2In addition, worldwide imports rose 9.9% in 2017, the strongest annual growth rate since 2010.3

Meanwhile, LNG supply from new additions has been slowing down and could create a supply deficit in the next decade if LNG demand continues on its current growth trajectory. Since LNG projects require a five-year lead time to develop, global LNG could move into a tighter market for longer time frames before higher prices encourage more investment in new supplies.

The Outlook for US LNG

In the United States, LNG exporters are benefiting from rapid demand growth and the streamlining of federal permits for LNG plants, export facilities and LNG tanker ships. As of June 2018, many companies said they are finalizing investment decisions to build planned US LNG facilities.4

Construction has been underway on a wave of US LNG plants along the Gulf of Mexico coast. The first, at Louisiana’s Sabine Pass, began shipping LNG in 2016, and Cove Point terminal in Maryland just started this year, while others are scheduled for completion through 2020.5

Will Trade Tensions Affect US LNG Exports?

In 2017, China was the third-largest destination for US LNG exports, behind Mexico and South Korea.6 The country’s demand for LNG is expected to continue growing rapidly as the Chinese government moves to limit air and water pollution from the combustion of coal. Coal, which accounts for about a third of global carbon dioxide emissions, currently dominates China’s total energy consumption (at about 70%) and electricity production (at nearly 80%).7

However, the escalating trade dispute between the US and China casts a shadow over those plans―at least in the short term. In August, China threatened to impose a 25% tariff on US LNG, which, if imposed, could make US LNG more expensive to Chinese buyers.8 However, given the lack of near-term supply sources which are not already contracted, the US remains a likely supplier of LNG to China, even with a tariff, given the wide spread between US and Chinese prices.

For now, US LNG exports account for a small amount of US natural gas demand, thus there has been minimal impact on US natural gas producers. Though if the tariff conflict were to continue for longer, it could eventually diminish one long-term export opportunity for US producers. That said, there appears to be growing opportunity in Europe for US LNG as the continent struggles to balance its demand needs with overdependence on Russian natural gas pipeline supplies.

The comments, opinions and analyses expressed herein are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. Because market and economic conditions are subject to rapid change, comments, opinions and analyses are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy.

This information is intended for US residents only.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

1. Source: IEA, Market Report Series: Gas 2018.

2. Source: International Group of Liquefied Natural Gas Importers, “The LNG industry, GIIGNL Annual Report 2018.”

3. Ibid.

4. Source: Financial Times, “US prepares for next wave of LNG exports,” June 20, 2018.

5. Ibid.

6. Source: U.S. Energy Information Administration, “China is a key destination for increasing U.S. energy exports,” July 10, 2018.

7. Source: U.S. Energy Information Administration, “Chinese coal-fired electricity generation expected to flatten as mix shifts to renewables,” September 27, 2017.

8. Source: Bloomberg, “Trump Push for Energy Dominant U.S. Blunted by China LNG Threat,” August 3, 2018.

© Franklin Templeton Investments

© Franklin Templeton Investments

Read more commentaries by Franklin Templeton Investments