As long-term investors, our credit research broadly focuses on determining if companies can service their debt throughout a credit cycle. In today’s crowded investment-grade (IG) space, our research also helps us distinguish overly leveraged companies from ones with manageable debt loads and durable business models. Within high yield, we are seeing a different dynamic compared to the enormous IG universe. Given shrinking supply, high-yield bonds have been enjoying positive tailwinds.

It’s quite a different story for the bank loan market, which now rivals high-yield in terms of size.1 With investor demand outstripping bank-loan supply, we are seeing more investors relinquishing control over credit terms. That could spell trouble down the road when the credit cycle finally shifts.

Investment-Grade Bonds

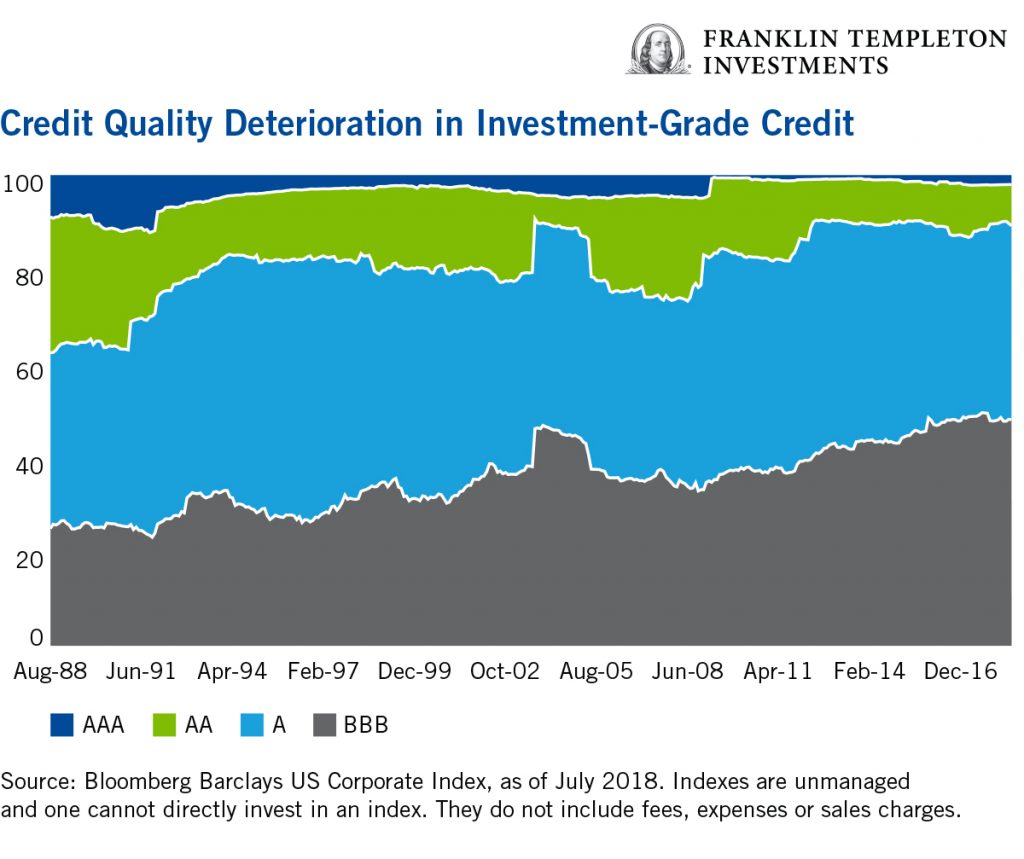

The IG seal of approval often conveys a status of safety that some investors might misinterpret. From our experience, we know these bonds can still be volatile if broader economic conditions deteriorate, or for company-specific reasons. To better gauge the risks of one IG bond in comparison to another, some investors look at credit ratings from agencies like Moody’s and Standard & Poor’s. The vast majority of IG corporate bonds historically carried the highest quality ratings, like S&P’s AAA, AA and A designations.

The quality of the IG universe, however, has steadily declined in recent years. On the back of low interest rates, many companies issued more debt to fund projects, acquire new companies, and even buy back equity shares. As more companies overindulged in borrowing, leverage levels rose, and credit metrics fell. BBB rated bonds (the lowest rating in the IG universe) now make up nearly half of IG securities, up from 25% in the 1990s, as shown in the chart below.

Given the late nature of today’s credit cycle, some investors might think exiting the BBB rated universe entirely and moving up the credit rating scale is a good idea. We think moving up in quality makes a lot of sense. However, we don’t need to exit the vast BBB rated universe entirely, given our deep credit research. Through our own analysis, we look to pinpoint BBB rated companies that we believe have the potential to generate reliable cash flows, even within competitive and rapidly evolving industries.

Survival of the fittest

One high-profile theme that brings secular industry changes and aggressive competition to life is the disruptive power of Amazon. Amazon’s purchase of Whole Foods in June of last year cast a dark cloud over the US grocery landscape. Overnight, markets reacted by indiscriminately driving down grocery retailing shares while spreads widened for bonds.

In the case of Kroger, the largest traditional US supermarket chain in terms of revenues,2 we thought the bond market was over-reacting. Kroger’s scale gives it tremendous cost advantages over smaller rivals. But it also fends off giant, well-resourced discounters like Wal-Mart and Germany’s Aldi, which decimated incumbent grocers in the United Kingdom. As a highly efficient operator, Kroger has an enviable reputation for generating strong cash flows despite strong competitors.

So is Kroger also equipped to battle the likes of Amazon? We think it is. Kroger has over 1,000 click-and-collect stores, where shoppers can order groceries online, with plans to double that footprint this year. It is also pushing into home food delivery and testing pre-made meal kits. Management also takes full advantage of its deep reservoir of customer data analytics, amassed over decades. By understanding customer behaviors, needs and patterns, it tailors its marketing promotions to increase repeat visits.

Kroger has all the fundamental qualities we look for in an attractive bond issuer—a defensible competitive position, proven cash flow generating capacity, and a smart, forward-looking management team that’s ready to take on Amazon.

High-Yield Bonds

Tight spreads in today’s high-yield market don’t offer much comfort this late in the credit cycle. And yet, high-yield bonds have broadly outperformed IG credit so far this year.3 That’s partly because high-yield durations4 are generally shorter compared with IG corporates, and less sensitive to rising Fed rates. But we’ve found another reason to like high-yield—shrinking supply.

Positive macro tailwinds

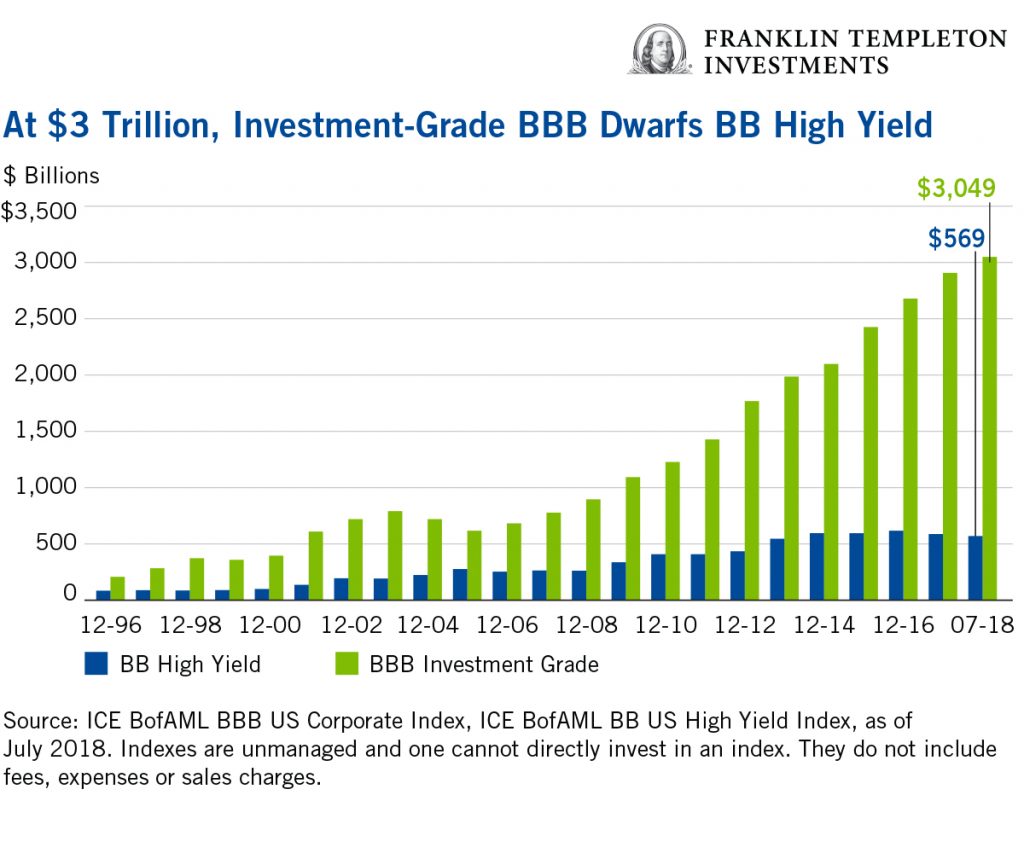

Unlike the steady rise in new IG issuance, net new high-yield issuance has been negative in recent years,5 as more high-yield entities are choosing to raise capital through leveraged loans. That means fewer high-yield bonds are coming to market than are being retired. The shrinking supply should give high-yield bonds a positive technical tailwind that can support valuations—a trend that IG bonds are not enjoying. The lowest spectrum of IG bonds (BBB) now tips the scales at over $3 trillion, compared with just $569 billion for BB high yield, as shown in the chart below.

Another potential tailwind for high-yield valuations is relatively low default rates—currently running below the historical average.6 The collapse of commodity prices in 2015 nurtured this, along with the dramatic crash in oil prices in February 2016. Like a healthy cleanse, the commodity correction helped purge over-leveraged players in the energy sector, in our view, setting the stage for more stability today.

Regardless of these positive macro tailwinds, our credit research capability remains indispensable as we seek to avoid company-specific meltdowns, and to uncover opportunities that others may overlook. Another example where exaggerated headlines and careful research revealed different stories is Bausch Health Companies (Bausch).

Previously known as Valeant, Bausch is a pharmaceutical and consumer health company. Back in 2015, as many pharmaceutical companies were producing record profits, the market applauded Valeant by driving its equity shares to extreme valuations. When Valeant appeared before the US Congress to discuss drug prices, it came under scrutiny by a high-profile short seller. Soon, rumors of large-scale fraud and potential bankruptcy swirled, and its shares nosedived. Although the pricing concerns were valid, we thought the media and certain vocal stakeholders had overly exaggerated Valeant’s risks.

Our health care credit analyst ignored the market noise and dove into Valeant’s product portfolio and pipeline. Two segments of Valeant, Bausch & Lomb and Salix, immediately grabbed his attention. Both segments had attractive products, robust cash flows, and peers with enterprise valuations that far exceeded what the market had assigned to Valeant. Bausch & Lomb gave Valeant some financial stability and revenue diversification, since it didn’t face patent expirations like a typical drug company. Bausch & Lomb’s main strength was its well-known consumer brand, and the repeat sales of staple products like contact lenses and saline solution. Valuations for industry peers like Cooper Cos. and Alcon were also far higher than investors gave Bausch & Lomb.

Evaluating Salix, we felt the market didn’t fully appreciate its upcoming expansion into the large gastrointestinal market with an existing product that faced few competing treatments. Doing a sum-of-the-parts valuation, we concluded that even with very little contribution from Valeant’s 1,500 other products, the valuations and cash flows of Bausch & Lomb and Salix alone could nearly cover Valeant’s debt.

What’s the main lesson from Bausch and Kroger? Markets and investors occasionally overreact to headlines. Investment managers with a long-term orientation and a willingness to do their own credit analysis can find investment opportunities that others may miss due to shortsightedness.

Bank Loans

Quite unlike the shrinking high-yield market, bank loan supply has doubled since 2010, now reaching over $1 trillion, according to S&P Global Market Intelligence. Yet investor demand is outstripping this supply, given strong relative performance in today’s rising-rate environment. With so much capital chasing bank loans, we have seen a steady erosion in bank loan standards, favoring borrowers over investors, in our view. Importantly, lenders are now losing their voice regarding changes to benchmark rates, which has important implications for future returns. We take a closer look at these troubling changes to credit agreements.

Rising rates accelerate demand

One of the main attractions of bank loans are their floating rates. Unlike fixed rate bonds, bank-loan coupons adjust in rising-rate environments because they are pegged to the London Interbank Offer Rate (LIBOR). This “benchmark rate” represents the average interest rate that a panel of leading banks charge each other for loans. This flexibility is attractive for investors looking to benefit from rising income or to avoid the negative interest rate exposure that fixed rate bonds may carry.

So far this year, this flexibility has paid off. On the back of two Fed rate hikes this year, bank loans generated attractive returns relative to some fixed rate counterparts. As bank loan demand has risen, we’ve noticed a steady decline in lender protections within credit agreements. Borrowers are modifying or eliminating protections that lenders considered sacrosanct—often creating greater risk for lenders. For example, bank loan issuers are incorporating provisions that allow them to issue more debt, pay out dividends to equity shareholders, and even put collateral out of lenders’ reach. Then, on the heels of news last July of LIBOR’s likely termination, a fresh wave of credit agreement amendments got our attention. We think more investors should sit up and take notice.

Due to a string of LIBOR pricing scandals, banks will no longer be required to quote LIBOR, starting in 2021.7 Many observers believe the banks will discontinue supporting LIBOR in the coming years, though no official comparable replacement exists yet. In response to these expected changes, borrowers started inking new provisions in credit agreements that take away lenders’ rights to opine on future LIBOR benchmark replacements.

Specifically, an issuer’s administrative agent can now identify future LIBOR benchmark replacements, but without giving lenders any say, or giving them just five business days to decline it. In the latter case, unless a majority of lenders in a syndicated loan reject the proposed LIBOR replacement in writing, the new benchmark rate becomes effective at the agent’s discretion.

Borrowers break an essential rule

In our view, this practice breaches a fundamental rule of bank loans: Any proposed reduction or change in the interest rate that lenders receive, may not move forward without the lenders’ affirmative consent. In our view, it is inappropriate to place the onus on lenders to respond negatively (i.e., opt out) within five business days. Lenders typically don’t know other lenders in the syndicate, nor have time to discuss the merits of a particular LIBOR alternative in just five days. We feel these actions will place investors at a possible disadvantage of having their expected income change, without any say in the matter.

We do not believe these provisions in new or amended loan documentation are in the best interest of our clients. That’s why one of our conditions before investing is that credit agreements give lenders the right of prior consent to any LIBOR changes. In several instances where we’ve seen unfavorable provisions regarding LIBOR introduced in loans we currently own, we have either eliminated or dramatically reduced our exposure to these borrowers. By par value, only 17% of our current bank loan holdings have objectionable LIBOR replacement language. By comparison, we currently estimate that 50% of the broader loan market contains this language.8

The loosening of credit agreements combined with record issuance levels should warrant more, not less, vigilance by investors. And yet, many investors are passively accepting these changes, and signing away one of their fundamental rights. We are encouraging more asset managers to join us in negotiating for the removal of unfavorable LIBOR replacement language in credit agreements. In our view, LIBOR replacements in syndicated bank loans should not be able to move forward without the affirmative consent of a majority of lenders.

Replacing LIBOR—What’s the Big Deal?

Although it is too early to know what rate or methodology will eventually replace LIBOR, a new benchmark rate could significantly affect the bank loan market and cause volatility. If the new benchmark rate does not closely replicate LIBOR’s implied risk-adjusted return, it could reset the spreads that lenders charge and borrowers are willing to pay for loans. In other words, depending on LIBOR’s replacement, there is a real probability for a large shift in value—either from lenders to borrowers or from borrowers to lenders.

© Franklin Templeton Investments

http://us.beyondbullsandbears.com

© Franklin Templeton Investments

Read more commentaries by Franklin Templeton Investments