In the 16 years since the Principles for Responsible Investment (PRI) were first unveiled there’s been a sea change in awareness and concern for the environment among the general public. But that hasn’t necessarily been reflected in the asset management world. Recently returned from the annual PRI in Person Conference in San Francisco, Franklin Templeton’s Head of European Fixed Income, David Zahn, detects an appetite for change among investors and investment managers.

After attending this year’s Principles for Responsible Investment Conference (PRI) in San Francisco―close to Franklin Templeton’s San Mateo headquarters—our takeaway message is clear: Investors and investment managers have to be proactive in addressing changing public attitudes toward the environment.

Unsurprisingly, with the conference taking place as Hurricane Florence was bearing down on the US East Coast, climate risk was high on the agenda for many delegates and there was much discussion of how investors assess and manage environment, social and governance (ESG) factors.

We believe the most important force for addressing environmental and social concerns may be the way we invest. In our view, that’s even more influential than the efforts of nongovernmental organizations or intergovernmental accords.

So, it was sobering to learn that on a show of hands, only around 10% of the audience at the conference identified themselves as portfolio managers or investment risk-takers.

That low percentage suggests to us integration of ESG processes is not what it could be across the asset-management industry.

Several speakers at the conference highlighted the importance of integrating ESG processes rather than treating ESG as a separate discipline.

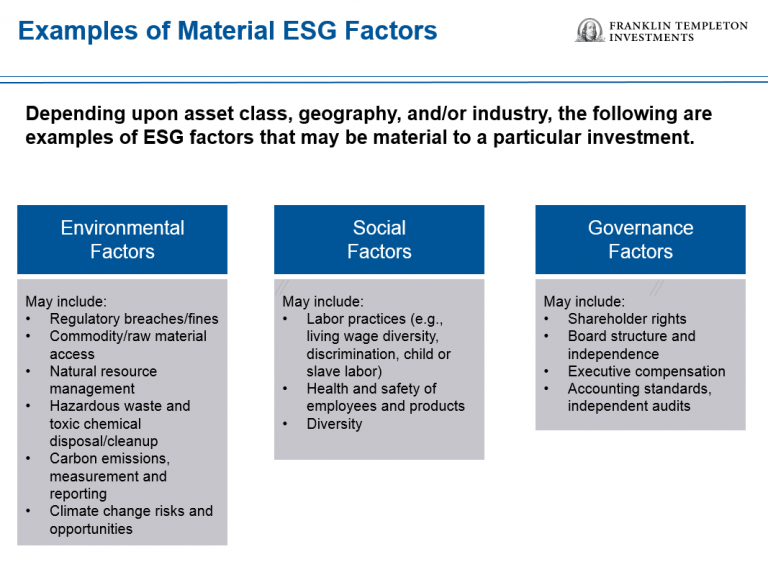

An Integrated Approach to ESG

At Franklin Templeton, we are working to make ESG considerations an inherent part of how we evaluate sectors and future business opportunities.

As active asset managers, we think it’s important to understand how broad macro themes such as CO2 emissions and water-stress impact the longer term strategic risks and opportunities for assets in our portfolios.

Our research teams have access to tools that allow them to synthesize ESG data themselves, rather than relying on a separate team to provide an overlay to financial valuations.

These tools include third-party ratings and research as well as our own proprietorial models.

Latent Risks Can Quickly Surprise

We view failure of climate change mitigation and adaptation, water crisis, cyber security as more than environmental and social challenges; we see them as economic issues and as such, we want to understand them from a risk and return perspective.

We believe these issues identify additional sources of potential risks and opportunities for investments that are often lurking beneath the surface of corporate and sovereign balance sheet information alone.

And as investors, we have to be aware of latent risks that may sit dormant in the risk register but which may come to the forefront very quickly.

A good example is plastics. Five years ago, very few people were concerned about plastics usage; today it’s recognized as a global issue and a growing number of countries are coming up with policies and sanctions to reduce plastic pollution.

The speed at which these issues can move from the bottom to the top of the agenda can have a meaningful impact on assets and has to be considered as part of an integrated ESG approach.

The Role of Millennials

A new generation of investors is taking a lead in shifting sentiment.

We recognize many younger investors, in particular millennials, appear to be much more concerned than other generations about where their money is being put to work.

In many instances, these younger investors seem more interested in whether their money is doing the right thing for the environment. For these individuals, investing isn’t solely about making a profit.

Still, the evidence suggests that those two things—doing the right thing for the environment and making money―do not have to be mutually exclusive.

Former US Vice President Al Gore told conference delegates in his keynote address: “The idea that the environment and the economy are in conflict is false.”

Historically, many investors felt an ESG-led investment approach would mean lower returns.

Our research suggests the opposite is true. In a meta-analysis conducted in 2015, 90% of the more than 2,200 studies covered found there was at least some correlation between ESG standards and corporate financial performance.1 In addition, a large majority of studies reported a positive finding.2

Investment Opportunities Should Emerge

As the business rationale for ESG crystallizes, we expect investors increasingly will be forced to engage in this space as a matter of fiduciary duty.

At the same time, events such as the PRI in Person Conference reinforce our view that there should be an investment opportunity associated with adapting to climate risks.

Speaking at the conference, PRI CEO Fiona Reynolds said: “Climate is a significant risk to portfolios and also an opportunity for investment in new technology and the energy transition.

“There’s a lot for investors to grapple with. You have to worry that some are not thinking about these issues. I wouldn’t want my pension savings [to be managed in a way that was] not thinking about climate risk,” she added.

Fixed Income Can Have a Louder ESG Voice

Traditionally, equity investors have been seen as the battle troops for ESG, exerting their influence on companies as shareholders. Meanwhile, fixed income investors may have been thought of as less-influential.

We take a different view and think fixed income has the potential to make a big impression in this space.

Consider for example that most firms only issue equity once, when they go public, or are private companies. By contrast, many firms issue bonds multiple times and many every year. So they need to keep a dialogue with investors.

There can certainly be a cost to those companies if they don’t manage those relationships with their bondholders well. Investors may demand higher yields on future debt.

The Important Role of ESG Data

It was clear from the PRI in Person Conference that ESG data are still evolving: there’s not yet the detail nor historical volume that there is for price returns history.

There was some discussion during the event of work that the Sustainability Accounting Standards Board (SASB) has been doing, particularly the connection that SASB makes between material ESG issues and financial impact.

That connection is something we’ve been focused on for some time. The ability for us to look at traditional quantitative measures of risk alongside sustainability risk allows us to get a multi-faceted deeper understanding of all the drivers of risk of the securities we’re invested in.

We see value in the intersection of evaluating financial measures alongside macroeconomic measures as well as sustainability measures.

In our view, the combination of all three really helps deepen our understanding of assets and helps us identify some of the longer term strategic risks in these themes that are disrupting sectors that we’re looking at.

The comments, opinions and analyses presented here are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. Because market and economic conditions are subject to rapid change, comments, opinions and analyses are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy.

This information is intended for US residents only.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

What Are the Risks?

All investments involve risks, including possible loss of principal. Bond prices generally move in the opposite direction of interest rates. Thus, as prices of bonds in an investment portfolio adjust to a rise in interest rates, the value of the portfolio may decline. Investments in foreign securities involve special risks including currency fluctuations, economic instability and political developments.

__________________________________________________________________

1. Source: ExaneBNP Paribas, Sustainable Finance, as of February 2018.

2. Source: Ibid.

© Franklin Templeton Investments

© Franklin Templeton Investments

Read more commentaries by Franklin Templeton Investments