Retirees got some good news from the US Social Security Administration, as it recently announced a 2.8% bump in benefits in 2019, the largest increase in seven years. Unfortunately, the good news also came with some bad news—higher Medicare premiums that could offset those gains. Gail Buckner, CFP, our personal retirement and financial planning strategist, takes a look at the situation.

Starting in January 2019, retirees will see their monthly Social Security checks increase by 2.8%. This is the largest cost-of-living-adjustment (COLA) increase since 2011 when we had a COLA of 3.6%1. The size of the COLA (which was 0% in 2009 and 2010) is based on the amount of inflation we’ve had from one year to the next, as calculated by the Bureau of Labor Statistics.

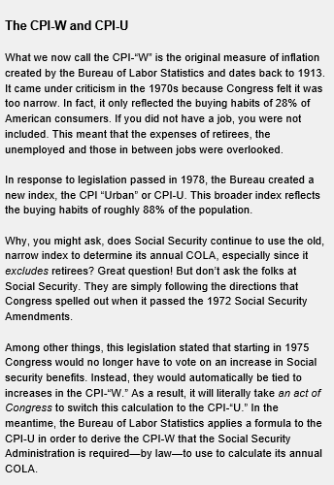

Specifically, Social Security looks at the Consumer Price Index for Wage Earners and Clerical Workers, or CPI-W, and is based on a year-on-year comparison of inflation—that is, it compares what it was in the third quarter of the previous year to the same period in the current year.2

The CPI-W covers a wide range of items that households commonly buy including food, medical care, shelter, energy, utilities and transportation. It turns out that during July, August and September of this year, Americans paid 2.8% more for this “basket” of goods and services than they did last year.

The problem is, this is not as neat and tidy a number as you might think. When you take a close look at the components of the CPI-W, you find that many things we bought actually went down in price compared to a year ago. This includes what we spent to buy clothing, an airline ticket or a used car or truck.3

So what caused the year-over-year spike in inflation? Don’t blame medical care! That rose less than 2% over the past 12 months. The cost of housing or “shelter” rose more than 3%. But the big culprit was the cost of energy. The price of a gallon of gasoline went up 9.1%. Fuel oil was up a whopping 23.4% over the same timeframe.

Other Numbers Impacted by Social Security’s COLA

The COLA that Social Security applies to retiree benefits also boosts several other key numbers. For instance, if you work in a job that deducts Social Security tax from your paycheck, a.k.a. “payroll tax,” in 2019 you will pay this tax on as much as $132,900 in earnings. (Earnings above this amount are not subject to payroll tax.) This year the “earnings limit” is $128,400.4

If you are under full retirement age (66 for those born between 1943 and 1954), receiving Social Security benefits and also earning income from a job, Social Security may reduce your monthly check. It depends upon whether your pay exceeds the annual “earnings limit.” Next year, the earnings limit will increase to $17,640. For every $2 above this amount, Social Security will hold back $1 in benefits. (Don’t worry! Any amount Social Security withholds is credited to your account. This will be reflected in your monthly checks once you reach full retirement age.) 5

If you are turning 66 next year, the “earnings limit” is $46,920. For every $3 over this amount that you earn, $1 in benefits is held back. Again, the same adjustment applies when you turn “Full” Retirement Age or “FRA.”6 Once you reach FRA, no matter how much money you earn from a job, you will receive 100% of your Social Security benefit.7

Keep in mind, if you are receiving Social Security and return to work, the income you earn from your current job will be reported to Social Security. If it is higher than what you earned in previous years, you could see your Social Security benefit go up.

A Dose of Reality, Compliments of Medicare

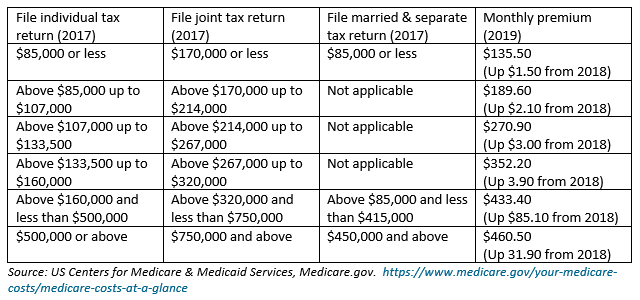

Medicare doesn’t use a COLA to calculate your monthly insurance premium. It simply tries to estimate what its costs will be in the coming year and then tells you what you have to pay based upon the income you had two years ago. In other words, if you retire next year, Medicare will look at what your income was in 2017 and that will determine your monthly Part B premium in 2019.

Since most Social Security recipients fall into the “hold harmless” category, as you can see in the table below, the brunt of the annual increase in Medicare premiums falls on those with higher incomes. The table shows your monthly premiums for 2019, based on your 2017 yearly income.

So, while any bump in Social Security benefits is good news, it doesn’t necessarily mean those checks will actually stretch much farther for many retirees grappling with higher Medicare premiums.

Gail Buckner’s comments, opinions and analyses are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. Opinions and analyses are rendered as of the date of the posting and may change without notice.

Certified Financial Planner Board of Standards Inc. owns the certification marks CFP®, CERTIFIED FINANCIAL PLANNER™, CFP® (with plaque design) and CFP® (with flame design) in the US, which it awards to individuals who successfully complete CFP Board’s initial and ongoing certification requirements.

This information is intended for US residents only.

Important Legal Information

All financial decisions and investments involve risk, including possible loss of principal.

The information (including tools) contained herein is general and educational in nature and should not be considered or relied upon as legal, tax, or investment advice or recommendations, or as a substitute for legal or tax counsel. It is not intended to serve as the primary basis for your investment, tax or retirement planning purposes, and should not be used as the final determinant on how and when to claim Social Security benefits, which can be a complex and personal decision. FTI is not responsible for content on the Social Security Administration’s website. Federal and state laws and regulations are complex and subject to change, which can materially impact your results. Always consult your own independent financial professional, attorney or tax advisor for advice regarding your specific goals and individual situation.

Hyperlink Disclaimer

Links can take you to third-party sites/media with information and services not reviewed or endorsed by us. We urge you to review the privacy, security, terms of use and other policies of each site you visit, as we have no control over and assume no responsibility or liability for them.

1. Source: Social Security Administration. https://www.ssa.gov/OACT/COLA/colaseries.html

2. Ibid.

3. Source: US Bureau of Labor Statistics economic release, October 11, 2018. Unadjusted percent change, 12 months ended September 2018.

4. Source: Social Security Administration Cost of Living Adjustment (COLA) information for 2019. https://www.ssa.gov/news/cola/

5. Ibid.

6. Ibid.

7. Ibid.

© Franklin Templeton Investments

© Franklin Templeton Investments

Read more commentaries by Franklin Templeton Investments