There has been a lot of talk this year about the flattening of the US yield curve—which is a graphical representation of the spread between short- and long-term interest-rate instruments.

In the past, when spreads between short- and long-term rates narrow, it typically suggests that the market believes economic growth and inflation are not sustainable and will fall in the future.

However, our senior investment leaders make a case that the “predictive power” of the yield curve when it comes to the US economy may not really be so predictive this time around.

Why the Yield Curve Is Flattening

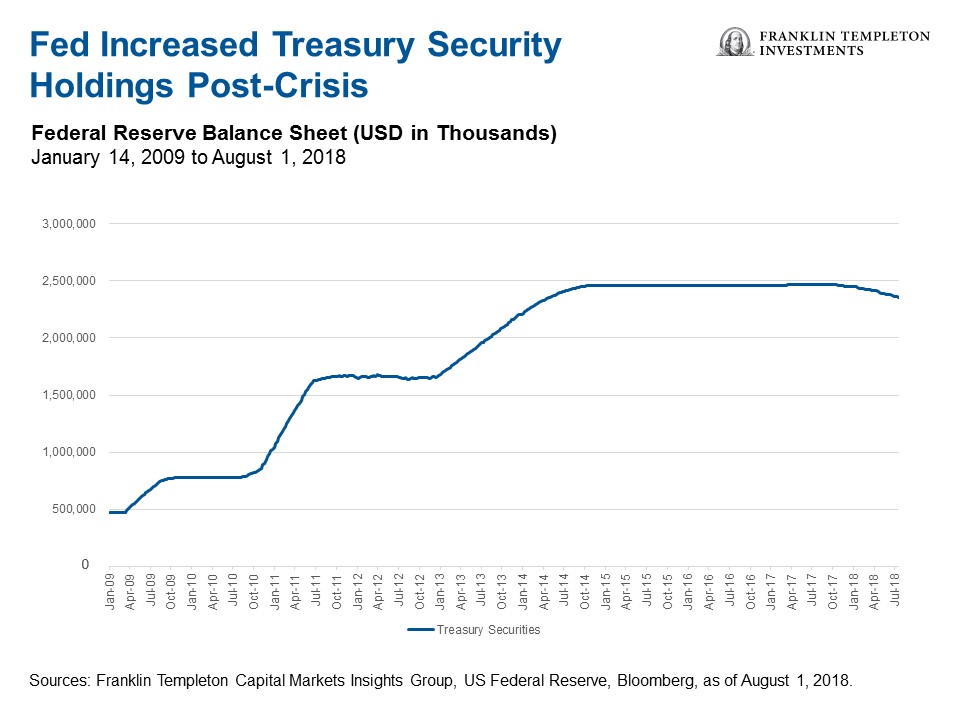

Through monetary policy actions—that is, buying or selling securities—the US Federal Reserve (Fed) has control over two short-term interest rates, the discount rate and the fed funds rate. The fed funds rate (considered the “benchmark” rate) is the rate which banks and other depository institutions lend money to each other on an overnight basis.

It is this rate that is more often manipulated, and typically impacts other short-term lending rates along the yield curve. Since 2015, the Fed has been increasing this benchmark rate in response to a growing US economy, and other short-term rates have followed.

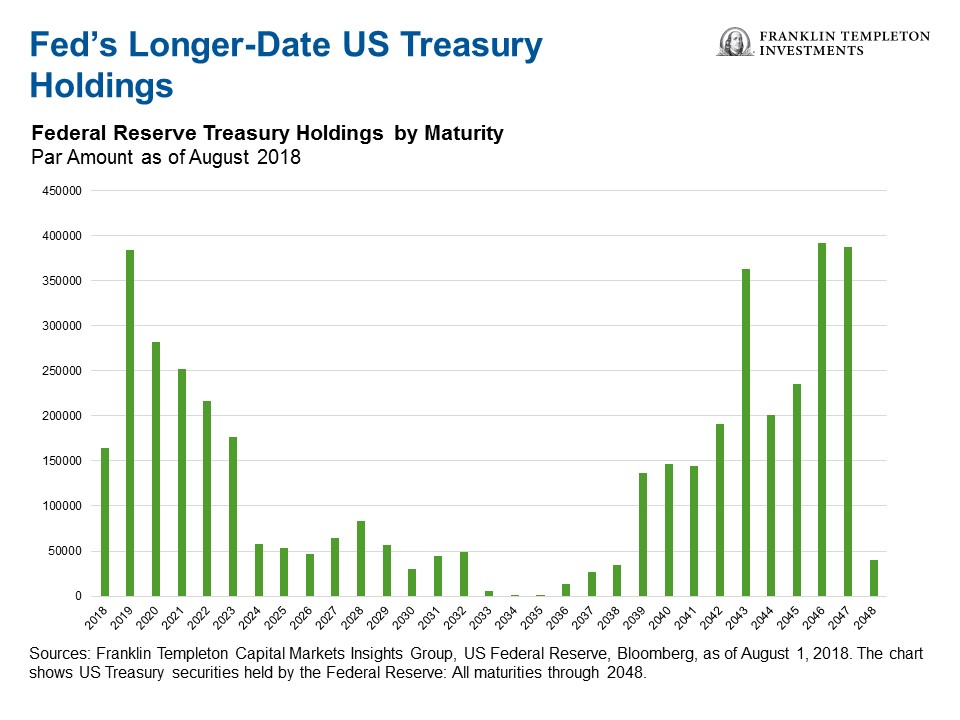

Meanwhile, various factors have kept a lid on long-term rates for much of this year. And some market observers have noted, without another quantitative easing program, the Fed can’t control the long end of the yield curve, represented by instruments such as 10- and 30-year Treasuries.

Simply put, we have seen the Fed raise short-term rates without a corresponding rise in long-term rates, causing a flattening of the curve.

US Yield Curve as a Recession Indicator

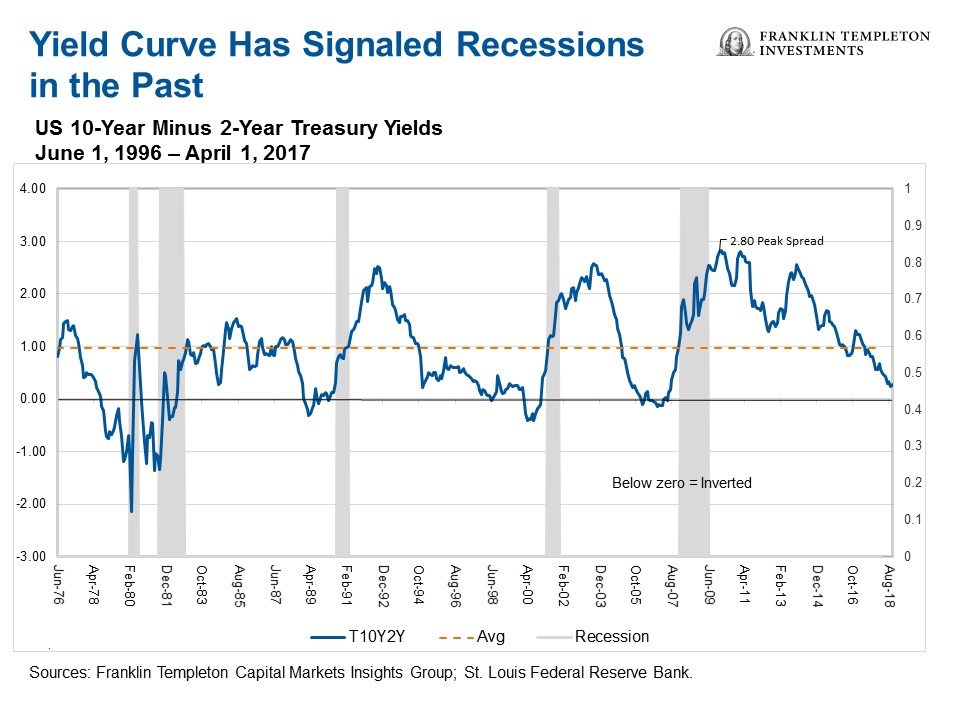

The spread between long-term and short-term rates has historically been considered a closely watched indicator used to gauge the health of the economy. In the past, changes in the yield curve have been a useful barometer to determine what phase of the cycle the US economy is currently in.

As the yield curve has flattened over the course of this year, some investors may be wondering if the yield curve could eventually invert, or fall below zero.

In this article, Ed Perks, CIO of Franklin Templeton Multi-Asset Solutions, points out that an inverted yield curve has been an indicator of US recessions in the past. As the chart below shows, the gap between two-year and 10-year Treasury notes narrowed to roughly 24 basis points in August, and the yield curve compressed to a level not seen since August 2007.

“This metric is closely watched due to its apparent predictive value—every recession in the past 60 years has been preceded by the yield curve inverting, or falling below zero.”

Ed Perks, July 31, 2018.