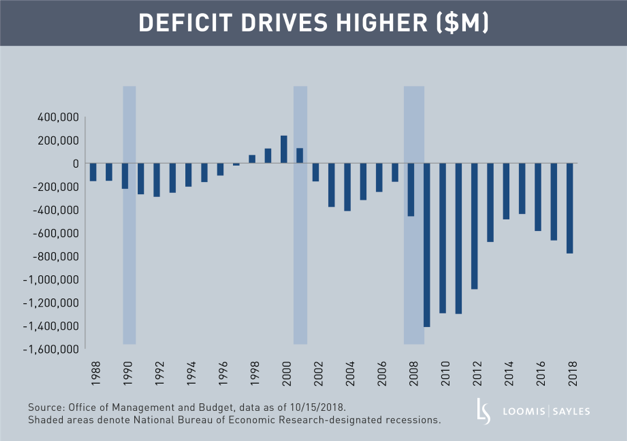

The federal deficit hit $779 billion in fiscal year 2018.1 This was the highest level since the $1.09 trillion deficit of FY 2012. Many pundits point to the tax cuts as the driver, but that tells only a part of the story.

It is true that increases in discretionary spending and tax cuts boosted the deficit in FY 2018. But the deficit also rose in FY 2016 and FY 2017 despite an expanding economy, a falling unemployment rate and no tax cuts.

How do you balance these facts? The surge in entitlement spending (Social Security, Medicare, Medicaid, the Children’s Health Insurance Program and the Affordable Care Act) is driving the deficit upward and I don’t see it relenting.

To make matters worse, an expanding federal debt requires more funding from the Treasury market, which should pressure interest rates higher across the yield curve. So look for increases in the national debt and higher interest rates to further drive up net interest outlays, and in a circular fashion further increase the national debt.

The deficit is likely to pass the $1 trillion threshold in FY 2019. Without a change in government policy, it won’t stop there.

MALR022676

This blog post is provided for informational purposes only and should not be construed as investment advice. Any opinions or forecasts contained herein reflect the subjective judgments and assumptions of the authors only and do not necessarily reflect the views of Loomis, Sayles & Company, L.P. This information is subject to change at any time without notice.

1October 1, 2017, through September 30, 2018.