In their fourth-quarter (Q4) 2018 outlook, K2 Advisors’ Research and Portfolio Construction teams take a deeper look at alpha, and why they feel it’s misunderstood. They believe offering these insights will help investors better understand the rationale for owning retail mutual funds that invest in hedge strategies.

Alpha Is Hard

For this quarter’s outlook we are taking a deeper look at alpha. For hedge funds, the importance of this measure cannot be overstated. The problem, from our perspective, is that often it is misunderstood. From a purely qualitative standpoint investors understand alpha as the value that an active portfolio manager adds to or subtracts from a fund’s return, depending upon his or her skill as an investment manager.

Fair enough. But when conversations turn to measuring this fleeting statistical phenomenon, things can get a bit more ambiguous.

Often alpha is talked about in the abstract. A precise quantitative measure is sometimes not specified or, if it is, the calculation may be flawed. Ad-hoc or loose definitions are also often used and never tested for validity.

To be clear, we are not casting aspersions. We understand the challenge. For all intents and purposes, alpha—in the purest mathematical sense—is hard. It is hard to quantify, hard to consistently measure, and even harder to capture. Sometimes asset management marketing materials describe “generating” alpha.

To be precise alpha cannot, in fact, be “generated.” It can only be captured—and it is in short supply. Over time and across markets it represents a zero-sum game. To obtain alpha means taking it away from someone else.

Mathematically speaking (and we are sorry for this), alpha represents the abnormal rate of return on a security or portfolio in excess of what would be predicted by an equilibrium model like the capital asset pricing model (CAPM). The CAPM says that the expected return for an investment is proportional to its exposure to systematic, or non-diversifiable, risk.

In plain English, any investment should earn whatever the risk-free rate is (let’s say US Treasury bonds… for now), plus any premium associated with the level of market risk taken (or so-called beta).

Taking it a step further, alpha is the coefficient—or residual of the expected return. In an efficient market, the expected value of the alpha coefficient would be zero; however, we find markets to be decidedly inefficient. As such, if a fund or security returns more than what would be expected given its market sensitivity (beta), it has positive alpha. If it returns less than its beta predicts, it has negative alpha.

So in the simplest of terms, alpha is the portion of a portfolio’s return that is the result of factors other than the portfolio’s exposure to the market.

Measuring alpha in alternatives presents an additional layer of complexity. Defining market beta is challenging. Remember many alternatives (not all) are considered “absolute return” vehicles; that is, they are not tied to any given benchmark. Take hedge funds, for example.

While hedge funds can be measured against traditional market benchmarks such as the S&P 500 Index, to identify a hedge fund’s beta profile requires insight and transparency into its trading strategy and the securities in which it invests. In this way, the systematic risk exposures can be understood and measured.

In our view, the good news is that alternatives and other select investment strategies deliver measurable alpha, provided that the appropriate methodology is used. That said, it is important to recognize that measuring and monitoring alpha is a variable exercise contingent upon each individual manager’s investment program, and the securities in which they invest.

Traditional measures and reports of alpha often fail to control for the statistical artifacts that can significantly alter the meaning of reported numbers. Just something to bear in mind. You cannot measure what you cannot see—and alpha is no exception.

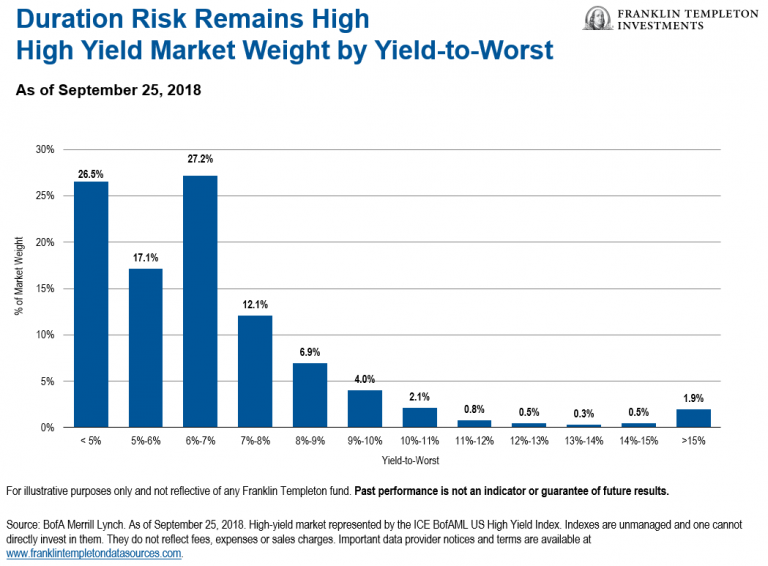

Relative Value – Fixed Income

With interest rates starting to rise, duration1 risk is coming into focus for fixed income investors, such as in the high yield market. In our view, relative value fixed income strategies such as long/short credit are well positioned, given their shorter duration portfolios, and should be able to capture alpha from rising sector dispersion.

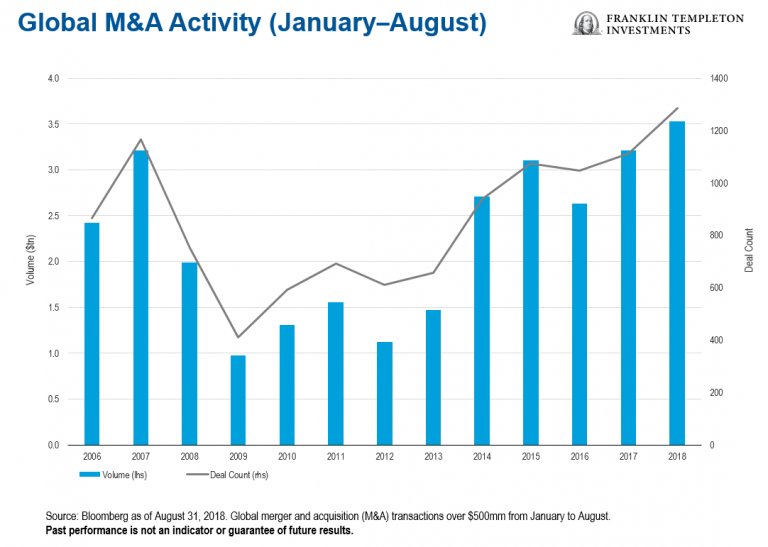

Event Driven – Merger Arbitrage

Corporate activity is expected to remain strong in 2019. The successful completion of the AT&T/Time Warner transaction is expected to lead to an increase in deal activity in the media industry, as well as a broadly more favorable outlook on vertical mergers. Tailwinds for corporate activity also persist, including corporate tax cuts, cash repatriation, high CEO confidence and strong credit markets. The most significant headwind is the trade war between the United States and China.

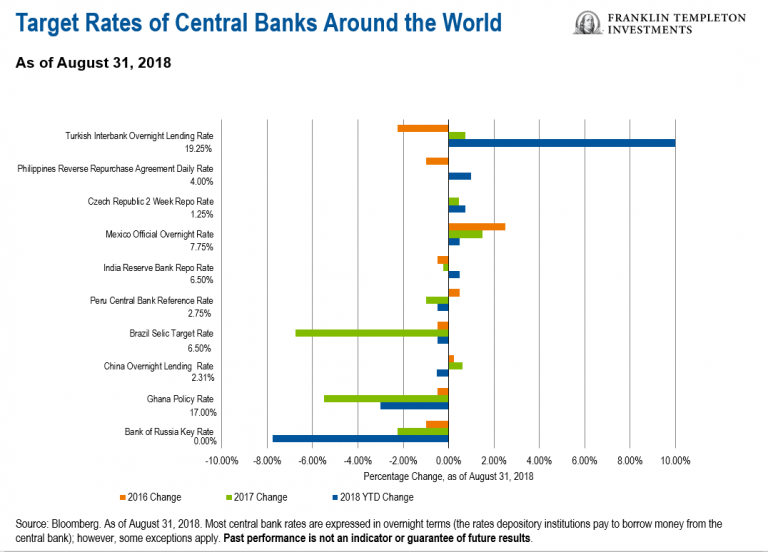

Discretionary Macro

In our opinion, there are many potentially attractive trade opportunities for discretionary managers stemming from macro divergence between countries and their resulting policy responses, important political elections and international trade negotiations. The recent weakness in emerging markets may also present an attractive entry point, but volatility and potential risks remain elevated.

Comments, opinions and analyses expressed herein are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. Because market and economic conditions are subject to rapid change, comments, opinions and analyses are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy.

Data from third party sources may have been used in the preparation of this material and Franklin Templeton has not independently verified, validated or audited such data. Franklin Templeton and its third party sources accept no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user. Important data provider notices and terms available at www.franklintempletondatasources.com.

This information is intended for US residents only.

What Are the Risks?

All investments involve risks, including possible loss of principal. Hedge funds are complex investments and may not be appropriate for all investors. Investment in these types of hedge-fund strategies is subject to those market risks common to entities investing in all types of securities, including market volatility. There can be no assurance that the investment strategies employed by hedge fund and liquid alternative managers will be successful. It is always possible that any trade could generate a loss if the manager’s expectations do not come to pass. Hedge strategy outlooks are determined relative to other hedge strategies and do not represent an opinion regarding absolute expected future performance or risk of any strategy or sub-strategy. Conviction sentiment is determined by the K2 Advisors’ Research group based on a variety of factors deemed relevant to the analyst(s) covering the strategy or sub-strategy and may change from time to time in the analyst’s sole discretion.

These materials reflect the analysis and opinions of K2 Advisors, and may differ from the opinions of other portfolio managers, investment teams or platforms at Franklin Templeton Investments.

For more information on any of our funds, contact your financial advisor or download a free prospectus. Investors should carefully consider a fund’s investment goals, risks, sales charges and expenses before investing. The prospectus contains this and other information. Please read the prospectus carefully before investing or sending money.

1. Duration is a measure of the sensitivity of the price (the value of principal) of a fixed-income investment to a change in interest rates. Duration is expressed as a number of years.

© Franklin Templeton Investments

© Franklin Templeton Investments

Read more commentaries by Franklin Templeton Investments