When Will the Federal Reserve Hit the Pause Button?

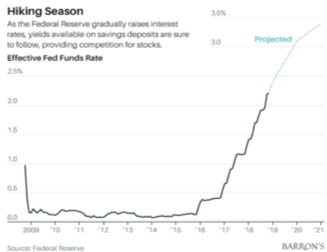

After the meeting on September 26 the FOMC published its dot plot and the expected path for the federal funds rate through the end of 2020. If all goes according to this script the federal funds rate will be raised in December, three more times in 2019, and once in 2020 with the federal funds rate reaching 3.25% - 3.50%. One has to admire the FOMC for having the chutzpah to publically publish the level the federal funds rate will crest during the second longest business cycle in history and precisely when it will take place. As Mike Tyson said, “Everyone has a plan until they get punched in the mouth.” No one is going to punch members of the FOMC in the mouth but the trajectory of the U.S. economy is not likely to follow the smooth path the Fed’s dot plot anticipates. The majority of FOMC members believe the Fed should lean against the fiscal stimulus that is generating a surge of economic growth that can be expected to narrow whatever slack is remaining in the labor market. Doubters of the Phillips Curve have become more numerous and vocal since the U-3 unemployment rate has fallen from 10.0% to under 4.0%, while wage growth has been far weaker than the Phillips Curve projected.

It’s possible that doubters and believers in the Phillips Curve have focused on the wrong measure of unemployment. As I noted in March 2015 Macro Tides, the U-6 unemployment rate is a better indicator of labor market slack than the widely followed U-3 unemployment rate. “While the (U3) gets the headline every month, the U6 unemployment rate, an alternate measure of the labor market, probably provides a better measurement of the actual amount of slack in the labor market. The U6 unemployment rate includes those working part time but who would prefer full-time employment and those who are marginally attached to the labor market, since they still want to work but have become discouraged. When the U3-U6 spread is above 3.85%, there is excess slack in the labor market and thus wages would increase more slowly. Since October 2012 the U3-U6 spread has gradually improved, but it is still fairly wide, which likely explains why annual wage growth has not risen faster than the 2.2% rate of the past few years.” I have referenced this analysis in a number of Macro Tides since March 2015 and always concluded that wage growth was likely to remain muted until the U3-U6 spread narrowed to less than 3.85%. The U3-U6 spread has been a far better predictor of wage growth than the Phillips Curve which has only produced head scratching, derision, and doubters. In May 2018 Alan Blinder, the former Vice Chairman of the Federal Reserve from June 27, 1994 to January 31, 1996, wrote an editorial in the Wall Street Journal entitled “Is the Phillips Curve Dead?” The former Vice-Chairman of the Fed noted that “The correlation between unemployment and changes in inflation is nearly zero… Inflation has barely moved as unemployment rose and fell.”

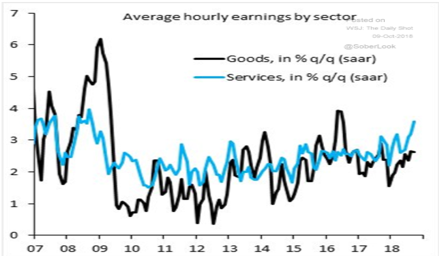

In the November 2017 Macro Tides I explained why wage growth was likely to accelerate in coming months. “In the October 2017 employment report, the U6 rate fell to 7.9% and the U3 rate dipped to 4.1%, so the U6-U3 spread in October was 3.8%. This is the lowest in nine years, and if maintained in coming months, is at the level that has led to higher wage growth since 1994. Wage growth is finally likely to accelerate in coming months.” In 2015, agriculture contributed around 1.05% to the GDP of the United States, 20.5% came from industry, and 78.92% from the service sector. Service sector wage growth is more important than the goods producing sector since it affects inflation more broadly. From 2010 until late 2017, wage growth in services flat lined just above 2.0%. Since then wage growth in the service sector has picked up nicely, as has wage growth in the goods producing sector, just as the U3-U6 spread suggested.

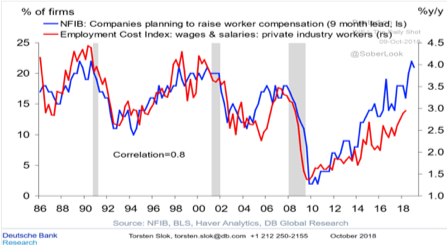

The unemployment rate was the lowest since October 1969 in September and October 2018, so for the few believers in the Phillips Curve left on the FOMC a late cycle pick up in wages is overdue and a real risk. The October employment rate will only heighten that risk. While the U3 rate was unchanged at 3.7%, the U6 rate fell to 7.4%, so the U6-U3 spread is down to 3.7%. The narrowing of the spread will continue to put upward pressure on wages. This outlook is supported by the recent survey of small businesses by the National Federation of Independent Businesses (NFIB). The September survey by the NFIB indicates that small businesses are expecting to boost wages in the next 9 months to keep experienced workers happy and from finding another employer offering more money.

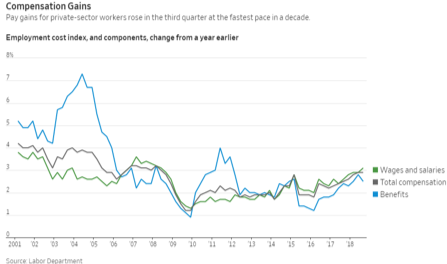

The Employment Cost Index is a broad measure of total income since it combines wages and salaries and benefits. Wages and salaries were up .9% in the third quarter and 3.1% from the prior year. That’s the largest increase since April 2009. Wages and salaries account for about 70% of total compensation according to the Labor Department. Benefit costs were up 0.4 percent in the third quarter and total compensation rose 2.9% from a year ago, the best gain in more than 10 years.

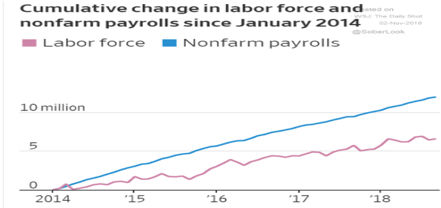

The increase in wages in the October employment report and the information from quarterly Employment Cost Index is not the only labor market concern for the FOMC. Since 2014 job growth has handily outpaced the growth in the labor force and was the outcome the Federal Reserve was hoping for. This is why the U3 and U6 unemployment rates have fallen as much as they have since 2014 and why wage growth has accelerated. The basic premise of the Phillips Curve is that there is a labor market wall at some level that when reached causes a much sharper increase in wages that become embedded in labor costs and the overall inflation rate. Labor costs represent about 65% of the cost of goods and a bigger share for service costs. Sooner or later the growth rate in the working age population needs to increase but that is largely dependent on an increase in population. Permitting the immigration of qualified working age workers is the easiest and most practical solution to spur GDP growth in the next decade. Current political ideology precludes this solution. Growth will suffer as a result and not average 3% as promised by President Trump as slow growth in the working age population curbs GDP growth.

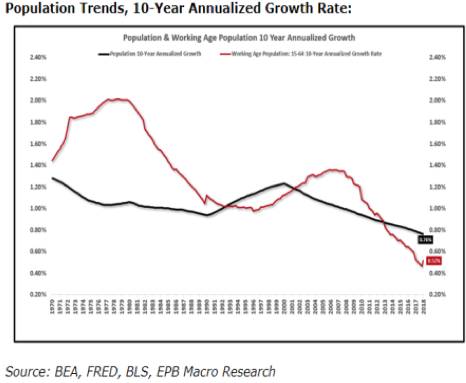

After the Baby Boom surge from 1946 to 1964, the 10-year annualized Population growth rate slowed from 1970 until 1990 falling from 1.34% to .93% (black line). During the healthy economic growth the U.S. experienced from 1991 until the dot.com boom ended in 2000, the 10-year growth rose from a .94% annual rate to 1.20%. Since 2000 economic growth has slowed especially when compared to GDP growth during the 1990’s and in the wake of the 2008 financial crisis. In response the 10-year population growth rate slowed to .76% in 2018. Working Age Population lags population growth since it measures those aged 15 to 64 (red line). This is why it topped in 1979 at 2.0% after the Baby Boom peak in 1964, and then declined until 1996 to .97%. It then peaked in 2007 at an annual rate of 1.37% but has slumped to .52% in 2018. One of the primary determinants of potential GDP growth longer term is the rate of growth in the labor force. The current downtrend in the Population growth rate basically caps future growth in the working age Population growth for at least the next 15 years.

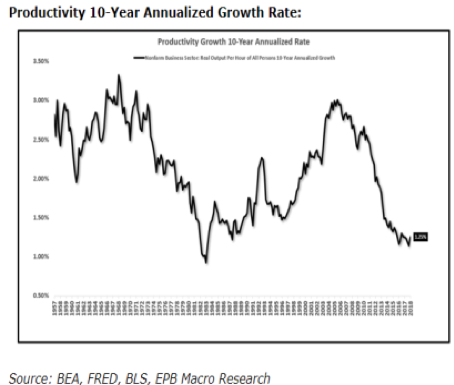

The second determinant of long term GDP growth is productivity, which rose smartly after World War II before the 10-year annual average peaked above 3.0% in 1970. The 10-year average in Productivity plunged from 1970 until 1983, before it bottomed just below 1.0%. One factor that likely weighed on productivity growth was the significant increase in long term interest rates during the 1970’s that ended in September 1981. Strong economic growth during the 1980’s and 1990’s helped productivity improve but GDP growth was also propelled by the technological innovation that came to fruition during the 1990’s. This enabled the 10-year average in productivity to reach 3.0% in 2005. The boom of the 1990’s was followed by a bust and the 10-year annual growth rate in productivity growth has fallen to 1.21% in 2018.

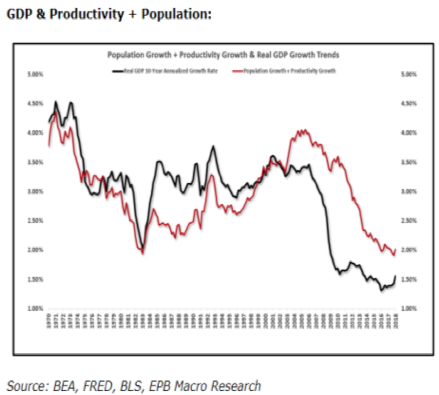

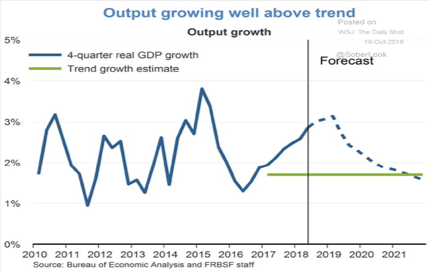

The economy’s long term growth potential is derived by adding the growth rate in the working age population and productivity. When GDP growth (black line) is above the long term potential rate of growth (red line), as it is currently, the risk of an increase in inflation is higher than when GDP growth is below the potential rate of growth. This is why the Federal Reserve expects GDP growth to slow and fall back to its long run potential growth rate, which is currently estimated to be below 2.0%. It is also why the Federal Reserve believes it is necessary to increase the federal funds rate to neutral since GDP growth is well above 2.0%. The neutral interest rate is the rate at which monetary policy is neither accommodative nor restrictive, and where growth and inflation are both at their natural rate on a stable basis.

In the next six months the Fed will attempt to identify the neutral level for the federal funds rate. In Chairman Powell’s press conference after the FOMC meeting on September 26, he emphasized the uncertainty surrounding the appropriate neutral rate, future productivity growth, and impact of trade tariffs on inflation and economic growth. While Powell’s candor about the Fed’s capability of knowing the neutral rate with precision is refreshing, the dot plot provided by the members of the FOMC at the FOMC’s September meeting indicates where they think it is. The doves on the FOMC think it is 2.75% and the hawks think it is 3.0%. The median rate was 2.9% which mathematically indicates that there are 1 or 2 more members who believe its 3.0%, rather than 2.75%. The median average would have been 2.875% if the two camps were equal. The important point is that even the doves support two more increases in the federal funds rate.

Prior to the October employment report, there were a small number of strategists speculating that the Fed might not raise the federal funds rate at the December meeting, and a more vocal group who thought the Fed would be one and done (CNBC’s Jim Cramer). If the doves support 2 more hikes, the odds of one and done are low. In an October 3 question-and-answer interview with Judy Woodruff on PBS, Chair Powell said the Fed no longer needed the policies that were in place that pulled the economy out of the financial crisis malaise. "The really extremely accommodative low interest rates that we needed when the economy was quite weak, we don't need those anymore. They're not appropriate anymore." As I have noted, with the federal funds rate at 2.18% and inflation above 2.18% as measured by the Consumer Price Index, the real federal funds rate is still negative and accommodative. Powell acknowledged this fact during his interview on PBS, "Interest rates are still accommodative, but we're gradually moving to a place where they will be neutral. We may go past neutral, but we're a long way from neutral at this point, probably."

In his first major policy speech on October 25 Federal Reserve Vice Chairman Richard Clarida said more interest rate increases are likely warranted. "I believe monetary policy today remains accommodative, and that, with the economy now operating at or close to mandate-consistent levels for inflation and unemployment, the risks that monetary policy must balance are now more symmetric and less skewed to the downside.”

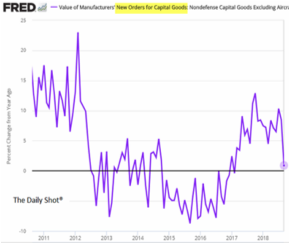

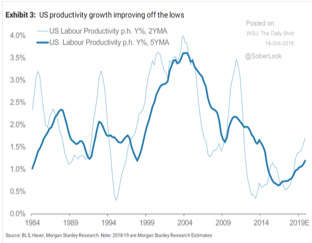

As Powell noted one unknown is whether productivity will improve and by how much, since it will largely be determined by the amount of business investment by companies. Business investment soared after the election from a Year-over-year rate of -5.0% to +12.8% in late 2017. However, the issue of trade and tariffs likely caused companies to curb investment in the third quarter of 2018 causing the Y-O-Y growth to fall to less than 1%. If the trade issue is reconciled and business investment picks up, the improvement in productivity seen in the last two years could continue. The two year moving average of productivity has climbed from 0.5% in 2016 to 1.7% in 2018, while the 5-year average has improved from .65% to 1.20%. If productivity rises further, the FOMC will be more comfortable in not moving the federal funds rate much above neutral in 2019. The FOMC will be monitoring business investment in the first half of 2019 to determine if productivity is likely to allow the Fed to slow rate increases after the neutral rate is reached. Even if productivity rises to 2.0%, GDP growth will still be less than 3.0%, unless the working age population growth rate is boosted from .56% through the immigration of qualified working age workers. This should be about the math and not politics.

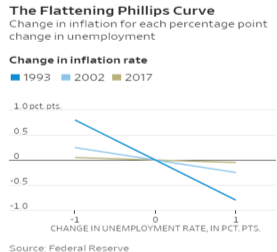

In an interview with the Wall Street Journal on November 1, Chair Powell discussed the Phillips Curve and said the Phillips Curve has simply changed in recent decades, and should not be discarded as an economic artifact. Studies by the staff of the Federal Reserve conclude that from the late 1970’s to the early 1990’s, the correlation between inflation and the Phillips curve was high. A 1.0% drop in the jobless rate would push inflation higher by 0.5% to 0.8%. During the recovery from 2001 to 2007, a 1% decline in the unemployment rate only raised inflation by .25%. During the current recovery inflation has only moved up by .05% for each 1.0% fall in the U3 rate. For Powell this “does not signal the death of the Phillips curve and is consistent with a very flat Phillips curve and inflation expectations anchored near 2%.” This statement is revealing and suggests that Powell may be more tolerant of a further decline in the unemployment rate, without the Fed having to push the federal funds rate beyond the neutral rate. This position is obviously dependent on wage growth rising gradually and not spiking. Powell could be receptive to the Federal Reserve pausing and becoming more data dependent, but only after the federal funds rate has been raised to neutral.

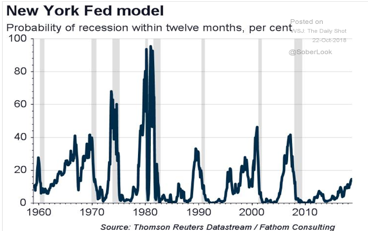

“Everyone has a plan until they get punched in the mouth.” What would it take to cause the FOMC to deviate from its plan of raising the federal funds rate in December and 3 times in 2019? Whatever the reason it would have to be significant enough to threaten economic growth and convince the FOMC to pause before additional rate hikes. A 10% decline in the stock market would not qualify. As I noted in the October Macro Tides “FOMC members are likely to become more circumspect about monetary policy in speeches and interviews, even though this might increase the level of uncertainty and volatility in the financial markets. However, the Fed may not view that as a bad thing, since the last two recessions were not preceded by a bout of cyclical inflation, but excesses in valuations in the financial markets as noted recently by Chair Powell and Lael Brainerd.” That said a 20% decline in the S&P 500 would get the Fed’s attention, especially if it was in response to surprisingly weak domestic data, or an international disruption. I expected the U.S. economy to slow in the second half of 2018 and it is. Although the Federal Reserve has been increasing the cost of money with its increases in the federal funds rate, it has not taken any steps to lower the availability of liquidity. The higher interest rates will certainly slow U.S. growth in coming months, but as long as the availability of liquidity is not impaired the risk of recession is low. The New York Federal Reserve assesses the risk of a recession in the next twelve months as being less than 20%, so the risk of an imminent recession is low. Any shock to the U.S. economy is far more likely to come from overseas.

Global Growth Slows More than Expected

In the August Macro Tides, which was entitled “Synchronized Slowing Growth”, I discussed how much global growth had already slowed and why it was likely to slow further. “The strength in air freight traffic, container traffic, Global Industrial Production, and Global PMIs formed the back bone of the synchronized global growth story. Growth is still positive in all of these components but some of the air has come out of the story. The introduction of tariffs and angst about global trade in general has had a dampening effect on export activity, as measured by the new exports sub component of the JP Morgan Global Manufacturing PMI Index. As trade talks drag on or trade tensions increase, particularly with China, the global economy will be facing another headwind that was not present in 2017 when global growth was stronger and more synchronized.” In August and September the notion that the global slowdown could bleed into U.S. earnings or affect growth in the U.S. was overlooked by the majority of strategists. That changed as more companies began to mention in their third quarter earnings call how the global slowdown was expected to hurt future revenues and profits.

China Trade Talks

Since President Trump levied tariffs on $50 billion of imports from China in March, the consensus view was that China would eventually negotiate. The U.S. buys more than $500 billion worth of goods from China while China only purchases $140 billion of U.S. exports giving the U.S. leverage. The consensus view also cited that the U.S. stock market was continuing to set all time highs while China’s stock market was plunging. I disagreed with the consensus view as I discussed in the August Macro Tides “China, No Trade Pushover.” “In the U.S. time is measured by quarters, but in China it is measured in decades. China’s leadership is not immune from short term considerations, but their focus is not centered on the next year or two but where things will be in 5 to 10 years and beyond. President Trump faces reelection in 2020 while changes to China’s Constitution will allow President Xi Jinping to remain in office until he dies. Actions speak louder than words or Tweets and China has been taking steps to insulate and bolster its economy from any short term negative impact from trade. In recent years China has expanded its military reach to a number of islands in the South China Seas despite Chinese President Xi Jinping’s 2015 pledge to President Obama that “China does not intend to pursue militarization” on the Spratly Islands. China’s military expansion reflects a mindset that is focused on the long term and an attitude that China will not be bullied nor dissuaded by any country. The Commerce Ministry also issued a statement on August 2. “China has been fully prepared and will have to retaliate to defend national dignity and the people’s interests.” The word dignity caught my attention since it indicates that for China the trade negotiations represent something much bigger. China wants to be treated as an equal to the U.S. and respected, and that’s something China is not willing to trade away.”

The stock market rallied like Pavlovs’s dog on November 1 after President Trump tweeted that he had just had a good conversation with President Xi of China. “Just had a long and very good conversation with President Xi Jinping of China. We talked about many subjects, with a heavy emphasis on Trade. Those discussions are moving along nicely with meetings being scheduled at the G-20 in Argentina.” On November 2, the stock market rebounded from a steep loss after Trump said he and President Xi would be having dinner at the G-20 meetings. Most investors are still clinging to the belief that China will eventually cave in to President Trump. My guess is that after President Trump and President Xi break bread at the G-20 meetings they will emerge and announce they have agreed to talk again! Whoopee!

The U.S. has already imposed a 25% tariff on $50 billion of Chinese imports and a 10% tariff on $200 billion of additional imports from China that will be increased to 25% on January 1, 2019. President Trump has pledged to impose a 10% to 25% tariff on the remaining $257 billion in imports not covered also on January 1, 2019. President Trump believes that the threat of these additional tarIffs will compel China to cowl to his demands. This outcome does not seem likely. If negotiations fail to make any substantive progress, and China’s economy slows due to the higher tariffs, the Chinese may use devaluation to retaliate. This would be signaled if the Yuan falls below .14397, or the Dollar rises above 6.955 and definitively if the Dollar rises above 7.0. Should China devalue its currency, EM currencies would experience another wave of selling and global financial markets may swoon, as they did in August 2015 after the Yuan was devalued.

European Union and Italy

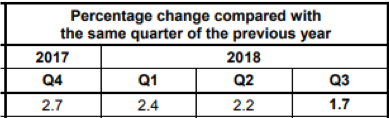

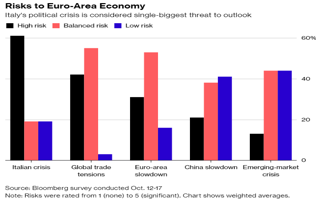

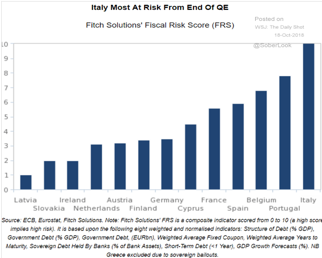

In the third quarter GDP growth in the EU fell to 0.2% half of the 0.4% increase in the second quarter. Although GDP in Q3 was up 1.7% from a year ago, growth has decelerated sharply from the 2.7% rate in Q4 of 2017. Some of the slowing is due to a natural modest ebbing after the strong spurt of growth in 2017, but more of the slowdown is from the fallout from trade concerns. GDP growth in Italy fell to 0.0% which was the lowest since Q4 in 2014. On an annualized basis GDP slumped to 0.8% in Q3 the slowest in three years. The absence of growth in Italy confirms the results of a Bloomberg October 2018 survey that Italy poses the greatest risk to the EU, even greater than trade tensions or a slowdown in China.

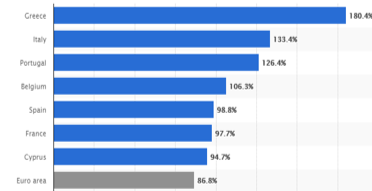

How do you spell disfunction? I-t-a-l-y. In the 72 years since World War II, Italy has had 66 governments or one every 1.1 years. Italy’s new government is composed of the left wing populist 5 Star Movement and the far right wing League. The U.S. domestic equivalent would be Bernie Sanders followers joining arms with members of the Tea Party. On October 16 the Italian government submitted its 2019 budget to the European Union. Italy’s 2019 budget proposes a boost to welfare spending, cutting the retirement age, and an increase in infrastructure spending that would result in a budget deficit of 2.4% of GDP not just in 2019 but through 2021. The budget passed by Italy’s parliament assumes good GDP growth in the next few years and far exceeds estimates by the International Monetary Fund (IMF) and Goldman Sachs. If growth is slower than Italy has projected, the larger annual budget deficit will cause Italy’s debt to GDP ratio to rise from 133.4%. Italy’s debt to GDP ratio is second only to Greece and is 53% higher than the average in the EU.

Italy’s 2019 budget proposal was not well received in Brussels. The budget blatantly breaks EU budget rules that oblige Italy to cut debt every year and turn its structural deficit into a surplus. As one EU official stated, “People are underestimating the scale, the complete insanity of the deviation. And Italian growth assumptions are ludicrous. Growth, especially with this government, will not get better, it will get worse.” Another EU senior official went further, “The budget plans for the next three years mean that Italy, and the euro zone with it, are sleepwalking into the next crisis.” Italy’s total debt is $2.82 trillion and its refinancing needs of $315 billion in 2019, $225 billion in 2020, and $206 billion in 2021 are large according to Reuters data. After a draft of the new government’s budget plan became public in May, the Italian 10-year government bond yield surged from 1.79% in May to 3.30% on November 2. The increase in interest rates will add to Italy’s annual budget deficit and increase the risk that refinancing the large sums coming due in 2019, 2020, and 2021 could become problematic. If global lenders balk at refinancing Italy’s debt, as doubts about its growth prospects increase, the EU’s European Stability Mechanism (ESM) bailout fund may not be large enough. When Greece was bailed out in exchange for draconian reforms, the three tranches Greece received were worth $285 billion. Italy needs to refinance a total of $746 billion during the next three years, so the risk of a major meltdown is real, unless northern countries (Germany) feel compelled to act. The reality is any rescue of Italy will not be proactive. It will be reactive just as it was with Greece. Northern country politicians will only acquiesce after turmoil in financial markets forces them to act.

This risk could develop sooner rather than later since the ECB is planning to reduce it monthly purchases of EU debt from $15 billion in the fourth quarter to zero in January 2019. Italy has been the biggest beneficiary of the ECB’s QE program and would be the country most at risk according to Fitch Ratings once it is suspended. Mario Draghi has attempted to apply some central bank leverage while negotiations are occurring since Italy has until November 13 to amend its budget proposal. My guess is that the EU and Italy will come to some compromise that avoids an immediate breakdown. However, Italy’s structural debt problems are likely to lead to another “Whatever it takes” moment in 2019 or 2020.

Italy’s weak economic growth since the 2008 financial crisis has not allowed Italian banks to sufficiently strengthen their balance sheets. Although Non-Performing Loans (NPL’s) as a percent of total loans have fallen from absurd levels in 2015, they are still an impediment to growth and a risk to the Italian financial system. In 2018 NPL’s were 9.7% of total loans or 2.7 times higher when compared to a NPL average of 3.6% in the EU. By comparison, in the U.S. nonperforming loans as a percent of total loans is 1.02%. Domestic government bonds make up 10% of Italian banks total assets. As noted interest rates on Italian 10-year government debt have surged from 1.79% in May to 3.30% on November 2, but yields have risen across the entire maturity spectrum. With government bond yields rising the value of government bonds prices have declined. As the yield premium Italian bonds pay over safer German Bunds rose since May, Italian banks lost on average 40 basis points (BPS) of their core capital in the second quarter and another 8 bps in the third quarter. The Italian traders’ association Assiom Forex has warned that an increase to 400 bps between German and Italian 10-year yields would force some banks to tap investors for cash, so those banks can maintain capital ratios. After climbing to 3.31% on October 19, the spread fell to 2.99% on October 29.

The transmission mechanism that would deliver problems in Italy and the EU to the shores of the U.S. is the Euro currency. The dark blue line in the Italian Woes chart is the spread between 10-year yields in German bunds and Italy. The spread has been inverted so as the spread widened in May the dark blue line declined. The price of the Euro (light blue line) is overlaid on top of the inverted yield spread so the correlation between the two is obvious. The Euro fell sharply in May as the spread widened and rallied in August and September as the spread narrowed. In the short term, sentiment has become quite negative toward the Euro and as long as the Euro holds above 1.130, the Euro has the potential to rally to 1.18 before the end of the year. If I’m correct and some deal is reached between the EU and Italy, the rally could be especially sharp. Conversely, if the spread between 10-year German bunds and Italian bonds closes above 3.5% (350bps), the Euro could break down below 1.130. The Euro represents 57.6% of the Dollar so a rally to 1.18 would cause the Dollar to fall in the short term.

Dollar Strength

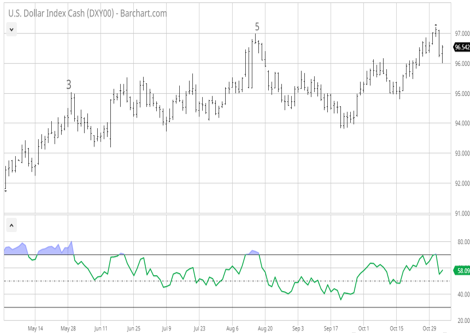

From its low of 88.25 in February I expected the Dollar to rally to 95.00 in part due to weakness in the Euro. After reaching 95.00 at the end of May the Dollar subsequently pushed up to 96.98 in mid August before pulling back to 93.81 on September 21. The rallied up to 97.20 on October 31 as the Euro tested its support at 1.13. Sentiment toward the Dollar is overly bullish since investors expect rate increases by the Fed to lead the Dollar higher. This view overlooks that the Dollar tumbled by more than 14% after peaking at 103.80 in January 2017, even though the Fed increased the federal funds rate in December 2016 and followed with 3 more hikes in 2017. Positioning in the Dollar shows that hedge funds have a very large long position so the Dollar has already benefited from their buying. If the Euro rallies as I expect, the Dollar could fall back to the September low near 94.00, even as the Federal Reserve raises the federal funds rate at their December meeting. If the Dollar fails to rally after the December rate hike, selling could increase and contribute to further weakness.

Emerging Markets

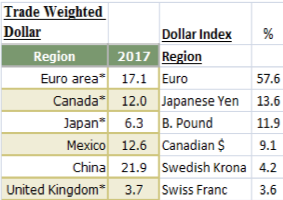

There are two Dollar indexes: the Trade Weighted Dollar index (TWD) and the far more popular Dollar index. The currency weighting is very different in each index. The Euro’s weighting drops from 57.6% in the Dollar index to just 17.1% in the TWD, while China’s representation goes from 0% to 21.9% and Mexico’s is 12.6% instead of 0% in the Dollar index. Emerging markets represent 33.9% of the TWD so comparing the relative performance of the two Dollar index’s can be instructive. The Dollar index was 6.4% below its January 2017 peak on October 31, while the TWD was just 1.1% under its late December 2016 peak. This explains in part why Emerging Market bonds and stocks have been so weak in 2018. Technically, the key take away is that the TWD is approaching the trend line from its peak in 2002 (130.20) and 2016 (128.68), so this is a key area of resistance. Should the TWD break out above the 2002 high it would likely lead to serious problems for Emerging Market countries and companies that are carrying too much dollar denominated debt. The Bank of International Settlements found that U.S. denominated debt to non-bank borrowers reached $11.5 trillion in March 2018. Over $200 billion of USD-denominated bonds and loans, issued by emerging market governments and companies will come due during the remainder of 2018 and $500 billion will come due in 2019, according to the Wall Street Journal.

President Trump is not a big fan of a strong Dollar. As I noted in the January 2017 Macro Tides, “In a May 2016 interview on CNBC, candidate Trump provided his view of the Dollar. “I love the concept of a strong Dollar, and in many respects obviously I like a strong Dollar. While there are certain benefits, it sounds better to have a strong Dollar than in actuality it is.” This statement provides a valuable insight as to how Trump might respond if the Dollar continues to increase in value in 2017. It suggests that Trump might not hesitate to talk the Dollar down, if he thinks it will help improve U.S. trade competitiveness and bring jobs back to the U.S.” I followed up in the February 2017 Macro Tides. “The only surprise is that Trump didn’t even wait until he was in office to do it. In an interview with the Wall Street Journal published on January 17, he described the Dollar as “too strong.” He also said the U.S. might need to “get the Dollar down” if a change in tax policy pushes it up. “Having a strong Dollar has certain advantages, but it has a lot of disadvantages.” If the Dollar rallies in coming months I will be surprised if President Trump and Treasury Secretary Mnuchin don’t attempt to talk the Dollar down.

President Trump has been publically critical of the Federal Reserve for raising rates and specifically Chair Powell. Powell and the other members of the FOMC are not newbies and understand that presidents have frequently pressured the Federal Reserve to keep rates low or not to raise them much. FOMC members know this just comes with the territory and will not be swayed from doing what they believe is in the best interest of the country. The only difference from the past is that President Trump has been far more public in expressing his view. However, if and when they decide to deviate from their plan to raise rates 3 times in 2019, the Fed will need clear economic data that justifies a pause, so they don’t appear to have been cowled by President Trump.

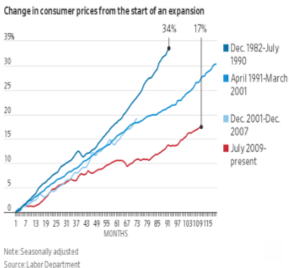

The trade negotiations with China, problems with Italy that cause the Dollar to strengthen, Emerging Market debt troubles are potential punches in the mouth that might convince the Fed to pause after getting the federal funds rate to a neutral level. That is not likely to occur until the Fed has increased the federal funds rate at least twice. The other punch would be if inflation escalates more in coming months and forces the Fed to increase the federal funds rate faster than the expected pace in 2019 of March, June, and sometime in the second half of the year. This risk shouldn’t be dismissed either, just because inflation has remained much tamer in the current recovery than the 1990 or 2001 expansions. If anything most investors are too complacent. Wage growth could push up to 3.5% in the first half of 2019 and an increasing number of companies are raising their prices. Some of the price increases are the result of previously enacted tariffs which have led to an 8% increase in aluminum prices and steel prices soaring by 38%. If the proposed additional tariffs go into effect in January, inflation will rise as more companies are forced to cover the increase in their costs by raising prices. For the past decade companies cut prices so they could maintain market share. Companies are now increasing prices across a wide range of industries and the price increases are sticking and provide competitors the cover needed to also raise prices. This is a significant change that the FOMC has surely taken note of.

Treasury Yields

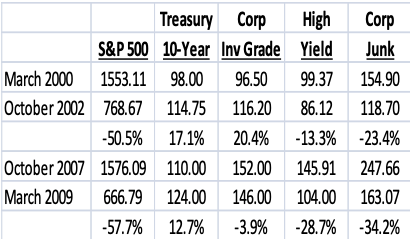

In the July 2017 Macro Tides I asked a question, “Is a Secular Bear Market in Bonds Possible?” I noted that financial advisors and investors who had a traditional allocation of 60% stocks and 40% bonds during the bear markets of 2000-2002 and 2007-2009 were partially insulated from equity losses that exceeded 50% in each bear market. Treasury bonds provided gains to offset losses, while investment grade corporate bonds performed well, especially in the 2000-2002 bear market. Even High Yield and Junk bonds helped cushion the equity losses, although they did lose money.

It’s possible that the low in the 10-year Treasury yield at 1.32% in July 2016 may have marked the end of the secular bull market and the beginning of a new bear market in Treasury bonds. Even if this proves to be true, the initial increase in Treasury rates is likely to be gradual. Pension funds and global investors are likely to buy Treasury bonds as yields tick higher. The second reason is that the negative correlation between Treasury bonds and stocks is a relatively new phenomenon. During the 1940’s, 1950’s, 1960’s, 1970’s, 1980’s, and 1990’s, bond and stock prices were fairly correlated. Although stocks typically ignored the initial increase in Treasury yields, they eventually succumbed and a bear market followed.

The key point is respecting that bear markets occur and investors must be prepared to alter their investment strategy in order to deal with a potential secular bear market in bonds. The buy and hold approach which has served investors and financial advisors well since 1981 may be the wrong strategy, if the bond market is on the cusp of the next secular bear market. This suggests that investors and financial advisors should consider adopting a tactical approach for a portion of their bond assets. A tactical strategy could minimize losses during periods when yields are rising, and potentially add capital gains when bond yields fall.

In March of 2017, I thought the yield on the 10-year Treasury bond could fall from 2.60% to under 2.20%, as the economy displayed signs of slowing and a record short position held by institutional investors expecting higher interest rates in the Treasury bond futures were forced to cover. The 10-year Treasury yield fell to 2.177% before rising to 2.42%. The pattern in the 10-year Treasury yield bond suggests the yield could fall below 2.177% and approach 2.0%. However, the coming low in the yield could represent a higher low relative to the July 2016 low of 1.32%, and set the stage for the next move up in yields before the end of 2017. This suggests a review of the allocation to bonds and the investment strategy employed in managing bond market risk by investors and financial advisors is appropriate.”

This advice proved prescient as the 10-year Treasury yield fell to 2.037% on September 7, 2017 and has since climbed to 3.248% in October 2018. As I recommended in July 2017 a tactical approach could minimize losses when yields are rising and potentially add capital gains. Since the low in yields in September 2017, I have recommended both long trades and short trades as indicated on the Treasury bond ETF TLT. The buy and hold approach lost money since September 2017 as I expected it would.

During the first Taper Tantrum in 2013, the 10-year Treasury yield rose by about 1.30%. From the low of 1.32% in July 2016, the 10-year Treasury yield increased to 2.62% in March 2017, an increase of 1.30%. From the September 2017 low of 2.037%, an equal rise of 1.30% suggests the potential for the 10-year Treasury yield to climb to 3.33% before the potential of another trading low is possible.

Stocks

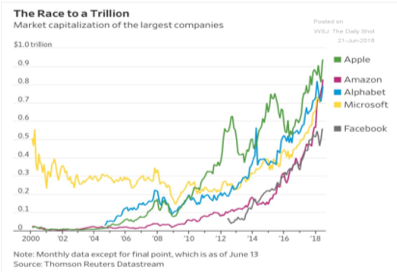

In the July Macro Tides I discussed Parabolic Curves and their Aftermath and the historical relevance of parabolic curves as they related to the FAANG stocks. “Parabolic curves are created by human emotion and psychology and are accompanied by a really good story that creates a veneer of authenticity enabling investors to rationalized irrational behavior. What prompted my renewed interest in parabolic curves was a chart showing how Facebook, Apple, Amazon, Alphabet, and Microsoft (FAAM) have performed during the past 15 years. The upward curve in each of the FAAM stocks since 2016 has become more vertical, which is one of the hallmark characteristics of every parabolic curve. All of these companies are well established with great businesses, enabling investors to rationalize almost any valuation. These companies are not comparable to the dot.com bubble, so a ‘crash’ of 70% is not likely. But that doesn’t mean they aren’t vulnerable to a healthy 10%+ correction along the way. This has occurred for each stock on several occasions since 2009. If the S&P 500 is going to fall below 2600 or the February 9 low of 2532, the FAANG stocks must tumble, and I think they will.”

On October 29 the S&P 500 dropped to 2603 before a strong rally took hold after President Trump tweeted on October 31 that he had a conversation with President Xi of China. A retest of the low of 2603 is likely within the next two weeks. If successful, a rally to 2775 to 2810 is likely to follow. Sometime in 2019 the S&P 500 may test the long term uptrend line, which connects the March 2009 low, October 2011 low, and the low in February 2016 low. This suggests the S&P 500 has the potential of trading below 2400 in 2019.

Gold

Looking out over the next 6 to 12 months and longer, Gold is likely to trade above $1260 and possibly above $1300 early next year and above $1400 before the end of 2019.

Jim Welsh

@JimWelshMacro

[email protected]