Debt, Deficits, and Decay

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsThe Wall Street Journal recently pointed out that the US government expects it will spend more in 2020 on interest payments on the government’s debt than it will on Medicaid. The Congressional Budget Office estimates interest payments will surpass national defense spending by 2023 and will be larger than all non-defense discretionary programs combined by 2025.1

Although investors believe it to be a recent issue, few have noticed that the US economy’s secular growth rate has been hindered by a debt overhang for nearly 40 years! Politicians from both parties have repeatedly tried to fend off the secular slowdown in growth by, ironically, adding more debt.

Investors need to be cognizant of the insidious issues relating to debt and deficits that tend to elude political discussions:

1. The debt problem has been growing for roughly 40 years.

2. Not unlike one who foolishly uses home equity to fund a vacation, the Federal government has created a significant asset/liability mismatch by using longer-term liabilities to fund short-term assets.

3. Increasing debt payments have been a major reason that US economic growth has secularly slowed. Debt payments divert the economy’s cash flow away from productive investment.

4. Despite repeated rhetoric to the contrary, politicians continuously try to correct slowing growth by issuing additional debt.

5. The government might have missed an opportunity to “term out” the debt. If Argentina, a marginal credit at best, could issue a 100-year bond, why couldn’t the US? Even low inflation compounded over a long enough period can significantly reduce the burden of repaying debt.

6. The US’s decaying infrastructure is undoubtedly hindering productivity growth and the overall standard of living. Funding badly needed US infrastructure may take some creativity.

7. There is always a business cycle, but investors should not expect US economic growth to secularly improve until we manage the government’s asset/liability mismatch.

The debt problem is nothing new

Debt and its related interest payments seem to be a major factor slowing the US’s secular growth rate because interest payments are diverting a growing proportion of cash flow away from productive use. If borrowed funds do not support projects with high enough and sustainable return-on-investment, then increasing interest payments simply curtail productivity, growth, and the overall standard of living.

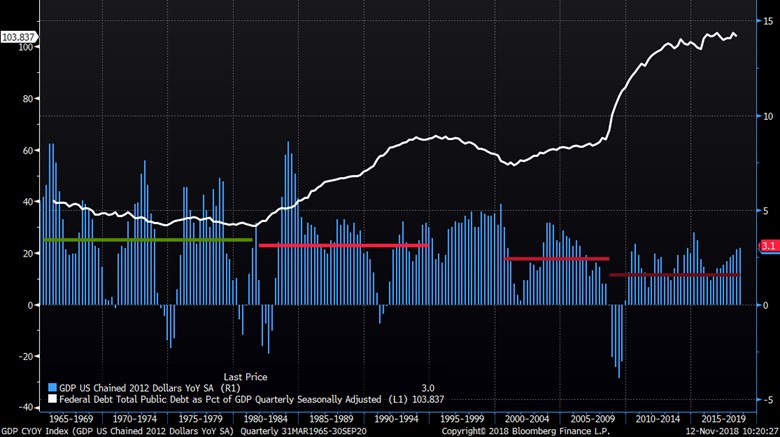

Chart 1 shows a comparison of real GDP growth (bars) and federal debt as a percent of GDP in nominal terms. Prior to 1980, federal debt/GDP was relatively stable and the economy secularly grew about 3.5%/year (green line). Debt/GDP started to rise in the early-1980s, and GDP growth began to secularly slow (light red line). Debt/GDP also grew in the 2000s and secular GDP growth slowed again (red line). More recently, debt grew yet again and secular growth slowed even more (dark red line).

Politicians today are acting as if the US’s debt problem is new, but that is clearly not the case. Both Democratic and Republican administrations have issued debt for short-term economic gain, and the growing interest payments associated with that debt has been contributing to the US’s slowing economic growth for decades.

CHART 1:

Real GDP Growth and Federal Debt as a percent of Nominal GDP

(Dec. 1965 – Sep. 2018)

Source: Richard Bernstein Advisors LLC. Bloomberg Finance L.P.

There is nothing necessarily wrong with borrowing to fund growth so long as the associated economic returns last as long or longer than the life of the liability (i.e., the loan or bond). If growth peters out or projects become obsolete before liabilities are paid off, then future growth might be constrained because cash flow is still needed to pay off the earlier liabilities and cannot be invested in newer projects.

A detrimental asset/liability mismatch can occur when assets’ lives are shorter than those of the associated liabilities. For example, homeowners faced a significant asset/liability mismatch a decade ago when they utilized home equity loans to fund short-term consumption. Advertisements encouraged homeowners to use their home equity to go on vacation, buy a new television, etc., but failed to mention that it might take years to pay off the loan that funded those purchases.

The US government has constructed an asset/liability mismatch over the past 40 years by using debt to spur economic growth geared for two-year election cycles. Repeatedly boosting the economy by cutting taxes or increasing government spending (and accordingly boosting voter confidence) prior to an election has left the US in a similar predicament to the home equity borrower who went on vacation.

The US does not face a “day of reckoning” as did homeowners because the US can issue additional debt to roll over previous obligations. However, the US economy must nonetheless siphon increasing proportions of cash flow to service liabilities as The Wall Street Journal article highlighted.

Terming out debt

Investors often worry about burdening future generations of Americans with repayment of today’s debt. The US may have unfortunately missed a unique opportunity to alleviate such concerns.

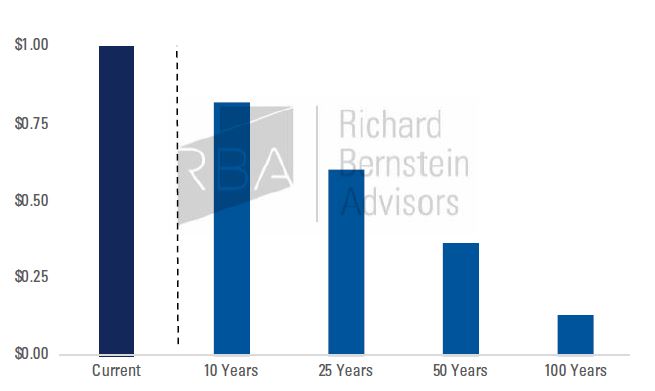

The US could have “termed out” its debt when interest rates were historically low. Many entities issued 50- and 100-year debt to take advantage of longer repayment periods with little increases in periodic coupon payments relative to existing debt. Even Argentina, a very tenuous credit at best, issued one such 100-year bond.

Extremely long-term debt can be advantageous to the issuer because the repayment of principle does not occur for an extraordinarily long time (i.e., 50 or 100 years hence). Chart 2 shows how low inflation (2%/year, which is the Federal Reserve’s target inflation rate) alters the nominal value of $1. For example, $1 today would have the purchasing power of about $0.13 in 100 years. Even with low inflation, roughly 87% of today’s debt burden would be inflated away.

CHART 2:

Purchasing Power of $1.00 by Time Horizon with 2% Inflation Rate

Source: Richard Bernstein Advisors LLC.

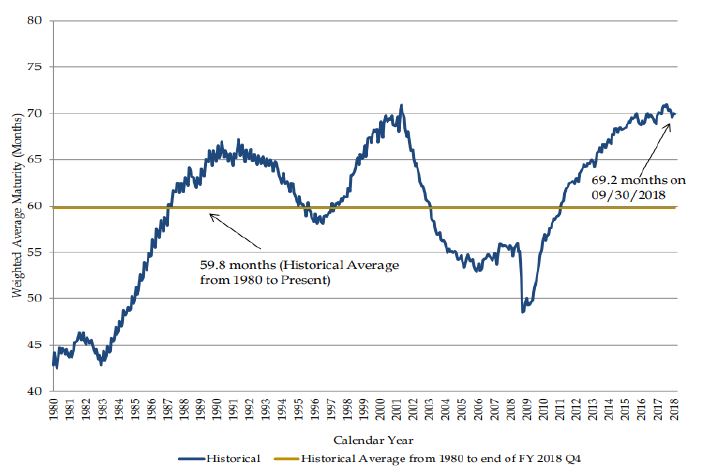

The government has indeed attempted to extend the maturities of Treasuries being issued, but not substantially so. Chart 3 shows the weighted average maturity of government debt outstanding. Maturities have been extended, but an average of 70 months hardly takes advantage of the compounding of inflation. Although rates have risen, they remain low by historical standards and the opportunity to issue extremely long-term debt might still be available.

CHART 3:

Historical Weighted Average Maturity of Marketable Debt Outstanding

(Dec. 1980 – Sep. 2018)

Source: Department of the Treasury: Office of Debt Management

Infrastructure and its funding

The government’s asset/liability mismatch mentioned earlier occurred because short-lived assets have been funded with longer-lived debt. It might have been much wiser to use debt to invest in longer-lived assets with benefits accrued to society over the lifetime (or hopefully past the lifetime) of the liability that funded it.

Infrastructure projects are typically long-lived assets from which generations can derive the benefits. Every morning I travel through a 108-year-old train tunnel. I strongly doubt that the constructors of the tunnel anticipated it lasting over 100 years, but it clearly qualifies as a long-lived asset that has lasted longer than the life of the debt that funded its construction. Chart 4 shows that funding for rebuilding things like the 108-year-old tunnel has been dwindling. Transportation Department spending as a percent of government outlays is at an all-time low.

CHART 4:

Transportation Department Spending as a Percent of Government Outlays

(Dec. 1962 – Dec. 2017)

Source: Department of the Treasury: Office of Debt Management

Fixing America’s decaying infrastructure has become the “baseball, hot dogs, and apple pie” of American politics because infrastructure is a key contributor to enhancing productivity and competitiveness (think of millions of Americans doing something productive instead of sitting in traffic). Everyone understands the need for improving US infrastructure, but funding infrastructure projects could be politically difficult as many object to additional debt funding or to raising taxes. A creative funding solution may be needed.

While we are certainly not experts in municipal finance implementation, it might be reasonable to incorporate aspects of various types of revenue raising methods:

1. War bonds – funds could be earmarked to a national infrastructure emergency.

2. Revenue bonds/floating rate bonds/inflation protection bonds – interest payments could be tied to revenue and float through time with no specific or guaranteed coupon. If there is inflation, then revenue should increase providing some inflation protection.

3. Treasuries – A special class of bonds could be backed by the full faith and credit of the US government should an issuing entity default.

4. Municipal bonds – interest payments could be tax-free.

5. Transportation assessments – assess corporate profits to pay for infrastructure for a non-renewable set period (e.g., 10 years). Although some might say this is an increase in corporate tax rates, corporations benefit greatly from efficient public goods that the private sector will not solely construct (e.g., efficient highways, ports, and train systems).

Debt, Deficits, and Decay

There is nothing necessarily wrong with debt and deficits so long as there is an effective asset/liability match. The problem for the United States is that politicians from both parties have supported a multi-decade period of using longer-term debt to fund short-term assets.

A wiser use of debt would be to match long-lived assets with long-lived liabilities. Long-lived assets, like infrastructure, benefit generations of Americans. Long-lived liabilities are easier to pay off through time because of simple compounding even of low inflation rates.

Fixing America’s decaying infrastructure has become the “apple pie” of American politics, but the reality is that politicians continue to fund short-term growth with long-term liabilities. There is always an economic cycle, but investors should not expect US economic growth to secularly accelerate until we solve this problem.

© Copyright 2018 Richard Bernstein Advisors LLC. All rights reserved. PAST PERFORMANCE IS NO GUARANTEE OF FUTURE RESULTS

Nothing contained herein constitutes tax, legal, insurance or investment advice, or the recommendation of or an offer to sell, or the solicitation of an offer to buy or invest in any investment product, vehicle, service or instrument. Such an offer or solicitation may only be made by delivery to a prospective investor of formal

offering materials, including subscription or account documents or forms, which include detailed discussions of the terms of the respective product, vehicle, service or instrument, including the principal risk factors that might impact such a purchase or investment, and which should be reviewed carefully by any such investor before making the decision to invest. RBA information may include statements concerning financial market trends and/or individual stocks, and are based on current market conditions, which will fluctuate and may be superseded by subsequent market events or for other reasons. Historic market trends are not reliable indicators of actual future market behavior or future performance of any particular investment which may differ materially, and should not be relied upon as such. The investment strategy and broad themes discussed herein may be unsuitable for investors depending on their specific investment objectives and financial situation. Information contained in the material has been obtained from sources believed to be reliable, but not guaranteed. You should note that the materials are provided "as is" without any express or implied warranties. Past performance is not a guarantee of future results. All investments involve a degree of risk, including the risk of loss. No part of RBA’s materials may be reproduced in any form, or referred to in any other publication, without express written permission from RBA. Links to appearances and articles by Richard Bernstein, whether in the press, on television or otherwise, are provided for informational purposes only and in no way should be considered a recommendation of any particular investment product, vehicle, service or instrument or the rendering of investment advice, which must always be evaluated by a prospective investor in consultation with his or her own financial adviser and in light of his or her own circumstances, including the investor's investment horizon, appetite for risk, and ability to withstand a potential loss of some or all of an investment's value. Investing is subject to market risks. Investors acknowledge and accept the potential loss of some or all of an investment's value. Views represented are subject to change at the sole discretion of Richard Bernstein Advisors LLC. Richard Bernstein Advisors LLC does not undertake to advise you of any changes in the views expressed herein.

1 Kate Davidson and Daniel Kruger, “US on a Course to Spend More on Debt Than Defense,” The Wall Street Journal. November 11, 2018

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All