Collective Investment Trusts (CITs) have been gaining momentum in the retirement space, and for good reason. Jason Colarossi, vice president, national retirement strategist, of Franklin Templeton’s Defined Contribution Division, outlines what CITs are and how they have evolved. He also discusses the different types of strategies and the growth we have seen with this investment vehicle recently.

What’s a Collective Investment Trust (CIT)?

CITs are tax-exempt, pooled investment vehicles sponsored and maintained by a bank or trust company which also serves as the trustee. Typically available only to qualified retirement plans, CITs combine assets from eligible investors into a single investment portfolio (or “fund”) with a specific investment strategy. By commingling, or pooling, assets, sponsors of CITs may take advantage of economies of scale to offer lower overall expenses. The sponsoring trustee provides an additional level of risk management, and today’s CITs offer more innovative investment opportunities than in the past.

Also known as collective investment funds, these vehicles have gained in popularity within the defined contribution (DC) space—which includes 401(k) plans—in recent years.

While sharing some characteristics of mutual funds, unlike mutual funds, neither the Securities and Exchange Commission (SEC) nor the Investment Company Act of 1940 regulate CITs. However, CITs are subject to supervision and regulation by the Office of the Comptroller of the Currency or similar state banking regulator. To the extent Employee Retirement Income Security Act of 1974 (ERISA) plan assets are invested, CITs are subject to ERISA regulations. As such, the CIT trustee is held to and managed to comply with the fiduciary standards of ERISA.

CITs: Then and Now

CITs have been around as an investment vehicle since the 1920s, but the early adopters were mainly defined benefit (DB) plans, which offer a fixed, pre-established benefit for employees at retirement. CITs were predominantly used in these plans to deliver stable value or passive strategies. However, certain features made them less attractive to a broader audience of investors, such as manual investor transactions, limited performance data availability and infrequent valuations.

In 2000, the National Securities Clearing Corporation added CITs to its mutual-fund trading platform, Fund/SERV®, and the limitations of CITs started disappearing. This allowed CITs to begin offering standardized transaction processing as well as access to daily valuations.

Further advances in technology made it easier to publish CIT information through widely available databases and media, such as Morningstar. The universe of CITs has expanded, with CITs now available across asset classes and investment disciplines, including equities, fixed income, alternatives, multi-asset strategies and international and domestic orientations. They can be actively or passively managed and can be—and often are—used in a fund-of-funds structure, like target-date or target-risk funds.

Types of CITs

Although CITs have come a long way from where they were before, there are still some differences to consider between this investment vehicle and mutual funds. Mutual funds have extensive public performance information available on multiple data aggregators whereas CIT performance is not as widely available. CITs are not subject to the numerous reporting and disclosure requirements applicable to mutual funds and, in general, there are still some limitations on what the average investor can find on CITs. Although CITs have grown in the types of investment objectives available, they still have not reached the broad selection of investment styles available through mutual funds. Both investment vehicles have pros and cons so it is always important for plan fiduciaries to research available options and any other factors involved before selecting investments for a retirement plan.

That said, CITs allow the flexibility to be tailored to the level of customization and specialized needs of a retirement plan. There are three different strategies available.

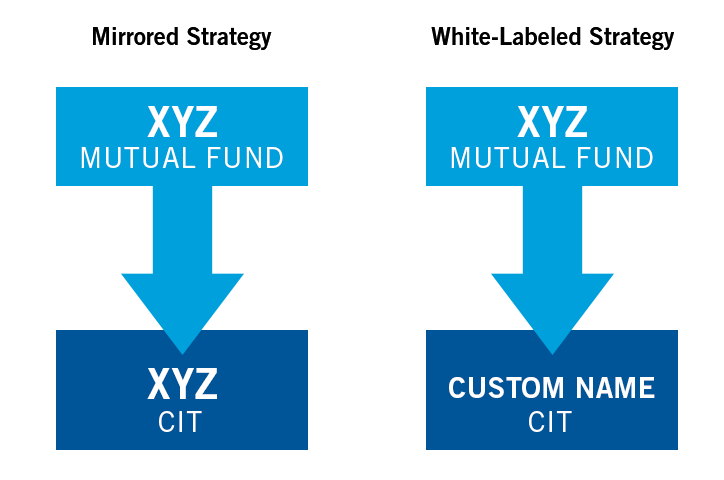

Mirrored and White-Labeled Strategies

Mirrored and white-labeled strategies both leverage the investment strategy and objectives of an existing mutual fund, but white-labeled strategies also allow the product name to be customized for a client. With a white-labeled product, a client can adopt it as their own.

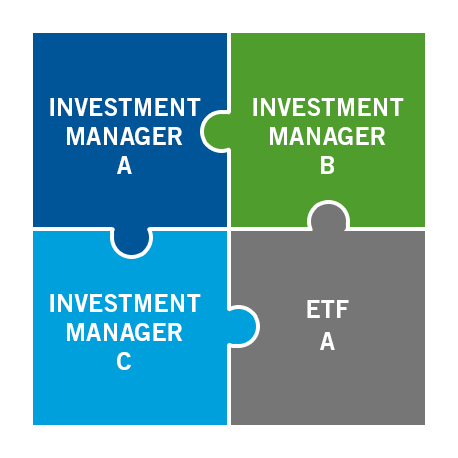

Custom Solutions

Customized solutions are an opportunity for advisors to partner with clients to create a tailored strategy meant to address the specific needs of a retirement plan. Using an innovative and cost-effective approach, CITs can help deliver a number of potential benefits—broader diversification across multiple managers, the potential for enhanced alpha1 opportunities and sophisticated risk management—all combined within a single, easy-to-use offering.

For example, you could construct a CIT with three different active investment managers, along with a passive exchange-traded fund (ETF).

Growth of CITs

While DB plans once dominated the retirement landscape, they have fallen in popularity over the past few decades. Today, DC plans are the primary employer-sponsored retirement savings vehicle, and many have adopted CITs because of beneficial changes in technology, regulation and accessibility.

With CITs, advisers and plan sponsors can negotiate custom fee arrangements and have flexibility in plan options. CITs offer the appeal of a multi-manager approach, which can make it possible to combine the skills of different sub-advisors to manage single asset class CITs, with each providing a distinct investment style.

The multi-manager approach can simplify a DC plan’s investment menu and make it easier for participants to get exposure to a diversified mix of investment strategies within a single allocation. In general, CITs can help keep costs low for several reasons. They usually don’t have redemption fees, they typically have relatively low overhead, have lower compliance costs because they aren’t registered with the SEC, and have lower administrative costs because they generally have fewer recordkeeping requirements. Since CITs are not available for sale to the public, the marketing costs are generally lower as well, as extensive public disclosure requirements are not required. Being exempt from SEC registration also allows CITs to avoid the costs associated with other activities the SEC requires of mutual funds, such as creating and delivering proxies, prospectuses, and Statements of Additional Information.

These are just a few of the reasons why, in 2017, CITs were the second-largest investment vehicle (after mutual funds) in terms of 401(k) plan assets, holding almost 20% of total 401(k) plan assets.2 As we approach the end of 2018, this is an investment vehicle we will be keeping an eye on this year and beyond.

The comments, opinions and analyses expressed herein are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. Because market and economic conditions are subject to rapid change, comments, opinions and analyses are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy.

This information is intended for US residents only.

What are the Risks?

All investments involve risks, including possible loss of principal.

Unlike a mutual fund, the offer and sale of a CIT’s units are not registered under the Securities Act of 1933, as amended, or applicable securities laws of any state or other jurisdiction. In addition, unlike mutual funds, CITs are exempt from registration under the Investment Company Act of 1940, as amended (“1940 Act”), and unit holders are not entitled to the protections of the 1940 Act. Mutual funds are regulated by the SEC and are offered through a prospectus, whereas CITs are offered through banks or trust companies and are regulated by the Office of the Comptroller of the Currency or similar state banking regulator.

As defined in a CIT’s Declaration of Trust, CITs are available for investment by (i) retirement plan trusts that qualify for exemption from federal income tax pursuant to Section 401(a) and 501(a) of the Internal Revenue Code, or are maintained by a governmental employer under Section 414(d) of the Internal Revenue Code, (ii) deferred compensation plans maintained by state or local governmental units under Section 457(b) of the Internal Revenue Code, or (iii) group trusts which consist solely of the assets of these types of plans. The decision to invest in a CIT should be carefully considered. The unit values for the CIT will fluctuate, and investors may lose money.

Investments in the CIT are not insured by the FDIC or any other government agency, are not deposits of or other obligations of or guaranteed by any bank or entity and involve investment risks, include loss of principal invested.

This communication is general in nature and provided for educational and informational purposes only. It should not be considered or relied upon as legal, tax or investment advice or an investment recommendation, or as a substitute for legal or tax counsel. Any investment products or services named herein are for illustrative purposes only, and should not be considered an offer to buy or sell, or an investment recommendation for, any specific security, strategy or investment product or service. Always consult a qualified professional for personalized advice or investment recommendations tailored to your specific goals, individual situation, and risk tolerance.

Securities offered through Franklin Templeton Financial Services Corp. (FTFS). FTFS does not provide legal or tax advice. Federal and state laws and regulations are complex and subject to change, which can materially impact results. We cannot guarantee that such information is accurate, complete or timely; and disclaims any liability arising out of your use of, or any tax position taken in reliance on, such information.

1. Alpha measures the difference between a fund’s actual returns and its expected returns given its risk level as measured by its beta. A positive alpha figure indicates the fund has performed better than its beta would predict.

2. Source: DST Systems, Erach Desai, Jason Dauwen “Collective Investment Trusts – A Perfect Storm.” Understanding CITs and Their New Opportunities, DST Systems, Mar. 2017.

© Franklin Templeton Investments

© Franklin Templeton Investments

Read more commentaries by Franklin Templeton Investments