Themes of 2018

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsEditor’s note: in this, our last commentary of the year, we look at the top economic stories we covered during the year. Please accept our best wishes for the holiday season, and for a prosperous 2019.

Confronting China

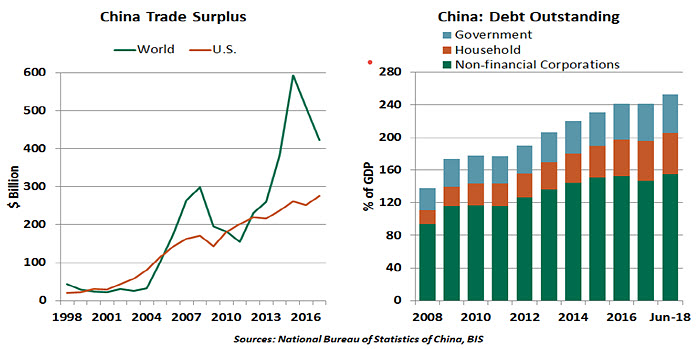

Over the past few decades, China has transformed itself from a minor economy with little global trade to the world’s largest exporter. China is now commonly referred to as the world’s factory, for good reason.

Besides low labor costs, this is largely due to the protection provided to Chinese industries in the form of lax environmental laws, generous domestic subsidies, state ownership and a “managed” currency. China’s appropriation of intellectual property and discrimination against foreign firms have also helped it gain competitive ground.

Unfortunately, these measures violate World Trade Organization (WTO) rules. They also have created large trade deficits among many of China’s trading partners. It is therefore no surprise that China has become the subject of heightened global anxiety. In September, American, European Union (EU) and Japanese trade ministers issued a joint statement criticizing China’s use of subsidies, claiming that China was turning “state owned enterprises into national champions and setting them loose in global markets.”

Thus far, the U.S. is the only country to retaliate (with import tariffs) against China’s practices, but it is gaining some support. The EU and Japan backed the U.S. complaint to the WTO alleging violation of U.S. intellectual property rights by China. The EU agreed to form a new foreign investments screening mechanism, while Germany (like Canada) blocked two prospective acquisitions by Chinese investors and lowered the foreign ownership stakes review requirement to 15% from 25%. The U.K. is also pitching for closer scrutiny of investments by foreign entities.

Chinese authorities have shown a limited willingness to change course, but they may be forced to be more flexible. The massive accumulation of debt across China’s economic sectors cannot be easily sustained if economic growth falters further. Things may get worse in the trade arena before they get better, but China may see wisdom in seeking a truce.

Stuckflation

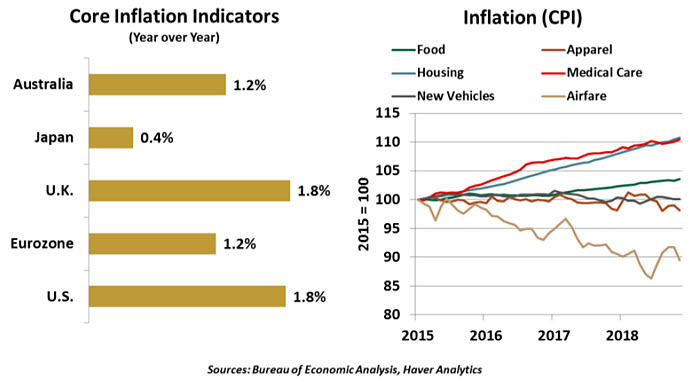

Following the September 2017 meeting of the Federal Open Market Committee, former Chair Janet Yellen stated, “The shortfall of inflation from two percent … is a mystery.” One year and five rate increases later, unemployment is straddling a 50-year low, but inflation remains stubborn. The reason: inflation appears to be held back by structural factors, summarized as the “three As:”

- Automation: Examples of machines replacing workers are legion. Self-checkout stations at grocery stores are ubiquitous, and self-service kiosks at fast food restaurants are helping managers handle the shortage of low-wage labor. Employers are investing in automation rather than paying workers to perform low-skill tasks.

-

Analytics: More data is available to help businesses refine their operations than ever before, helping to cure inefficiencies. Surge pricing by ride-sharing networks helps attract more drivers at high-demand intervals. Package delivery drivers receive calculated routes that optimize time on the road, fuel economy, and even lower risk of accidents. As efficiencies improve, inflation abates.

- Amazon: We cite Amazon as the most prominent of many platforms that have improved buyers’ ability to search for the best prices. This is clearly evident in cumulative price increases for categories where e-commerce has had the greatest penetration.

But the “three As” are gradually working their way into the service sector, as well. Online platforms covering travel, housing and maintenance services have expanded, and consortia are working hard to bring more discipline to the cost of medical care.

Inflation is not entirely in retreat; it has been firm throughout 2018. Nonetheless, central banks and investors may have to re-specify the curves that relate price and quantity across the economy.

Change Is in the Air

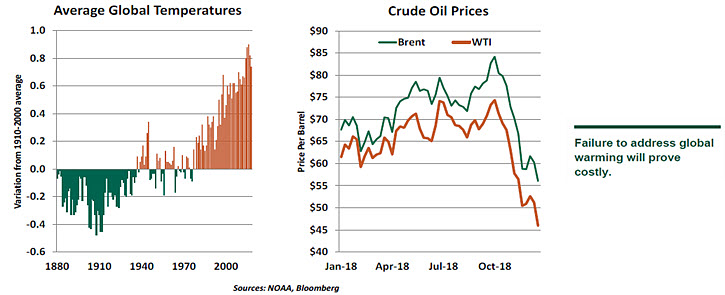

For environmental policy and energy markets, the heat was on in 2018. As we noted in our October essay on climate change, global temperatures have been rising persistently for the past 30 years. While some still debate whether this trend is within historical norms, and whether human behavior is its root cause, the consequences of warming are clear: more severe storms, loss of arable land and shortages of fresh water. Air quality in some parts of the world is disgraceful.

The situation could become much worse over the coming decades, as documented in reports from both the U.S. government and the United Nations. The use of alternative fuels has expanded, but still makes up only a modest fraction of the world’s energy consumption. To avoid a worst-case scenario, an international commitment to limiting carbon dioxide emissions is required.

But getting there will not be easy. Developing countries still burn copious amounts of coal, which is inexpensive and abundant. Petroleum producers are struggling to contemplate life after oil; the dramatic fall in crude prices since October has already created significant stress for several of them. And the United States stubbornly remains the only country in the world refusing to sign the Paris Climate Accord. Instead, it has chosen to ease emissions standards for autos and factories.

Failure to act will have substantial economic and humanitarian consequences. Simulations suggest that global output could be severely damaged by rising temperatures, and populations that cannot survive in more arid climates will seek to migrate. Border control, already a challenging issue, will become even more prominent in the decades ahead.

William Nordhaus, one of this year’s Nobel Prize winners in economics, authored a book entitled “The Climate Casino.” Given the consequences of climate change, we cannot afford to roll the dice on this issue.

A Less Perfect Union

The decades spent laying the groundwork for the European Union’s creation in 1992, and the years since, have been some of the most peaceful and productive years for EU members. But in the past 12 months, the union has seen challenges from all directions.

From the west: Brexit is far from complete. The costs of unwinding the union became tangible this year. Prime Minister Teresa May’s proposed exit deal with the EU contains something for everyone to find distasteful. We agree with May’s assessment that there is no better deal to be found; phrased pessimistically, there is no possibility of a painless Brexit.

From the south: Italy has challenged the EU with its lack of fiscal rectitude. Its proposed budget exceeded the EU’s required government spending limit of 3% of gross domestic product. This tested the EU’s ability to enforce its rules, but was resolved this week with concessions by Italy’s populist government. The malaise is contagious: French president Emmanuel Macron has offered fiscal measures to appease Yellow Vest protestors, but their cost would put France’s outlays beyond the 3% ceiling.

From the east: Poland and Hungary were the latest countries to see a rise in Eurosceptic populism, though Poland has backed down from its more extreme measures, like purging its Supreme Court. And ongoing investigations continue to reveal Russia’s position as an antagonist seeking to upset coalitions and change world power dynamics.

Nationalist leaders are filling the gap left by the failing fortunes of strong pro-European leaders like Macron and Angela Merkel. Turnover next year in the European Parliament and at the European Central Bank may expand the vacuum. In an era in which individual leaders are making outsized impacts, the EU needs advocates who will continue the successful European experiment. Europe must present a united front in an increasingly fractious world.

Aging Awkwardly

It is said that father time is undefeated. This is true, both biologically and financially.

Many countries experienced a population surge in the years after World War II. That generation is now reaching retirement age. Since the end of the baby boom, birth rates in developed countries have fallen sharply, a product of women participating more actively in labor markets and rising levels of household income. (People in wealthier countries have fewer children, because it is costly for parents to spend time away from work.) China has a more extreme version of this problem, thanks to the one-child policy that was in effect for almost 30 years.

These developments have produced a growing demographic imbalance. This has two effects, neither of them good:

- Labor force growth is expected to slow in the years ahead, or even decline in some cases. This will reduce the potential for economies to expand. It will also prompt more active exploration of technological alternatives to replace retiring workers, which can be unsettling

- The ratio of working people to retired people is declining steadily, placing strains on retirement systems around the world. Further, plans and people have failed to invest properly to prepare for their retirements. This may dampen consumption and increase political anxiety in the years ahead.

A country can only narrow a demographic imbalance two ways. Encouraging higher birth rates has been attempted, but has generally not succeeded. This leaves immigration, a topic freighted with controversy. Securing national borders has been a point of international emphasis in 2018, as nationalist sentiment prevails.

But locking immigrants out will lock in the adverse consequences of an aging population. There is still time to find a productive solution to demographic challenges, but time is not on our side.

Divergence

The global expansion, after enjoying a long stretch of coordinated growth, has become asymmetric. Performance and prospects have diverged importantly across regions this year.

In the U.S., tax reductions boosted household income and consumption, while strong business sentiment provided impetus for corporate investments. By contrast, other major advanced economies, namely Europe and Japan, have been unable to sustain growth at prior levels.

In Europe, regional strains, coupled with inadequate or unpopular reforms and elevated trade uncertainty, weighed on both business and consumer confidence. Meanwhile, ongoing Brexit chaos has led businesses to cut or defer investments in the U.K. In Japan, the government has struggled to implement crucial reforms designed to add economic vigor.

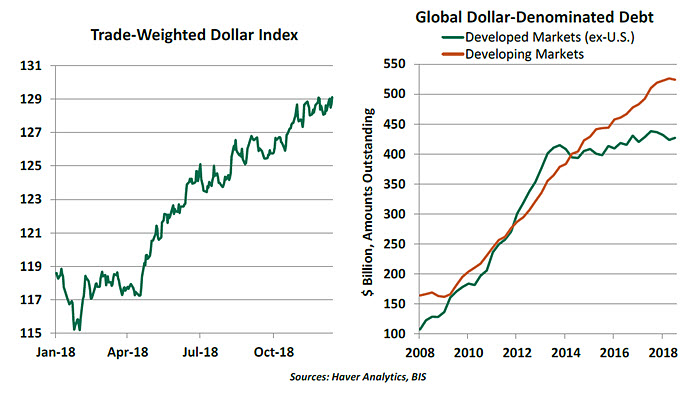

There is divergence among central bank policies, as well. While the Federal Reserve, despite rising criticism, continues to tighten, the European Central Bank and Bank of Japan have maintained their accommodative stances. Persistent Brexit-related uncertainty has hindered the Bank of England’s ability to act decisively. The U.S. dollar has appreciated as a result, which has hindered American exporters.

Emerging markets were the darlings of yield-hungry global investors in recent years, but many are now struggling amid stricter monetary policy, tighter financial conditions and a stronger dollar. Rising uncertainties around global trade and the potential for a Chinese slowdown create additional headwinds for the emerging world.

The year 2018 was initially heralded as the year of synchronized global expansion. It now concludes with countries going their separate ways, making markets anxious about prospects for 2019. Getting things back into alignment may not be easy.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2018 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/disclosures.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All