Numerous uncertainties weighed on investor sentiment in 2018 and led to a down year for emerging markets overall, although the fourth quarter saw some outperformance versus developed markets. Manraj Sekhon, CIO of Franklin Templeton Emerging Markets Equity, and Chetan Sehgal, senior managing director and director of portfolio management, present the team’s overview of the emerging-markets universe in the fourth quarter of 2018, along with their current outlook.

Three Things We’re Thinking about Today

-

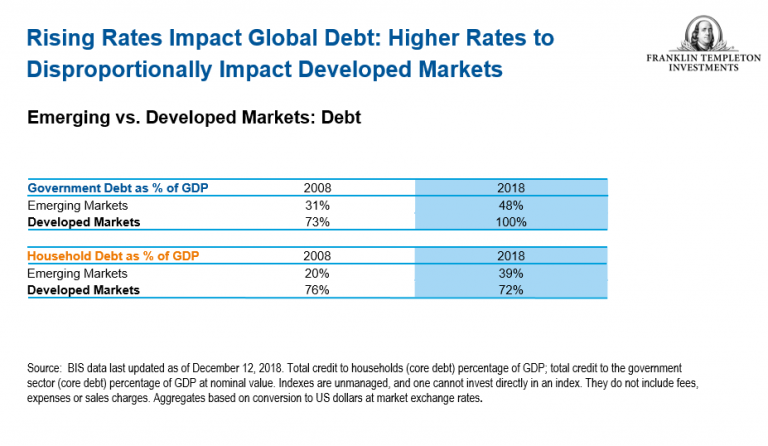

- The US Federal Reserve (Fed) raised its key interest rate by 25 basis points in December, its fourth increase in 2018, and in line with market expectations. While the Fed lowered its US gross domestic product (GDP) growth and inflation forecasts slightly, it continued to see relatively strong growth in the US economy. US interest-rate hike projections for 2019 and the longer run were also lowered, with two interest-rate hikes expected in 2019, instead of three. While rising rates—by design—apply pressure to growth and inflation expectations, this is not solely restricted to emerging markets (EMs), and most debt ratios are considerably higher in the developed world. EMs in aggregate have shifted to current account surpluses, floating exchange rates and a reduced reliance on US-dollar debt funding. However, those emerging economies (and companies) pursuing less prudent policies have been punished heavily by financial markets. Investors appear to be increasingly discerning between winners and losers, which presents opportunities for active management.

- US dollar strength has focused attention on weaker commodity prices and dented investor enthusiasm for emerging markets in recent months—stoking fears that the current climate could lead to a repeat of the 1997-1998 Asian Financial Crisis (AFC). However, we believe these concerns are largely overdone as the last two decades of mass financial reforms have transformed emerging Asia’s financial markets. Twenty years on from the AFC, we regard the economic landscape in many EMs as fundamentally stronger than it was back then. Our experience suggests investors should focus less on what’s going on in the United States, and more on the developments on the ground in the countries themselves. In many cases, EMs have drawn lessons from past crises to strengthen policies and governance. In addition, many EM economies are less commodity-driven then they were decades ago. Therefore, the whims of commodity prices have less influence. Changes in US policy could, of course, still cause pain in EM countries with high external debt. But we have noticed a general shift. Asian monetary policy is no longer as highly correlated with US interest rates and is more dependent on local growth and inflation conditions.

- The recent decline in oil prices has helped ease pressure on the Indian rupee, current account deficit and inflation. The Indian economy also continues to perform well; government capital expenditure (capex) through infrastructure spending has progressed well, corporate capex involving capacity expansion is gradually unfolding, and we believe that household capex is also improving. Consumption remains robust as well. India went through a challenging environment recently where shadow banks, typically referred to as non-banking financial companies (NBFCs) in India, suffered liquidity issues, raising concerns of systemic risk and liquidity across the entire financial system. Liquidity has since been normalizing and credit flows returning. While upcoming elections could impact sentiment in the interim, we do not foresee a significant impact on the domestic economy. As such, our assessment of the macro picture and corporate fundamentals (with continued economic recovery and corporate earnings growth acceleration) supports our favorable long-term conviction for India’s market.

Outlook

Trade tensions have been a primary contributor to weakness in EM equities, and while exports remain a key engine of growth for EMs, they are increasingly shipped to other emerging economies; the relative importance of developed markets has declined. Similarly, the roles of consumption and technology in generating economic growth have become more prominent; EMs have become more domestically orientated. While tariffs undoubtedly come at a challenging time for China as it seeks to deleverage its economy, the impact will also be felt globally.

Despite slowing global growth, EMs are still widely expected to achieve faster economic growth than developed markets (DMs) in 2019 and for the foreseeable future. The International Monetary Fund (IMF) forecasts EMs to grow 4.7% in 2019, more than double the 2.1% estimate for DMs1. EM currencies are relatively cheap after declining in 2018; returning to 2001-2002 levels. We expect to see a recovery in 2019.

EM valuations have become increasingly attractive due to weakened confidence (and performance), yet cash flows and earnings generally remain resilient. EM earnings growth is expected to exceed that of the US and DMs, resuming the trend witnessed in 2017. These conditions, when paired with improving corporate governance that includes dividend payouts and buybacks, present an increasingly attractive long-term buying opportunity for us and should contribute to renewed optimism in the EM asset class.

Emerging Markets Key Trends and Developments

EM equities fell over the fourth quarter, though they fared better than their DM counterparts. Concerns about global economic growth, US interest rate hikes and US-China trade relations stoked market volatility during the period, as they did in much of 2018. The year proved challenging for global markets as a whole, with EM equities losing more ground than DM stocks. The MSCI Emerging Markets Index fell 7.4% over the quarter, compared with a 13.3% decline in the MSCI World Index, both in US dollars.

The Most Important Moves in Emerging Markets This Quarter

- Asian equities pulled back in the fourth quarter, with Pakistan, Taiwan and South Korea leading regional losses. Pakistan’s financial health weakened, while the government sought a bailout from the IMF. Technology-heavy indexes in Taiwan and South Korea were hobbled by weakness in technology stocks. Conversely, markets in Indonesia, the Philippines and India gained, aided by local currency strength. The Indonesian rupiah and Philippine peso rose on central bank action to shore up the currencies against the US dollar. The Indian rupee also advanced as lower oil prices eased worries about the oil-importing nation’s trade deficit.

Emerging European markets lost ground, with Greece, Russia and the Czech Republic especially weak. Hungary and Turkey, however, held on to earlier gains to end the quarter with positive returns. Lower oil prices and increased geopolitical risk weighed on share prices in Russia. The Turkish market benefited from a double-digit gain in November, following significant weakness earlier in the year, as political tensions eased, and the Turkish lira appreciated. The South African market declined but fared relatively better than its EM peers. The South African economy returned to growth in the third quarter of 2018, following two consecutive quarters of contraction.

Frontier markets corrected over the final quarter of the year but performed better than their global counterparts. Lithuania, Romania and Tunisia were among the weakest markets. Vietnam and Kenya also underperformed. Global trade concerns and weak market sentiment weighed on equity prices in Vietnam despite positive earnings results and robust GDP growth. Sri Lanka, Lebanon and Estonia, however, bucked the trend, ending the three-month period with gains. Investors in Sri Lanka remained positive despite continuing political instability and weakness in the Sri Lankan rupee.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

The comments, opinions and analyses expressed herein are solely the views of the author(s), are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. Because market and economic conditions are subject to rapid change, comments, opinions and analyses are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy.

Important Legal Information

All investments involve risks, including the possible loss of principal. Investments in foreign securities involve special risks including currency fluctuations, economic instability and political developments. Investments in emerging markets, of which frontier markets are a subset, involve heightened risks related to the same factors, in addition to those associated with these markets’ smaller size, lesser liquidity and lack of established legal, political, business and social frameworks to support securities markets. Because these frameworks are typically even less developed in frontier markets, as well as various factors including the increased potential for extreme price volatility, illiquidity, trade barriers and exchange controls, the risks associated with emerging markets are magnified in frontier markets. Stock prices fluctuate, sometimes rapidly and dramatically, due to factors affecting individual companies, particular industries or sectors, or general market conditions.

________________________

1. Source: International Monetary Fund, World Economic Outlook Database, October 2018.

© Franklin Templeton Investments

© Franklin Templeton Investments

Read more commentaries by Franklin Templeton Investments